Question: A question about stochastic process. (Gambler's ruin problem) Q. 3. Recall the setting of the gambler's ruin problem: (Xn) is a Markov chain representing your

A question about stochastic process. (Gambler's ruin problem)

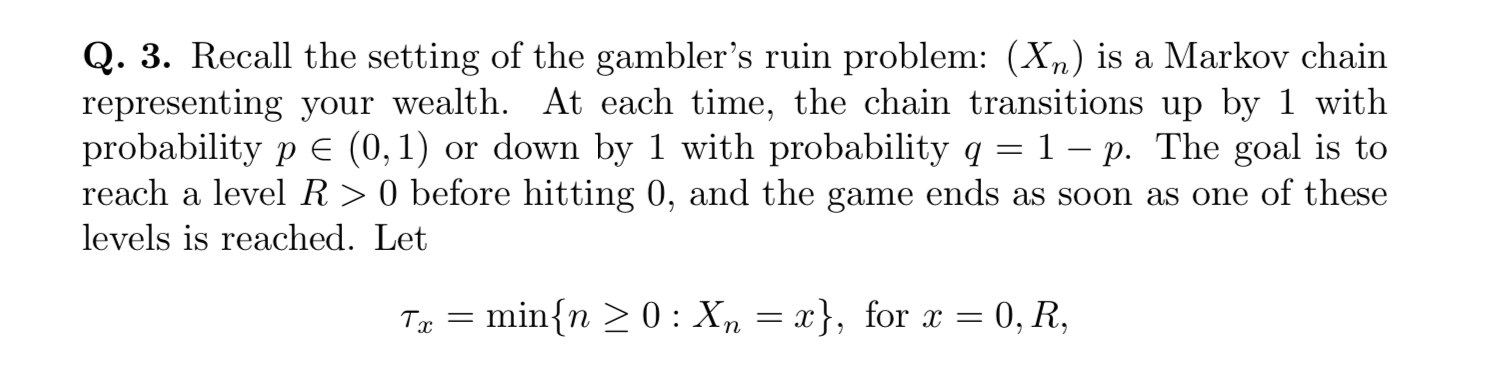

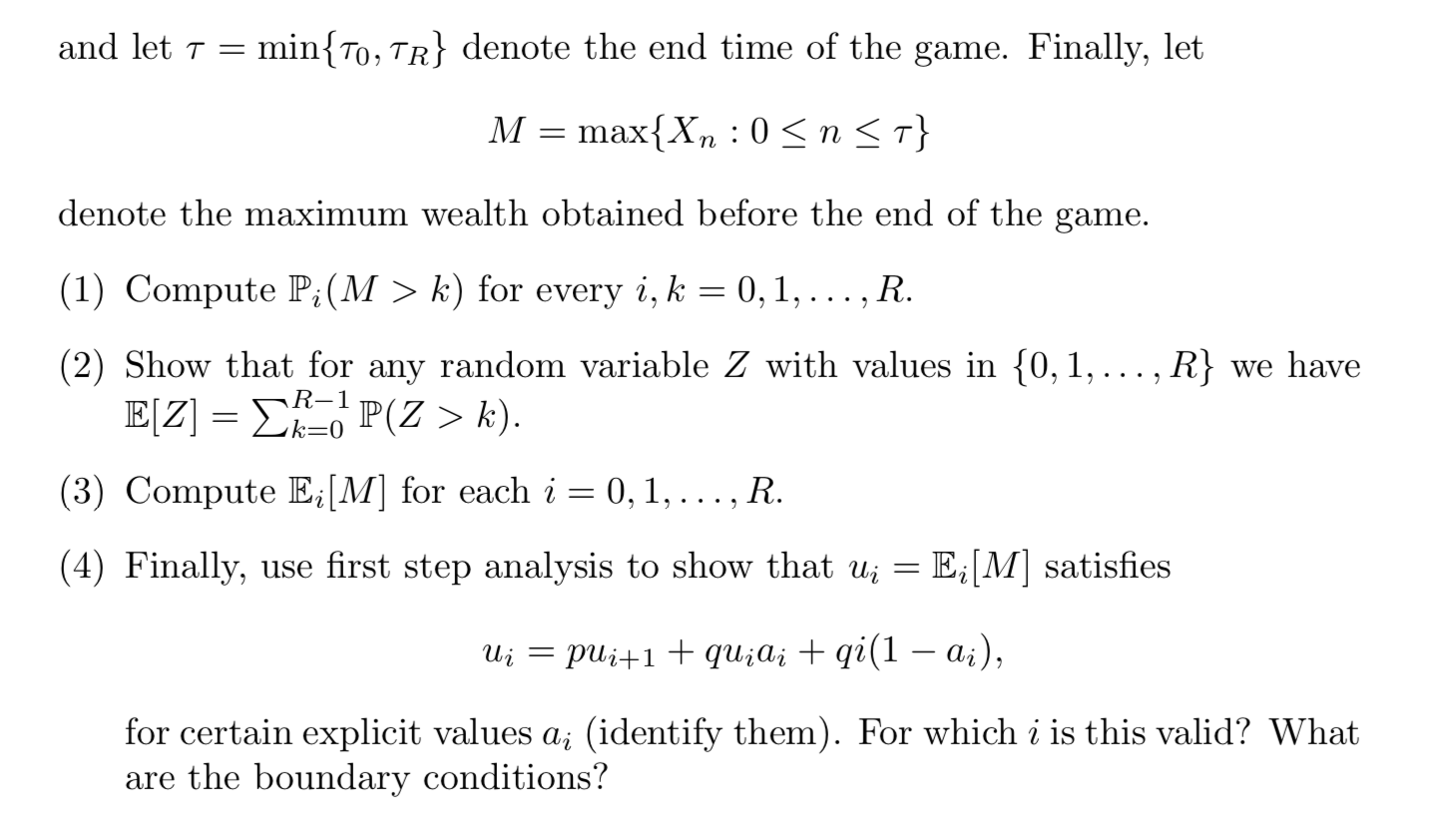

Q. 3. Recall the setting of the gambler's ruin problem: (Xn) is a Markov chain representing your wealth. At each time, the chain transitions up by 1 with probability p 6 (0,1) or down by 1 with probability q = 1 p. The goal is to reach a level R > 0 before hitting 0, and the game ends as soon as one of these levels is reached. Let T3,; = min{n 2 0 2 Xn =33}: for 33 = 03R: and let 7 = min {To, TR} denote the end time of the game. Finally, let M = max { Xn : 0 k) for every i, k = 0, 1, . . ., R. (2) Show that for any random variable Z with values in {0, 1, ..., R} we have E[Z] = ZK OP(Z > k). (3) Compute E:[M] for each i = 0, 1, . . ., R. (4) Finally, use first step analysis to show that ui = E:[M] satisfies Ui = Puit1 + quiai + qi(1 - ai), for certain explicit values ai (identify them). For which i is this valid? What are the boundary conditions

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts