Question: A. True or False ? (max 20 points) B. Standard Question 1 (max 30 points) We assume a non-dividend paying stock of a company called

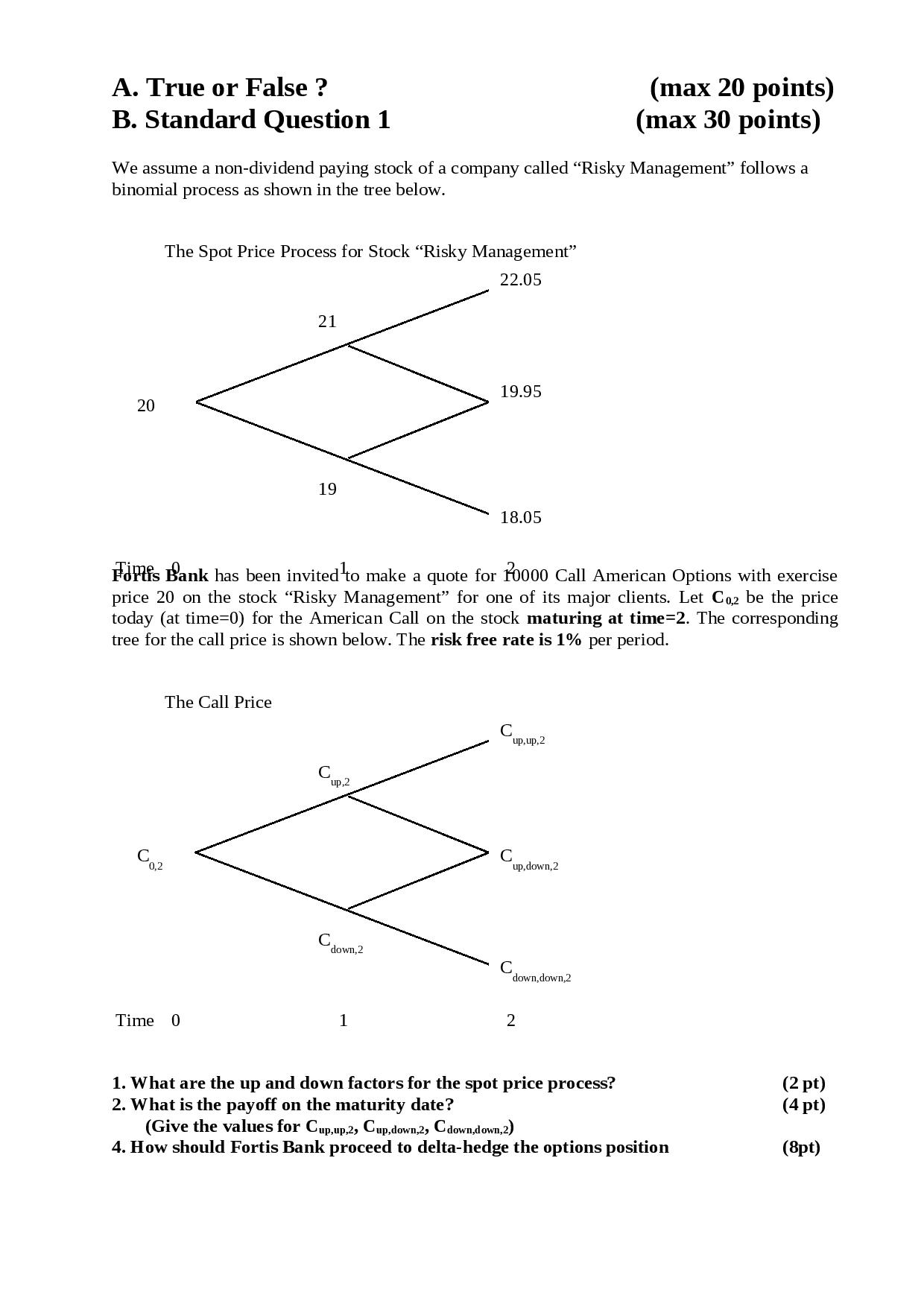

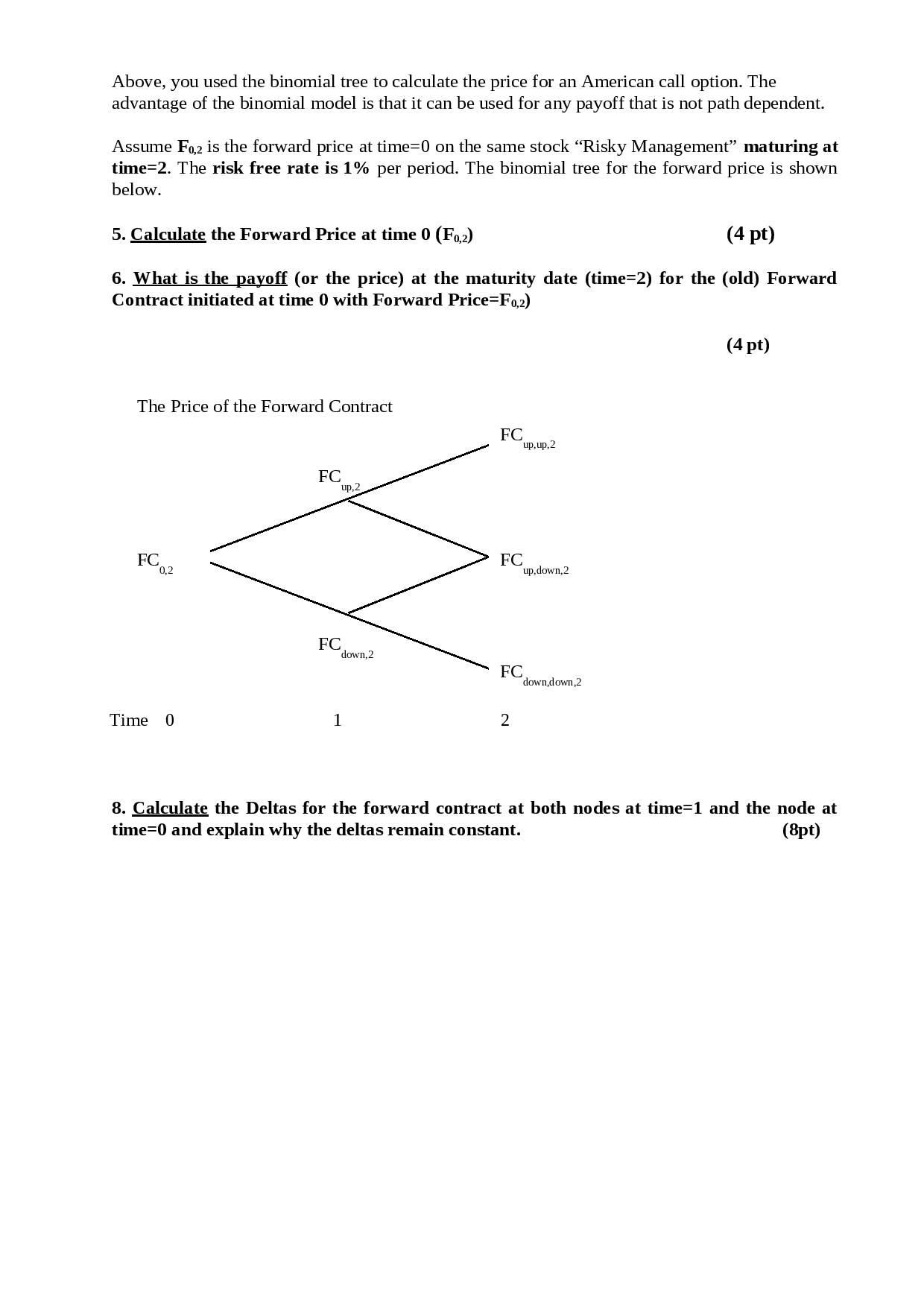

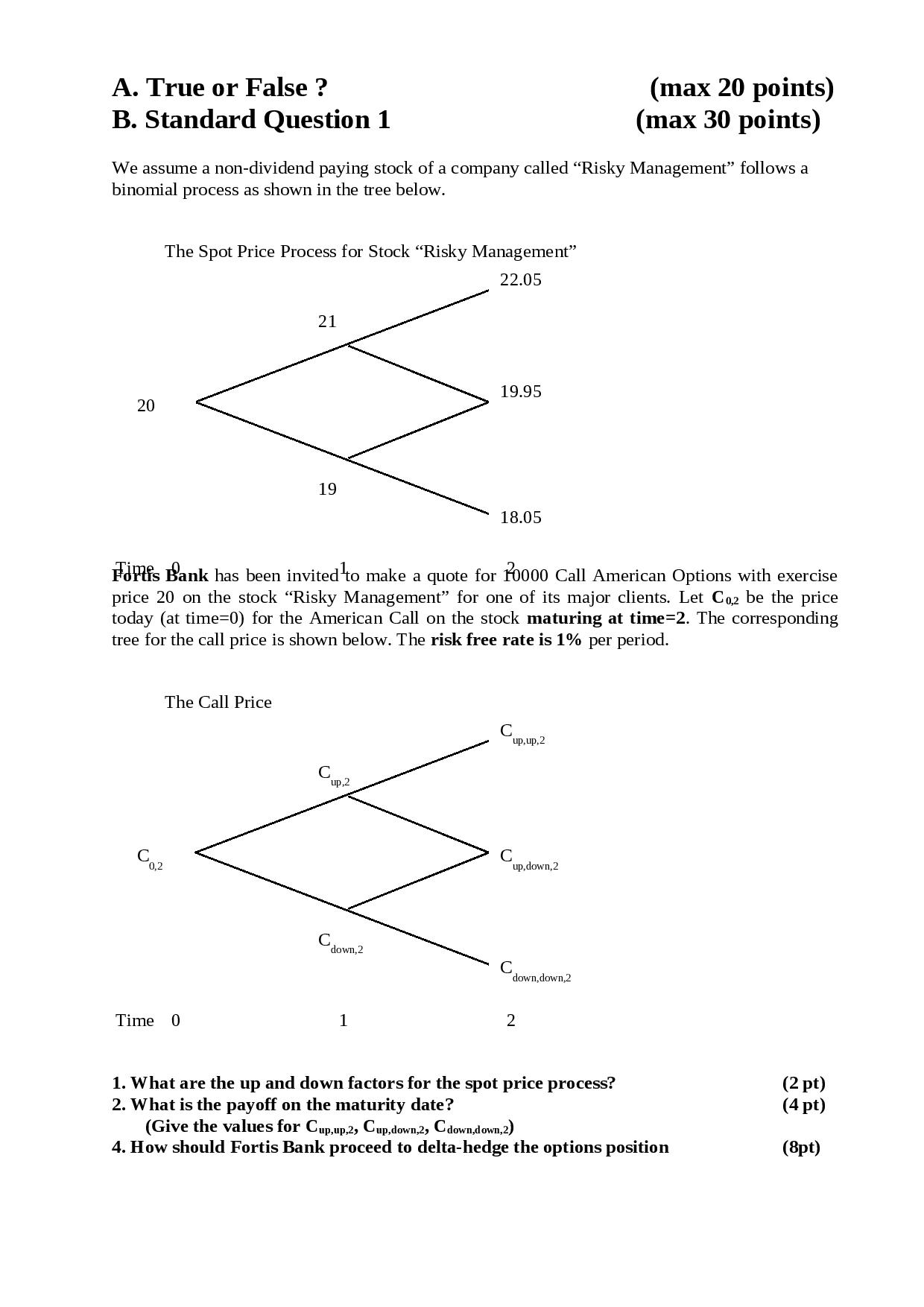

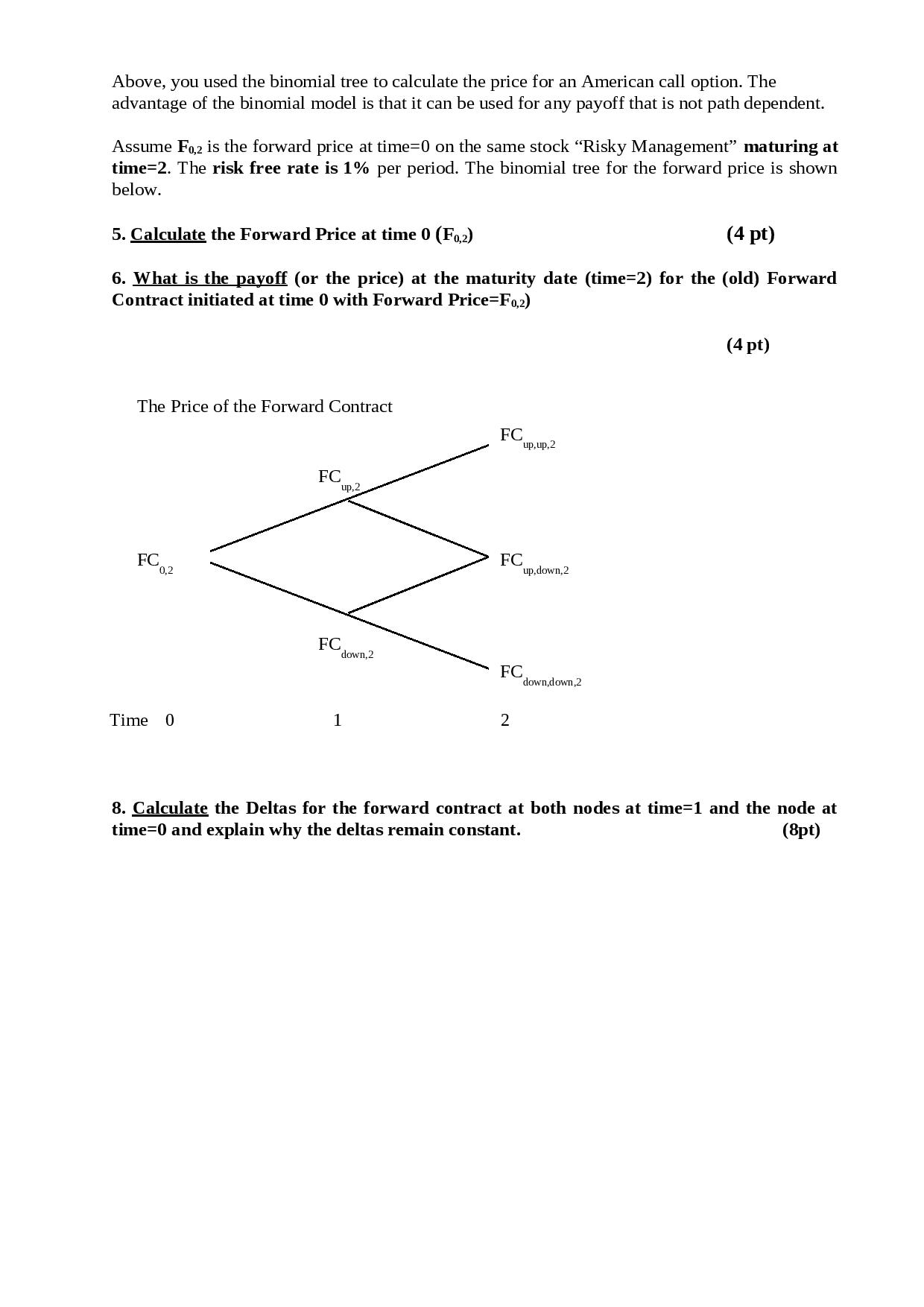

A. True or False ? (max 20 points) B. Standard Question 1 (max 30 points) We assume a non-dividend paying stock of a company called \"Risky Management\" follows a binomial process as shown in the tree below. The Spot Price Process for Stock \"Risky Management\" 22.05 2 1 19.95 20 19 18.05 Edgii's lgank has been invitedlto make a quote for 0000 Call American Options with exercise price 20 on the stock \"Risky Management\" for one of its major clients. Let (10,: be the price today (at time=0) for the American Call on the stock maturing at time=2. The corresponding tree for the call price is shown below. The risk free rate is 1% per period. The Call Price C 0,2 Time 0 1 2 1. What are the up and down factors for the spot price process? (2 pt) 2. What is the payoff on the maturity date? (4 pt) (Give the values for Cumpg, Cup,dm_2, Cdmmg) 4. How should Fortis Bank proceed to deIta hedge the options position (Bpt) Above, you used the binomial tree to calculate the price for an American call option. The advantage of the binomial model is that it can be used for any payoff that is not path dependent. Assume Fo,2 is the forward price at time:0 on the same stock \"Risky Management\" maturing at time=2. The risk free rate is 1% per period. The binomial tree for the forward price is shown below. 5. Calculate the Forward Price at time 0 (Fu) (4 pt) 6. What is the payoff [or the price) at the maturity date (time=2) for the (old) Forward Contract initiated at time 0 with Forward Price=Fo,2) (4 pt) The Price of the Forward Contract FCHIWP.2 FC 1113.2 PC. FC 0.2 up.down.2 chown,2 FCduwn,doum,2 Time 0 1 2 8. Calculate the Deltas for the forward contract at both nodes at time=1 and the node at time=0 and explain why the deltas remain constant. (8pt)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts