Question: A share price X(t) evolves according to the It process dX cXdW with initial condition X(0) = Xo, where c is a constant and dW

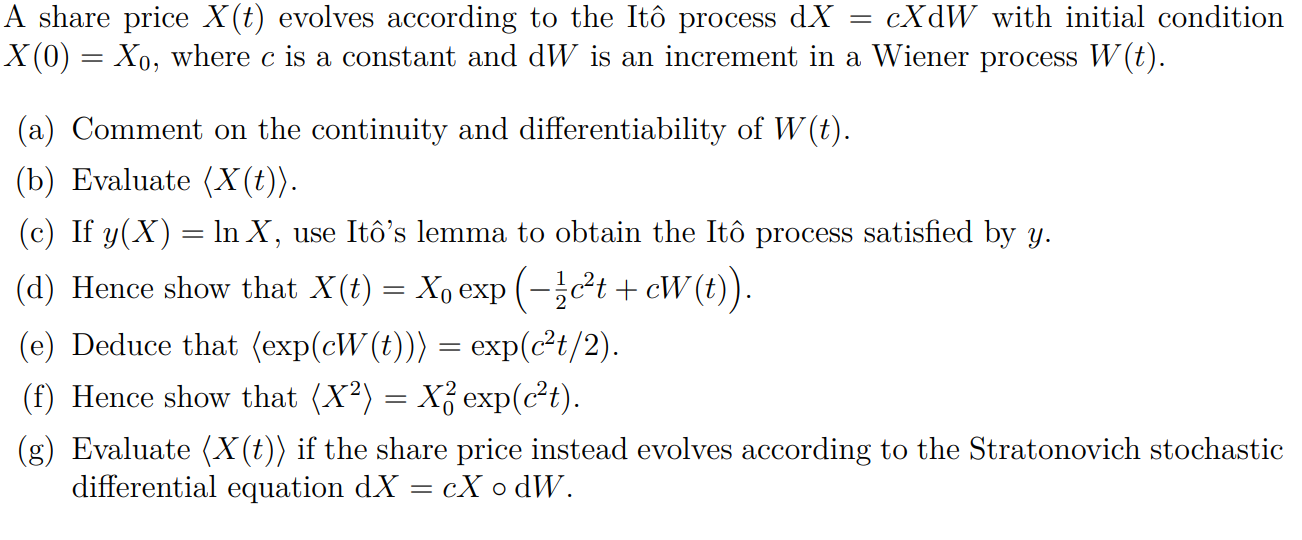

A share price X(t) evolves according to the It process dX cXdW with initial condition X(0) = Xo, where c is a constant and dW is an increment in a Wiener process W(t). = = (a) Comment on the continuity and differentiability of W(t). (b) Evaluate (X(t)). (c) If y(X) = ln X, use It's lemma to obtain the It process satisfied by y. (d) Hence show that X(t) = Xo exp(-4c+ cW (t)). (e) Deduce that (exp(cW (t))) = exp(ct/2). (f) Hence show that (X2) = Xz exp(ct). (g) Evaluate (X(t)) if the share price instead evolves according to the Stratonovich stochastic differential equation dX = cX odW. = = = A share price X(t) evolves according to the It process dX cXdW with initial condition X(0) = Xo, where c is a constant and dW is an increment in a Wiener process W(t). = = (a) Comment on the continuity and differentiability of W(t). (b) Evaluate (X(t)). (c) If y(X) = ln X, use It's lemma to obtain the It process satisfied by y. (d) Hence show that X(t) = Xo exp(-4c+ cW (t)). (e) Deduce that (exp(cW (t))) = exp(ct/2). (f) Hence show that (X2) = Xz exp(ct). (g) Evaluate (X(t)) if the share price instead evolves according to the Stratonovich stochastic differential equation dX = cX odW. = = =

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts