A trader has entered into a forward rate agreement in which it will receive 4.5% based on

Fantastic news! We've Found the answer you've been seeking!

Question:

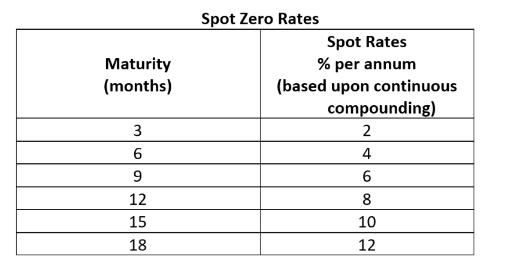

A trader has entered into a forward rate agreement in which it will receive 4.5% based on quarterly compounding for a three-month period starting in 9 months. The notional value of the forward rate agreement is $10,000,000. Note that the spot zero rates in the table below are based upon continuous compounding.

a. Given the data below, what is the value of a forward rate agreement?

b. Provide two ways in which the trader can hedge the risk of the forward rate agreement?

Expert Answer:

The 9 months period will start after three months It means it will be 12 months time from now onw... View the full answer

Related Book For

Financial Markets and Institutions

ISBN: 978-0077861667

6th edition

Authors: Anthony Saunders , Marcia Cornett

Posted Date: