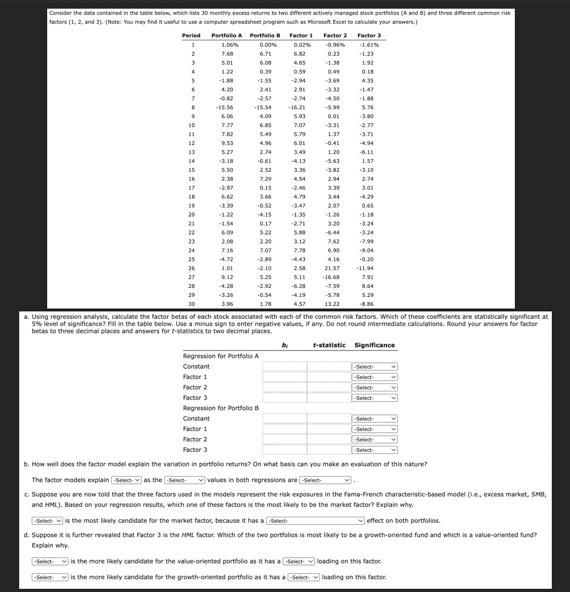

Question: a. Using regression analysis, calculate the factor deras or eacn swock assocosed with each of the commen nax ractors. wmich of these coellicienss are statistically

a. Using regression analysis, calculate the factor deras or eacn swock assocosed with each of the commen nax ractors. wmich of these coellicienss are statistically significant at 5 Sw level of signifeamcet fil in the table below. Use a minus sigs to enter negutive values, if any. Do not round intermediabe calculations. Ppound yeur answers for factor betad to three secimal ptaces and answers for t-statiotics to two decimal places. b. How wel does the factor mosel explain the variation in portiolio returns? On what basis can you make an cvaluation of this nature? The factor models eapiain as the walyes is both regresisns are c. Suppose you are now told that the three factors used in the models regresent the risk exposures in the Fama-French eharacteristic-based moder puef, eacess market, sMe, and HML). Based an your regression results, which ose of these factors is the most ikely to be the market factor? Explain why. is the most likely candidate for the market factoc, because it has a effect on both portfolios. d. Suppose is is further revealed that factor 3 is the red foctor which of the two portolios is most ikely to be a growth-ariested fund and which it a value-oriented fund? Explain why. is the more likely candifate for the vake-oriented portfolis as it has a losding on this factor. W the more lkeily candidate for the growth-griented portfolig as is has a losding on this tactor. a. Using regression analysis, calculate the factor deras or eacn swock assocosed with each of the commen nax ractors. wmich of these coellicienss are statistically significant at 5 Sw level of signifeamcet fil in the table below. Use a minus sigs to enter negutive values, if any. Do not round intermediabe calculations. Ppound yeur answers for factor betad to three secimal ptaces and answers for t-statiotics to two decimal places. b. How wel does the factor mosel explain the variation in portiolio returns? On what basis can you make an cvaluation of this nature? The factor models eapiain as the walyes is both regresisns are c. Suppose you are now told that the three factors used in the models regresent the risk exposures in the Fama-French eharacteristic-based moder puef, eacess market, sMe, and HML). Based an your regression results, which ose of these factors is the most ikely to be the market factor? Explain why. is the most likely candidate for the market factoc, because it has a effect on both portfolios. d. Suppose is is further revealed that factor 3 is the red foctor which of the two portolios is most ikely to be a growth-ariested fund and which it a value-oriented fund? Explain why. is the more likely candifate for the vake-oriented portfolis as it has a losding on this factor. W the more lkeily candidate for the growth-griented portfolig as is has a losding on this tactor

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts