Question: A reconciliation should be presented to explain the difference between the net changes in fund balances for the governmental funds (fund financial statements) and the

A reconciliation should be presented to explain the difference between the net changes in fund balances for the governmental funds (fund financial statements) and the change in net position for the governmental activities (government-wide financial statements). What were several of the largest reasons for the differences?

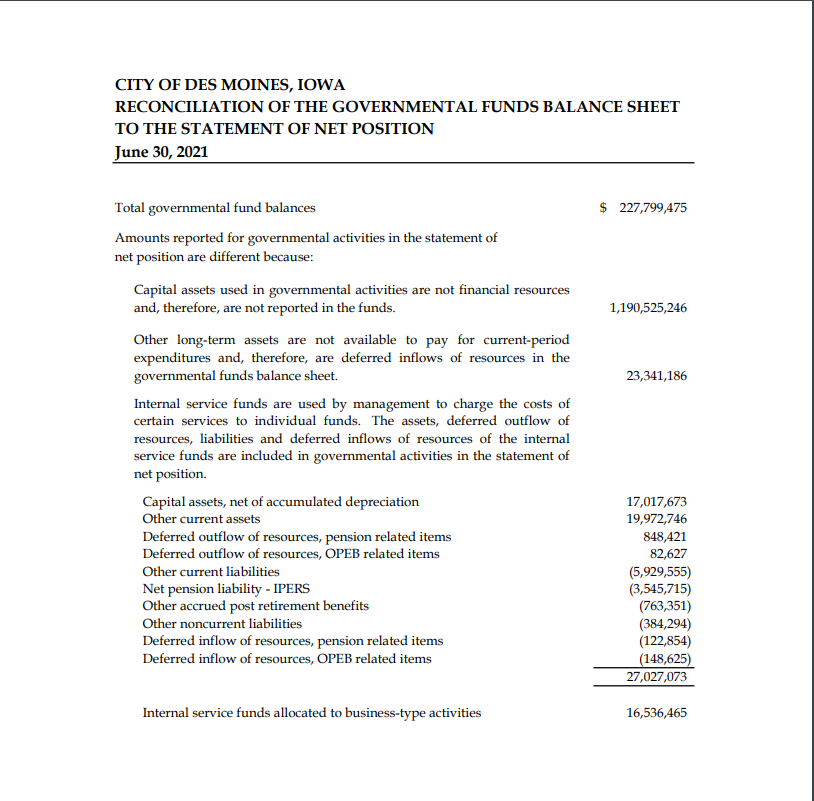

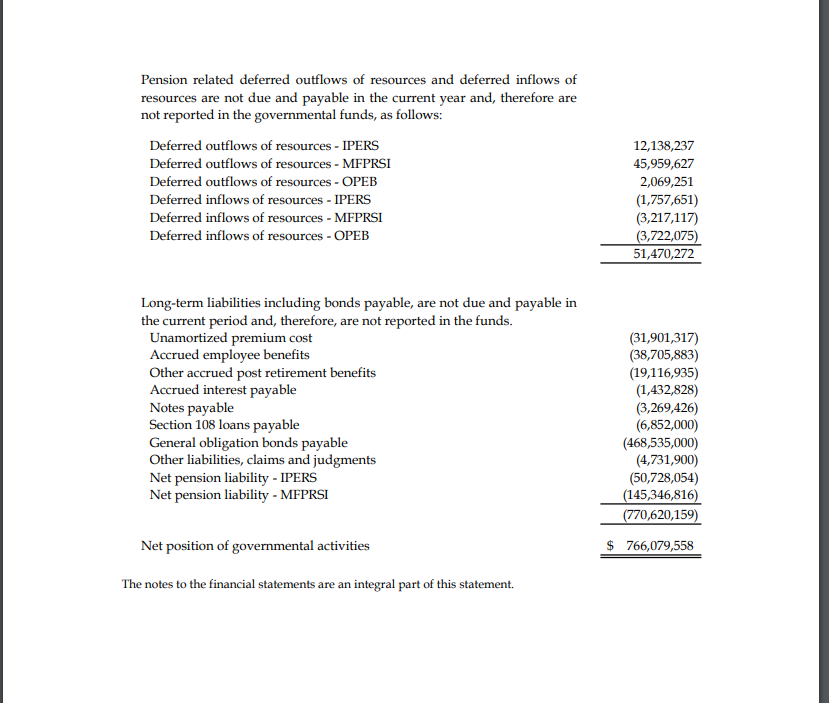

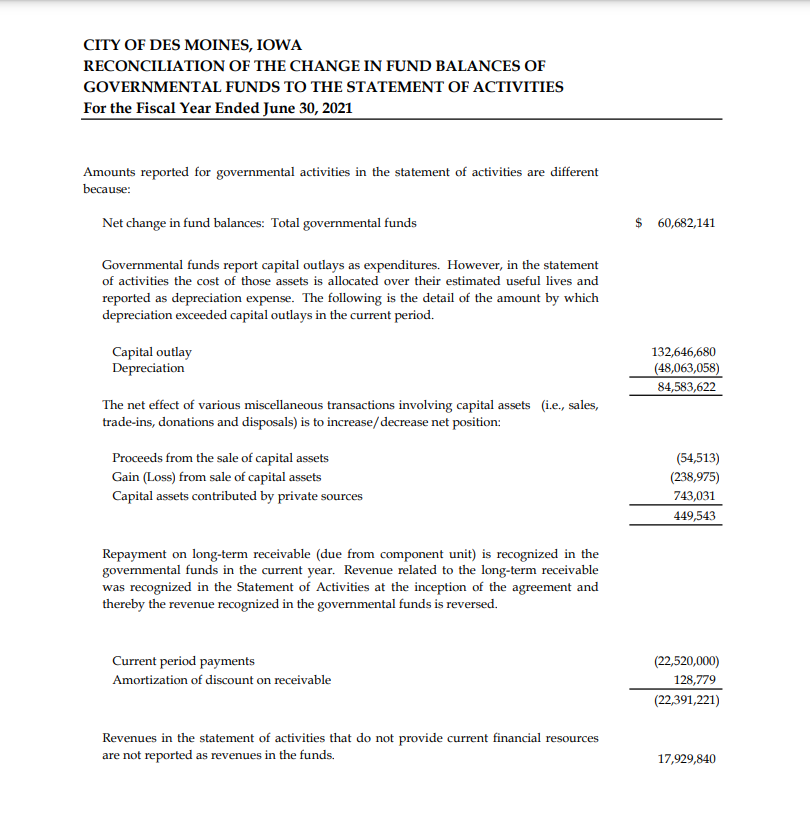

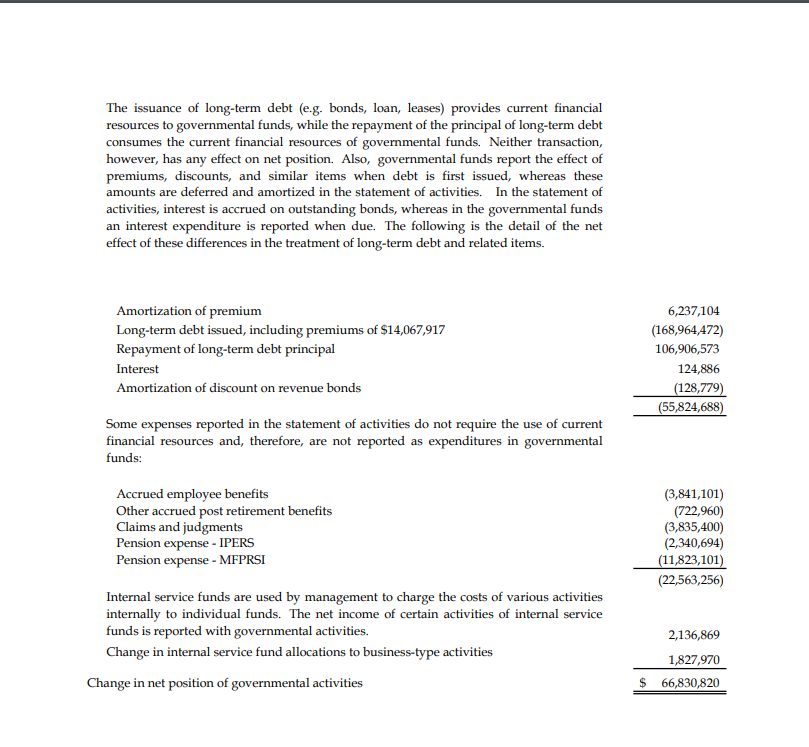

CITY OF DES MOINES, IOWA RECONCILIATION OF THE GOVERNMENTAL FUNDS BALANCE SHEET TO THE STATEMENT OF NET POSITION June 30, 2021 Total governmental fund balances 227,799,475 Amounts reported for governmental activities in the statement of net position are different because: Capital assets used in governmental activities are not financial resources and, therefore, are not reported in the funds. 1,190,525,246 Other long-term assets are not available to pay for current-period expenditures and, therefore, are deferred inflows of resources in the governmental funds balance sheet. 23,341,186 Internal service funds are used by management to charge the costs of certain services to individual funds. The assets, deferred outflow of resources, liabilities and deferred inflows of resources of the internal service funds are included in governmental activities in the statement of net position. Capital assets, net of accumulated depreciation 17,017,673 Other current assets 19,972,746 Deferred outflow of resources, pension related items 848,421 Deferred outflow of resources, OPEB related items 82,627 Other current liabilities 5,929,555) Net pension liability - IPERS (3,545,715) Other accrued post retirement benefits (763,351) Other noncurrent liabilities (384,294) Deferred inflow of resources, pension related items (122,854) Deferred inflow of resources, OPEB related items (148,625) 27,027,073 Internal service funds allocated to business-type activities 16,536,465Pension related deferred outflows of resources and deferred inflows of resources are not due and payable in the current year and, therefore are not reported in the governmental funds, as follows: Deferred outflows of resources - IPERS 12,138,237 Deferred outflows of resources - MFPRSI 45,959,627 Deferred outflows of resources - OPEB 2,069,251 Deferred inflows of resources - IPERS (1,757,651) Deferred inflows of resources - MFPRSI (3,217,117) Deferred inflows of resources - OPEB (3,722,075) 51,470,272 Long-term liabilities including bonds payable, are not due and payable in the current period and, therefore, are not reported in the funds. Unamortized premium cost (31,901,317) Accrued employee benefits (38,705,883) Other accrued post retirement benefits (19,116,935) Accrued interest payable (1,432,828) Notes payable (3,269,426) Section 108 loans payable (6,852,000) General obligation bonds payable (468,535,000) Other liabilities, claims and judgments (4,731,900) Net pension liability - IPERS (50,728,054) Net pension liability - MFPRSI 145,346,816) (770,620,159) Net position of governmental activities 766,079,558 The notes to the financial statements are an integral part of this statement.CITY OF DES MOLNES, IOWA RECONCILIATION OF THE CHANGE IN FUND BALANCES OF GOVERNMENTAL FUNDS TO THE STATEMENT OF ACTIVITIES For the Fiscal Year Ended June 31], 202] Amounts reported for governmental activities in the statement of activities are different because: Net change in fund balances: Total governmental funds lGovernmental funds report capital outlays as expenditures. However, in the statement of activities the cost of those assets is allocated over their estimated useful lives and reported as depreciation expense. The following is the detail of the amount by which depreciation exceeded capital outlays in the current period. Capital outlay Depreciation The net effect of various miscellaneous transactions involving capital assets [i.e.. sales. trade-ins, donations and disposals} is to increase;Ir decrease net position: Proceeds from the sale of capital assets lGain {Loss} from sale of capital assets Capital assets contributed by private sources Repayment on long-term receivable [due from component unit} is recognized in the governmental funds in the current year. Revenue related to the long-term receivable was recognized in the Statement of Activities at the inception of the agreement and thereby the revenue recognized in the governmental funds is reversed. Current period payments Amortization of discount on receivable Revenues in the statement of activities that do not provide current financial resources are not reported as revenues in the funds $ 59,682,141 132,646.:asn [d'iSE] 34,583,622 {54.513} {133.935} 'J'A'tl 449,543 manual} 1251,??? {22,391,221} 1r,929.s4n The issuance of long-term debt [e.g. bonds, loan, leases} provides current financial resou rces to governmental funds, while the repayment of the principal of longsterm debt consumes the current nancial resources of governmental funds Neither transaction, however, has an}? effect on net position Also, governmental funds report the effect of premiums, discounts, and similar items when debt is first issued, whereas these amounts are deferred and amortized in the statement of activities. In the statement of activities, interest is accrued on outstanding bonds, whereas in the governmental funds an interest expenditure is reported when due. The following is the detail of the net effect of these differences in the treatment of long-term debt and related items. Amortization of premium Long-term debt issued, including premiums of $14.06E91? Repayment of long-term debt principal Interest Amortization of discount on revenue bonds Some expenses reported in the statement of activities do not require the use of current financial resources and, therefore. are not reported as expenditures in governmental funds: Accrued employee benefits Other accrued post retirement benets Claims and judgments Pension expense - IPERS Pension expense - MFPRSI Internal service funds are used by management to charge the costs of various activities internall}P to individual funds. The net income of certain activities of internal service funds is reported with governmental activities. Change in internal service fund allocations to business-type activities lChange in net position of governmental activities 62311114 {153,954,45'2} 10:19:05,513 124.3% (mm: {55,324,638} {3,341,101}. {722,960} [3,335,4n} {amass {11,323.1111} {mascara} 2,136,869 13321970 $ seasons

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Accounting Questions!