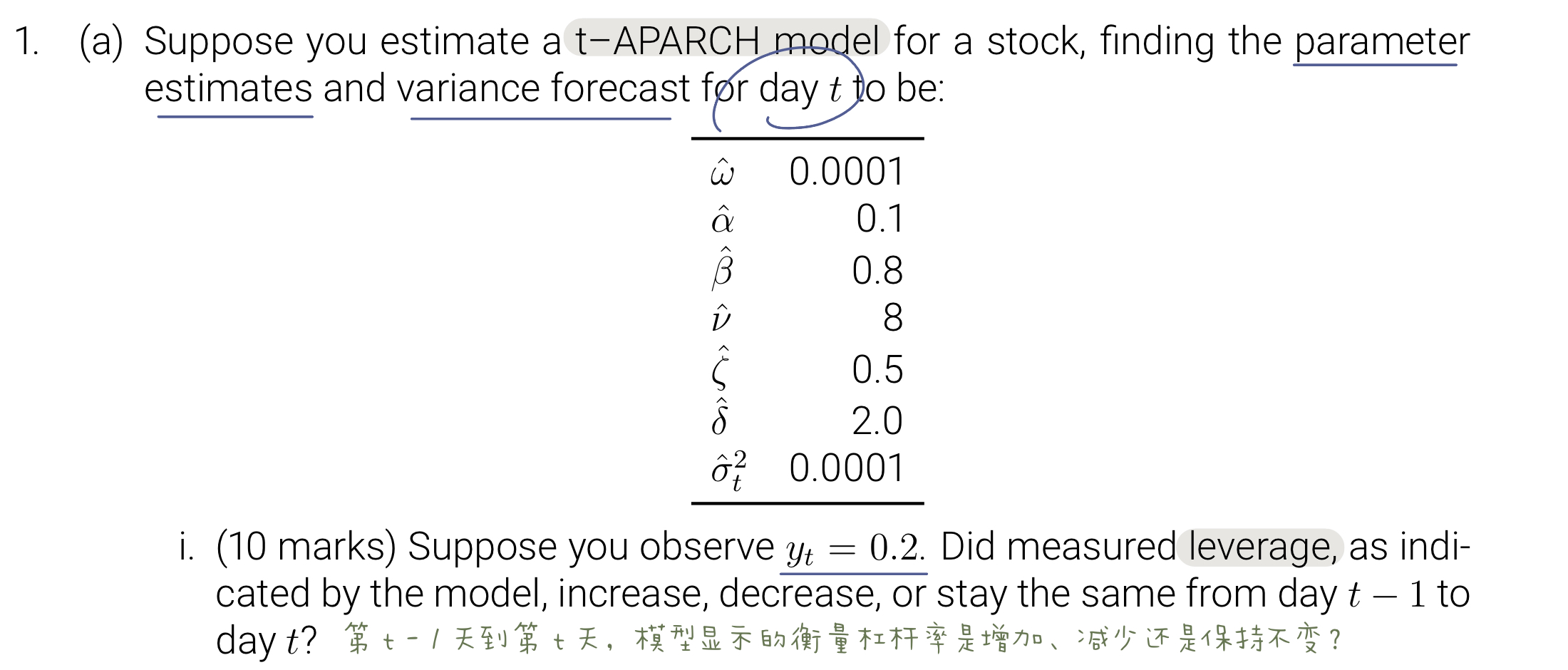

Question: ( a ) Suppose you estimate a t - APARCH model for a stock, finding the parameter estimates and variance forecast for day t to

a Suppose you estimate a tAPARCH model for a stock, finding the parameter estimates and variance forecast for day to be: i marks Suppose you observe Did measured leverage, as indi cated by the model, increase, decrease, or stay the same from day to day

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock