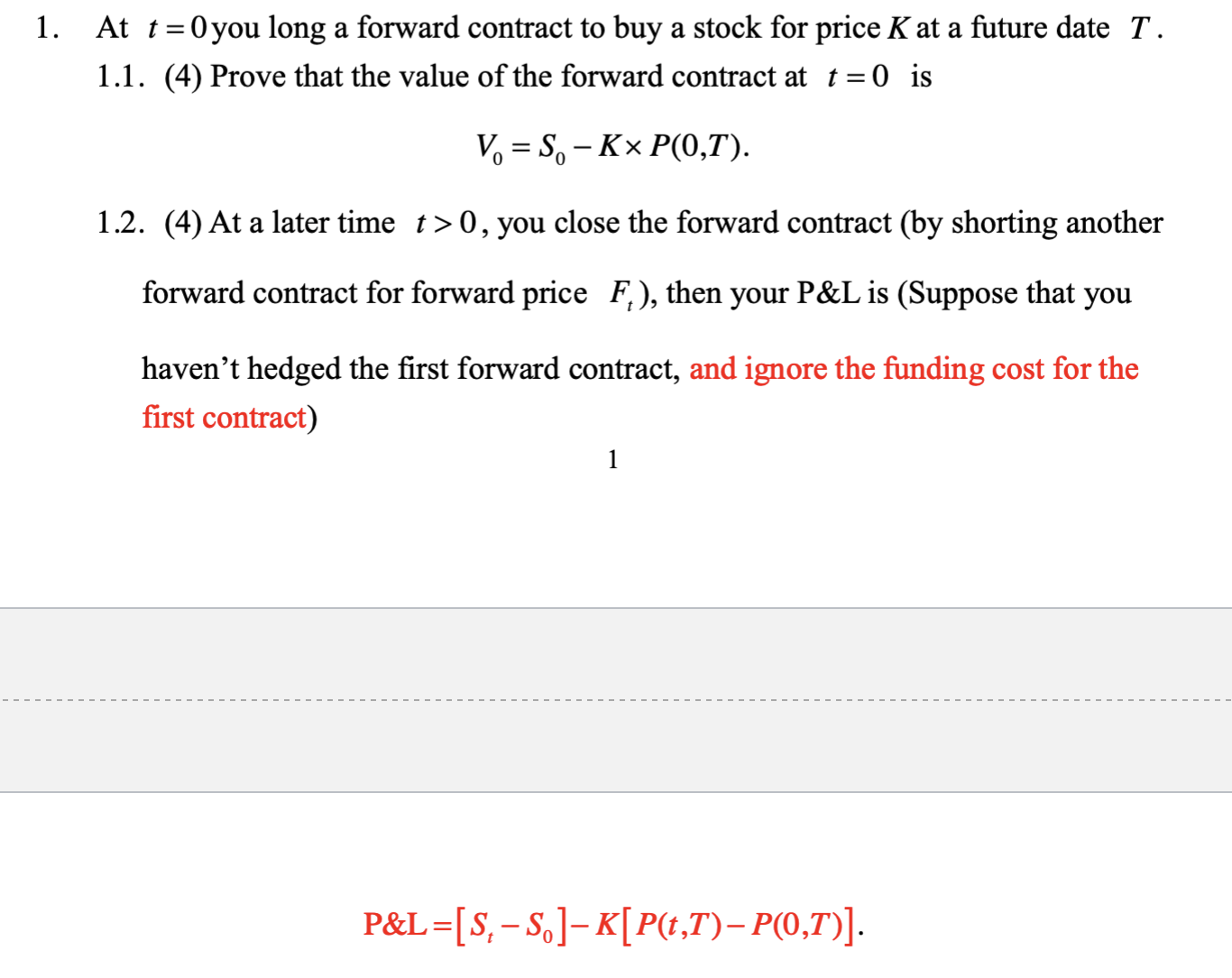

Question: A t t = 0 you long a forward contract t o buy a stock for price K a t a future date T .

you long a forward contract buy a stock for price a future date

Prove that the value the forward contract

a later time & that you

haven't hedged the first forward contract, and ignore the funding cost for the

first contract

&

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock