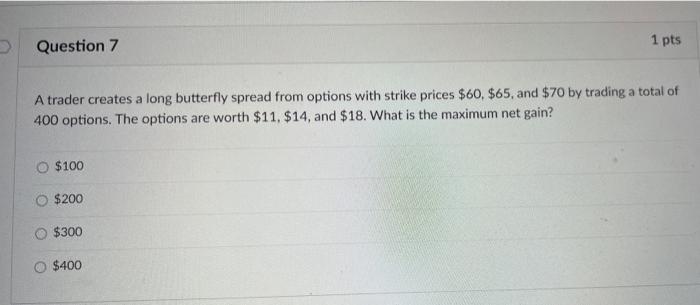

Question: A trader creates a long butterfly spread from options with strike prices $60,$65, and $70 by trading a total of 400 options. The options are

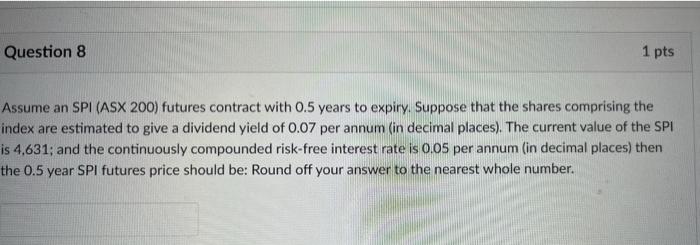

A trader creates a long butterfly spread from options with strike prices $60,$65, and $70 by trading a total of 400 options. The options are worth $11,$14, and $18. What is the maximum net gain? $100 $200 $300 $400 Assume an SPI (ASX 200) futures contract with 0.5 years to expiry. Suppose that the shares comprising the index are estimated to give a dividend yield of 0.07 per annum (in decimal places). The current value of the SPI is 4,631 ; and the continuously compounded risk-free interest rate is 0.05 per annum (in decimal places) then the 0.5 year SPI futures price should be: Round off your answer to the nearest whole number. A trader creates a long butterfly spread from options with strike prices $60,$65, and $70 by trading a total of 400 options. The options are worth $11,$14, and $18. What is the maximum net gain? $100 $200 $300 $400 Assume an SPI (ASX 200) futures contract with 0.5 years to expiry. Suppose that the shares comprising the index are estimated to give a dividend yield of 0.07 per annum (in decimal places). The current value of the SPI is 4,631 ; and the continuously compounded risk-free interest rate is 0.05 per annum (in decimal places) then the 0.5 year SPI futures price should be: Round off your answer to the nearest whole number

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts