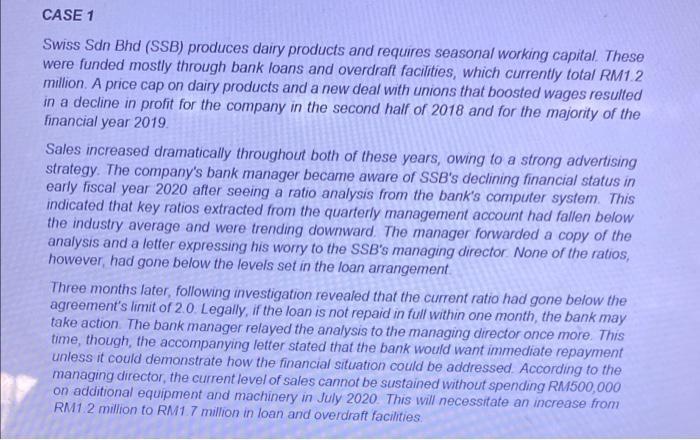

CASE 1 Swiss Sdn Bhd (SSB) produces dairy products and requires seasonal working capital. These were...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

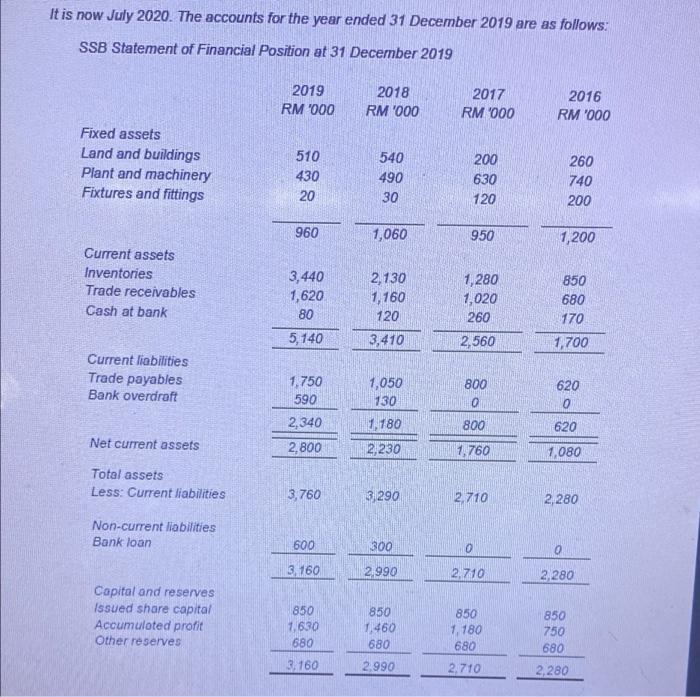

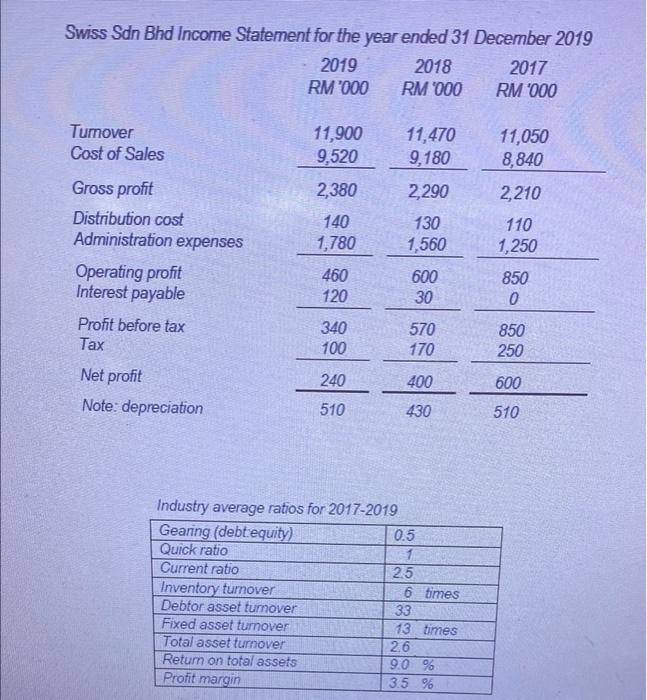

CASE 1 Swiss Sdn Bhd (SSB) produces dairy products and requires seasonal working capital. These were funded mostly through bank loans and overdraft facilities, which currently total RM1.2 million. A price cap on dairy products and a new deal with unions that boosted wages resulted in a decline in profit for the company in the second half of 2018 and for the majority of the financial year 2019. Sales increased dramatically throughout both of these years, owing to a strong advertising strategy. The company's bank manager became aware of SSB's declining financial status in early fiscal year 2020 after seeing a ratio analysis from the bank's computer system. This indicated that key ratios extracted from the quarterly management account had fallen below the industry average and were trending downward. The manager forwarded a copy of the analysis and a letter expressing his worry to the SSB's managing director None of the ratios, however, had gone below the levels set in the loan arrangement Three months later, following investigation revealed that the current ratio had gone below the agreement's limit of 2.0. Legally, if the loan is not repaid in full within one month, the bank may take action. The bank manager relayed the analysis to the managing director once more. This time, though, the accompanying letter stated that the bank would want immediate repayment unless it could demonstrate how the financial situation could be addressed. According to the managing director, the current level of sales cannot be sustained without spending RM500,000 on additional equipment and machinery in July 2020. This will necessitate an increase from RM1.2 million to RM1.7 million in loan and overdraft facilities. It is now July 2020. The accounts for the year ended 31 December 2019 are as follows: SSB Statement of Financial Position at 31 December 2019 Fixed assets Land and buildings Plant and machinery Fixtures and fittings Current assets Inventories Trade receivables Cash at bank Current liabilities Trade payables Bank overdraft Net current assets Total assets Less: Current liabilities Non-current liabilities Bank loan Capital and reserves Issued share capital Accumulated profit Other reserves 2019 RM '000 510 430 20 960 3,440 1,620 80 5,140 1,750 590 2,340 2,800 3,760 600 3,160 850 1,630 680 3,160 2018 RM '000 540 490 30 1,060 2,130 1,160 120 3,410 1,050 130 1,180 2,230 3,290 300 2,990 850 1,460 680 2,990 2017 RM '000 200 630 120 950 1,280 1,020 260 2,560 800 800 1,760 2,710 0 2,710 850 1,180 680 2,710 2016 RM '000 260 740 200 1,200 850 680 170 1,700 620 0 620 1,080 2,280 0 2,280 850 750 680 2,280 Swiss Sdn Bhd Income Statement for the year ended 31 December 2019 2019 2018 RM '000 RM '000 Turnover Cost of Sales Gross profit Distribution cost Administration expenses Operating profit Interest payable Profit before tax Tax Net profit Note: depreciation 11,900 9,520 Return on total assets Profit margin 2,380 140 1,780 460 120 340 100 240 510 Industry average ratios for 2017-2019 Gearing (debt equity) Quick ratio Current ratio Inventory turnover Debtor asset turnover Fixed asset turnover Total asset turnover 11,470 9,180 2,290 130 1,560 600 30 570 170 400 430 0.5 1 2.5 6 times 33 13 times 2.6 9.0 % 3.5 % 2017 RM '000 11,050 8,840 2,210 110 1,250 850 0 850 250 600 510 d. If the bank granted the additional loan, could the company pay off the loan by 31 December 2020? Explain. (8 marks) CASE 1 Swiss Sdn Bhd (SSB) produces dairy products and requires seasonal working capital. These were funded mostly through bank loans and overdraft facilities, which currently total RM1.2 million. A price cap on dairy products and a new deal with unions that boosted wages resulted in a decline in profit for the company in the second half of 2018 and for the majority of the financial year 2019. Sales increased dramatically throughout both of these years, owing to a strong advertising strategy. The company's bank manager became aware of SSB's declining financial status in early fiscal year 2020 after seeing a ratio analysis from the bank's computer system. This indicated that key ratios extracted from the quarterly management account had fallen below the industry average and were trending downward. The manager forwarded a copy of the analysis and a letter expressing his worry to the SSB's managing director None of the ratios, however, had gone below the levels set in the loan arrangement Three months later, following investigation revealed that the current ratio had gone below the agreement's limit of 2.0. Legally, if the loan is not repaid in full within one month, the bank may take action. The bank manager relayed the analysis to the managing director once more. This time, though, the accompanying letter stated that the bank would want immediate repayment unless it could demonstrate how the financial situation could be addressed. According to the managing director, the current level of sales cannot be sustained without spending RM500,000 on additional equipment and machinery in July 2020. This will necessitate an increase from RM1.2 million to RM1.7 million in loan and overdraft facilities. It is now July 2020. The accounts for the year ended 31 December 2019 are as follows: SSB Statement of Financial Position at 31 December 2019 Fixed assets Land and buildings Plant and machinery Fixtures and fittings Current assets Inventories Trade receivables Cash at bank Current liabilities Trade payables Bank overdraft Net current assets Total assets Less: Current liabilities Non-current liabilities Bank loan Capital and reserves Issued share capital Accumulated profit Other reserves 2019 RM '000 510 430 20 960 3,440 1,620 80 5,140 1,750 590 2,340 2,800 3,760 600 3,160 850 1,630 680 3,160 2018 RM '000 540 490 30 1,060 2,130 1,160 120 3,410 1,050 130 1,180 2,230 3,290 300 2,990 850 1,460 680 2,990 2017 RM '000 200 630 120 950 1,280 1,020 260 2,560 800 800 1,760 2,710 0 2,710 850 1,180 680 2,710 2016 RM '000 260 740 200 1,200 850 680 170 1,700 620 0 620 1,080 2,280 0 2,280 850 750 680 2,280 Swiss Sdn Bhd Income Statement for the year ended 31 December 2019 2019 2018 RM '000 RM '000 Turnover Cost of Sales Gross profit Distribution cost Administration expenses Operating profit Interest payable Profit before tax Tax Net profit Note: depreciation 11,900 9,520 Return on total assets Profit margin 2,380 140 1,780 460 120 340 100 240 510 Industry average ratios for 2017-2019 Gearing (debt equity) Quick ratio Current ratio Inventory turnover Debtor asset turnover Fixed asset turnover Total asset turnover 11,470 9,180 2,290 130 1,560 600 30 570 170 400 430 0.5 1 2.5 6 times 33 13 times 2.6 9.0 % 3.5 % 2017 RM '000 11,050 8,840 2,210 110 1,250 850 0 850 250 600 510 d. If the bank granted the additional loan, could the company pay off the loan by 31 December 2020? Explain. (8 marks) CASE 1 Swiss Sdn Bhd (SSB) produces dairy products and requires seasonal working capital. These were funded mostly through bank loans and overdraft facilities, which currently total RM1.2 million. A price cap on dairy products and a new deal with unions that boosted wages resulted in a decline in profit for the company in the second half of 2018 and for the majority of the financial year 2019. Sales increased dramatically throughout both of these years, owing to a strong advertising strategy. The company's bank manager became aware of SSB's declining financial status in early fiscal year 2020 after seeing a ratio analysis from the bank's computer system. This indicated that key ratios extracted from the quarterly management account had fallen below the industry average and were trending downward. The manager forwarded a copy of the analysis and a letter expressing his worry to the SSB's managing director None of the ratios, however, had gone below the levels set in the loan arrangement Three months later, following investigation revealed that the current ratio had gone below the agreement's limit of 2.0. Legally, if the loan is not repaid in full within one month, the bank may take action. The bank manager relayed the analysis to the managing director once more. This time, though, the accompanying letter stated that the bank would want immediate repayment unless it could demonstrate how the financial situation could be addressed. According to the managing director, the current level of sales cannot be sustained without spending RM500,000 on additional equipment and machinery in July 2020. This will necessitate an increase from RM1.2 million to RM1.7 million in loan and overdraft facilities. It is now July 2020. The accounts for the year ended 31 December 2019 are as follows: SSB Statement of Financial Position at 31 December 2019 Fixed assets Land and buildings Plant and machinery Fixtures and fittings Current assets Inventories Trade receivables Cash at bank Current liabilities Trade payables Bank overdraft Net current assets Total assets Less: Current liabilities Non-current liabilities Bank loan Capital and reserves Issued share capital Accumulated profit Other reserves 2019 RM '000 510 430 20 960 3,440 1,620 80 5,140 1,750 590 2,340 2,800 3,760 600 3,160 850 1,630 680 3,160 2018 RM '000 540 490 30 1,060 2,130 1,160 120 3,410 1,050 130 1,180 2,230 3,290 300 2,990 850 1,460 680 2,990 2017 RM '000 200 630 120 950 1,280 1,020 260 2,560 800 800 1,760 2,710 0 2,710 850 1,180 680 2,710 2016 RM '000 260 740 200 1,200 850 680 170 1,700 620 0 620 1,080 2,280 0 2,280 850 750 680 2,280 Swiss Sdn Bhd Income Statement for the year ended 31 December 2019 2019 2018 RM '000 RM '000 Turnover Cost of Sales Gross profit Distribution cost Administration expenses Operating profit Interest payable Profit before tax Tax Net profit Note: depreciation 11,900 9,520 Return on total assets Profit margin 2,380 140 1,780 460 120 340 100 240 510 Industry average ratios for 2017-2019 Gearing (debt equity) Quick ratio Current ratio Inventory turnover Debtor asset turnover Fixed asset turnover Total asset turnover 11,470 9,180 2,290 130 1,560 600 30 570 170 400 430 0.5 1 2.5 6 times 33 13 times 2.6 9.0 % 3.5 % 2017 RM '000 11,050 8,840 2,210 110 1,250 850 0 850 250 600 510 d. If the bank granted the additional loan, could the company pay off the loan by 31 December 2020? Explain. (8 marks) CASE 1 Swiss Sdn Bhd (SSB) produces dairy products and requires seasonal working capital. These were funded mostly through bank loans and overdraft facilities, which currently total RM1.2 million. A price cap on dairy products and a new deal with unions that boosted wages resulted in a decline in profit for the company in the second half of 2018 and for the majority of the financial year 2019. Sales increased dramatically throughout both of these years, owing to a strong advertising strategy. The company's bank manager became aware of SSB's declining financial status in early fiscal year 2020 after seeing a ratio analysis from the bank's computer system. This indicated that key ratios extracted from the quarterly management account had fallen below the industry average and were trending downward. The manager forwarded a copy of the analysis and a letter expressing his worry to the SSB's managing director None of the ratios, however, had gone below the levels set in the loan arrangement Three months later, following investigation revealed that the current ratio had gone below the agreement's limit of 2.0. Legally, if the loan is not repaid in full within one month, the bank may take action. The bank manager relayed the analysis to the managing director once more. This time, though, the accompanying letter stated that the bank would want immediate repayment unless it could demonstrate how the financial situation could be addressed. According to the managing director, the current level of sales cannot be sustained without spending RM500,000 on additional equipment and machinery in July 2020. This will necessitate an increase from RM1.2 million to RM1.7 million in loan and overdraft facilities. It is now July 2020. The accounts for the year ended 31 December 2019 are as follows: SSB Statement of Financial Position at 31 December 2019 Fixed assets Land and buildings Plant and machinery Fixtures and fittings Current assets Inventories Trade receivables Cash at bank Current liabilities Trade payables Bank overdraft Net current assets Total assets Less: Current liabilities Non-current liabilities Bank loan Capital and reserves Issued share capital Accumulated profit Other reserves 2019 RM '000 510 430 20 960 3,440 1,620 80 5,140 1,750 590 2,340 2,800 3,760 600 3,160 850 1,630 680 3,160 2018 RM '000 540 490 30 1,060 2,130 1,160 120 3,410 1,050 130 1,180 2,230 3,290 300 2,990 850 1,460 680 2,990 2017 RM '000 200 630 120 950 1,280 1,020 260 2,560 800 800 1,760 2,710 0 2,710 850 1,180 680 2,710 2016 RM '000 260 740 200 1,200 850 680 170 1,700 620 0 620 1,080 2,280 0 2,280 850 750 680 2,280 Swiss Sdn Bhd Income Statement for the year ended 31 December 2019 2019 2018 RM '000 RM '000 Turnover Cost of Sales Gross profit Distribution cost Administration expenses Operating profit Interest payable Profit before tax Tax Net profit Note: depreciation 11,900 9,520 Return on total assets Profit margin 2,380 140 1,780 460 120 340 100 240 510 Industry average ratios for 2017-2019 Gearing (debt equity) Quick ratio Current ratio Inventory turnover Debtor asset turnover Fixed asset turnover Total asset turnover 11,470 9,180 2,290 130 1,560 600 30 570 170 400 430 0.5 1 2.5 6 times 33 13 times 2.6 9.0 % 3.5 % 2017 RM '000 11,050 8,840 2,210 110 1,250 850 0 850 250 600 510 d. If the bank granted the additional loan, could the company pay off the loan by 31 December 2020? Explain. (8 marks) CASE 1 Swiss Sdn Bhd (SSB) produces dairy products and requires seasonal working capital. These were funded mostly through bank loans and overdraft facilities, which currently total RM1.2 million. A price cap on dairy products and a new deal with unions that boosted wages resulted in a decline in profit for the company in the second half of 2018 and for the majority of the financial year 2019. Sales increased dramatically throughout both of these years, owing to a strong advertising strategy. The company's bank manager became aware of SSB's declining financial status in early fiscal year 2020 after seeing a ratio analysis from the bank's computer system. This indicated that key ratios extracted from the quarterly management account had fallen below the industry average and were trending downward. The manager forwarded a copy of the analysis and a letter expressing his worry to the SSB's managing director None of the ratios, however, had gone below the levels set in the loan arrangement Three months later, following investigation revealed that the current ratio had gone below the agreement's limit of 2.0. Legally, if the loan is not repaid in full within one month, the bank may take action. The bank manager relayed the analysis to the managing director once more. This time, though, the accompanying letter stated that the bank would want immediate repayment unless it could demonstrate how the financial situation could be addressed. According to the managing director, the current level of sales cannot be sustained without spending RM500,000 on additional equipment and machinery in July 2020. This will necessitate an increase from RM1.2 million to RM1.7 million in loan and overdraft facilities. It is now July 2020. The accounts for the year ended 31 December 2019 are as follows: SSB Statement of Financial Position at 31 December 2019 Fixed assets Land and buildings Plant and machinery Fixtures and fittings Current assets Inventories Trade receivables Cash at bank Current liabilities Trade payables Bank overdraft Net current assets Total assets Less: Current liabilities Non-current liabilities Bank loan Capital and reserves Issued share capital Accumulated profit Other reserves 2019 RM '000 510 430 20 960 3,440 1,620 80 5,140 1,750 590 2,340 2,800 3,760 600 3,160 850 1,630 680 3,160 2018 RM '000 540 490 30 1,060 2,130 1,160 120 3,410 1,050 130 1,180 2,230 3,290 300 2,990 850 1,460 680 2,990 2017 RM '000 200 630 120 950 1,280 1,020 260 2,560 800 800 1,760 2,710 0 2,710 850 1,180 680 2,710 2016 RM '000 260 740 200 1,200 850 680 170 1,700 620 0 620 1,080 2,280 0 2,280 850 750 680 2,280 Swiss Sdn Bhd Income Statement for the year ended 31 December 2019 2019 2018 RM '000 RM '000 Turnover Cost of Sales Gross profit Distribution cost Administration expenses Operating profit Interest payable Profit before tax Tax Net profit Note: depreciation 11,900 9,520 Return on total assets Profit margin 2,380 140 1,780 460 120 340 100 240 510 Industry average ratios for 2017-2019 Gearing (debt equity) Quick ratio Current ratio Inventory turnover Debtor asset turnover Fixed asset turnover Total asset turnover 11,470 9,180 2,290 130 1,560 600 30 570 170 400 430 0.5 1 2.5 6 times 33 13 times 2.6 9.0 % 3.5 % 2017 RM '000 11,050 8,840 2,210 110 1,250 850 0 850 250 600 510 d. If the bank granted the additional loan, could the company pay off the loan by 31 December 2020? Explain. (8 marks) CASE 1 Swiss Sdn Bhd (SSB) produces dairy products and requires seasonal working capital. These were funded mostly through bank loans and overdraft facilities, which currently total RM1.2 million. A price cap on dairy products and a new deal with unions that boosted wages resulted in a decline in profit for the company in the second half of 2018 and for the majority of the financial year 2019. Sales increased dramatically throughout both of these years, owing to a strong advertising strategy. The company's bank manager became aware of SSB's declining financial status in early fiscal year 2020 after seeing a ratio analysis from the bank's computer system. This indicated that key ratios extracted from the quarterly management account had fallen below the industry average and were trending downward. The manager forwarded a copy of the analysis and a letter expressing his worry to the SSB's managing director None of the ratios, however, had gone below the levels set in the loan arrangement Three months later, following investigation revealed that the current ratio had gone below the agreement's limit of 2.0. Legally, if the loan is not repaid in full within one month, the bank may take action. The bank manager relayed the analysis to the managing director once more. This time, though, the accompanying letter stated that the bank would want immediate repayment unless it could demonstrate how the financial situation could be addressed. According to the managing director, the current level of sales cannot be sustained without spending RM500,000 on additional equipment and machinery in July 2020. This will necessitate an increase from RM1.2 million to RM1.7 million in loan and overdraft facilities. It is now July 2020. The accounts for the year ended 31 December 2019 are as follows: SSB Statement of Financial Position at 31 December 2019 Fixed assets Land and buildings Plant and machinery Fixtures and fittings Current assets Inventories Trade receivables Cash at bank Current liabilities Trade payables Bank overdraft Net current assets Total assets Less: Current liabilities Non-current liabilities Bank loan Capital and reserves Issued share capital Accumulated profit Other reserves 2019 RM '000 510 430 20 960 3,440 1,620 80 5,140 1,750 590 2,340 2,800 3,760 600 3,160 850 1,630 680 3,160 2018 RM '000 540 490 30 1,060 2,130 1,160 120 3,410 1,050 130 1,180 2,230 3,290 300 2,990 850 1,460 680 2,990 2017 RM '000 200 630 120 950 1,280 1,020 260 2,560 800 800 1,760 2,710 0 2,710 850 1,180 680 2,710 2016 RM '000 260 740 200 1,200 850 680 170 1,700 620 0 620 1,080 2,280 0 2,280 850 750 680 2,280 Swiss Sdn Bhd Income Statement for the year ended 31 December 2019 2019 2018 RM '000 RM '000 Turnover Cost of Sales Gross profit Distribution cost Administration expenses Operating profit Interest payable Profit before tax Tax Net profit Note: depreciation 11,900 9,520 Return on total assets Profit margin 2,380 140 1,780 460 120 340 100 240 510 Industry average ratios for 2017-2019 Gearing (debt equity) Quick ratio Current ratio Inventory turnover Debtor asset turnover Fixed asset turnover Total asset turnover 11,470 9,180 2,290 130 1,560 600 30 570 170 400 430 0.5 1 2.5 6 times 33 13 times 2.6 9.0 % 3.5 % 2017 RM '000 11,050 8,840 2,210 110 1,250 850 0 850 250 600 510 d. If the bank granted the additional loan, could the company pay off the loan by 31 December 2020? Explain. (8 marks)

Expert Answer:

Answer rating: 100% (QA)

Solution As per managing director by giving entre loan the company able to maintai... View the full answer

Related Book For

Posted Date:

Students also viewed these finance questions

-

Consider the following events related Mr. Masood, the owner of a retail shop in Ibri. 1 Masood gifted a watch to his staff Ms. Zainab on the occasion of her marriage. 2 Paid rent for the staff...

-

Office supplies were sold by Janer's cleaning service at cost to another repair shop, with cash received. Which of the following entries for Janer's Cleaning Service records this transaction? 1.Dr...

-

a Retired bonds payable at maturity date by issuing common shares 143000 b Sold the longterm investments for cash c Sold plant assets for cash cost 554400 twothirds depreciated d Purchased plant...

-

Suppose that In Example 18.6 the electrical firm does not have enough prior information regarding the population mean length of life to be able to assume a normal distribution for p. The firm...

-

Consider the system described where a communication system transmits a square pulse of width t1. In that example, it was found that the matched filter can be implemented as a finite time integrator...

-

Using acetonitrile (CH 3 CN) and CO 2 as your only sources of carbons, identify how you could prepare each of the following compounds: a. b. c. d.

-

Describe some computer assisted substantive tests an auditor might apply to accounts receivable.

-

Salamander Inc. is a food processing company that operates divisions in three major lines of food products: cereals, frozen fish, and candy. On 13 September 20X1, the Board of Directors voted to put...

-

define a K-NN model IN PYTHON please 3. Define a K-NN model (1% total grade) Write code to define a K-NN regression model with K-5 and the neighbors are weighted by the inverse of their distance....

-

Reverend Peter Wilson qualifies as a minister for income tax purposes. He receives a $75,000 annual salary and a $32,000 housing allowance. He pays $24,000 (including utilities) per year for the...

-

Asuncion Alcala, to be able to guide the accountancy students in their pursuits for CPA glory, established the AA Tutorial Services. On May 1, 2020, she contributed P70,000 as investment to start the...

-

Free cash flow valuation Lin is evaluating the potential purchase of a small business with no debt or preferred stock that is currently generating 32,000 of free cash flow 1FCF0 = +32,0002 every...

-

The sales team of a large car dealership in Seattle consists of the following individuals: A customer visiting the dealership randomly chooses one of the salespersons to discuss the purchase of a new...

-

A company manages three different mutual funds. Let \(A_{\mathrm{i}}\) be the event that the ith mutual fund increases in value on a given day. Probabilities of various events relating to the mutual...

-

A large-scale firm specializing in providing temporary secretarial services to corporate clients has completed a study of the main reason why secretaries become dissatisfied with their work...

-

SUPERCOMP, a retail computer store, sells personal computers and printers. The number of computers and printers sold on any given day varies, with the probabilities of the various possible sales...

-

Complete the code in ArrMin.asm . Inputs: R1 contains the RAM address of the first element in the array and the R2 contains the length of the array. Output: Final answer to R0. Write 7 test cases...

-

Consider the sections of two circuits illustrated above. Select True or False for all statements.After connecting a and b to a battery, the voltage across R1 always equals the voltage across R2.Rcd...

-

A manager at an airline raised concerns about the airlines pay practices. She also complained that the performance appraisal process discriminated against female employees. After a number of run-ins...

-

A fifty-three-year old director of an assisted living facility was terminated. Top managers regularly made statements such as Silver Oak should be a youth oriented company, there was no room for dead...

-

The married owner of a company touched and kissed a female salesperson at work, made comments about oral sex, and suggested that they be alone together. A few months later the woman began making...

-

All prototypes must be ___________ in nature. (a) Evolutionary (b) Conceptual (c) Physical (d) None of these

-

_____________ is an iterative tool for project development which produces a live working model of the system. (a) Function (b) Prototype (c) Module (d) Class

-

It is the responsibility of __________ to build prototype with suitable tool. (a) End users (b) Systems Analyst (c) Programmers (d) Managers

Study smarter with the SolutionInn App