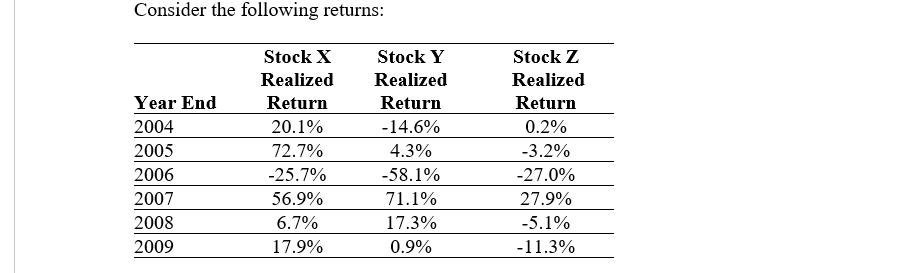

Question 1 : Calculate the following: 1. covariance between Stock Y's and Stock Z's returns. 2. correlation

Question:

Question 1 :

Calculate the following:

1. covariance between Stock Y's and Stock Z's returns.

2. correlation between Stock Y's and Stock Z's returns.

3. variance on a portfolio that is made up of equal investments in Stock Y and Stock Z stock.

4. Briefly explain why the covariance of a security with the rest of a well-diversified portfolio is a more appropriate measure of the risk of the security than the security's variance.

5. If a portfolio has a positive investment in every asset, can the standard deviation on the portfolio be less than that on every asset in the portfolio? What about the portfolio beta?

6. Is it possible that a risky asset could have a beta of zero? Explain. Based on the CAPM, what is the expected return on such an asset? Is it possible that a risky asset could have a negative beta? What does the CAPM predict about the expected return on such an asset? Can you give an explanation for your answer?

Expert Answer:

Step 12 1 Covariance between Stock Y and Stock Z Stock Y Stock Z Product of Year End Return De... View the full answer