Question: a time series problem A time series r, is modelled with an AR(2) process with intercept, as follows: It = 6+010-1+ 020-2 + et where

a time series problem

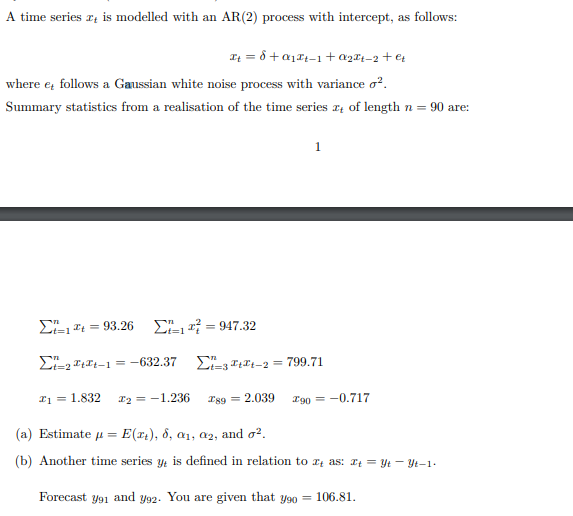

A time series r, is modelled with an AR(2) process with intercept, as follows: It = 6+010-1+ 020-2 + et where er follows a Gaussian white noise process with variance o'. Summary statistics from a realisation of the time series r, of length n = 90 are: ELIT = 93.26 E x7 =947.32 1=2 0+It-1 = -632.37 _ _Text-2 = 799.71 1 = 1.832 $2 = -1.236 T89 = 2.039 Cgo = -0.717 (a) Estimate u = E(x,), 6, 01, 02, and o. (b) Another time series y is defined in relation to It as: It = yt - yt-1. Forecast you and y92. You are given that yo = 106.81

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock