Question: A. What are the appropriate allocaton rates? B. Use an allocation table similiar to Exhibit 6.7 (I have given it in a second photo). To

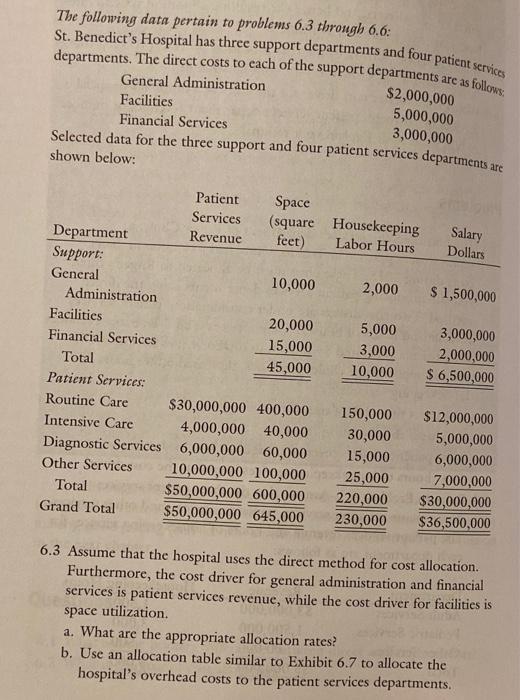

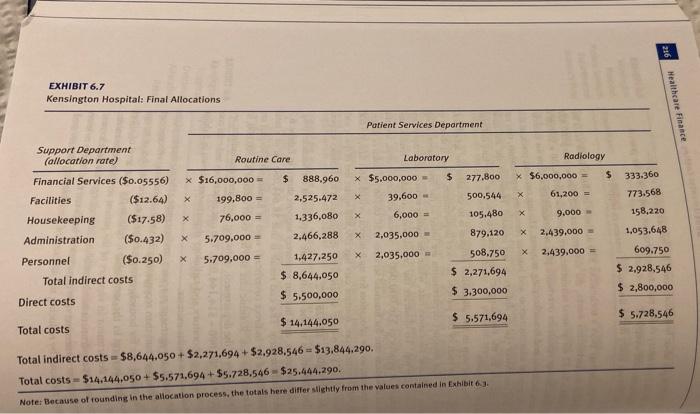

The following data pertain to problems 6.3 through 6.6: St. Benedict's Hospital has three support departments and four patient services departments. The direct costs to each of the support departments are as follows: General Administration $2,000,000 Facilities 5,000,000 Financial Services 3,000,000 Selected data for the three support and four patient services departments are shown below: Patient Space Services (square Housekeeping Salary Department Revenue feet) Labor Hours Dollars Support: General 10,000 2,000 $ 1,500,000 Administration Facilities 20,000 5,000 3,000,000 Financial Services 15,000 3,000 2,000,000 Total 45,000 10,000 $ 6,500,000 Patient Services: Routine Care $30,000,000 400,000 150,000 $12,000,000 Intensive Care 4,000,000 40,000 30,000 5,000,000 Diagnostic Services 6,000,000 60,000 15,000 6,000,000 Other Services 10,000,000 100,000 25,000 7,000,000 Total $50,000,000 600,000 220,000 $30,000,000 Grand Total $50,000,000 645,000 230,000 $36,500,000 6.3 Assume that the hospital uses the direct method for cost allocation. Furthermore, the cost driver for general administration and financial services is patient services revenue, while the cost driver for facilities is space utilization. a. What are the appropriate allocation rates? b. Use an allocation table similar to Exhibit 6.7 to allocate the hospital's overhead costs to the patient services departments, EXHIBIT 6.7 Kensington Hospital: Final Allocations Healthcare Finance Patient Services Department Routine Care Laboratory $ $ 277.800 888.960 2.525.472 * $16,000,000 = X 199.800 = X 76,000 = Support Department (allocation rate) Financial Services ($0.05556) Facilities ($12.64) Housekeeping ($17.58) Administration ($0.432) Personnel ($0.250) Total Indirect costs Radiology x $6,000,000 = $ X 61,200 X $5,000,000 39,600 X 6,000 = 500.544 105,480 333.360 773.568 158,220 1,053,648 9.000 1.336,080 2.466,288 X X X 879.120 2,035,000 2.439,000 5.709.000 5.709,000 = X X 1,427,250 X 2,439,000 = 2,035.000 $ 8,644.050 508.750 $ 2,271,694 $ 3.300,000 609.750 $ 2,928,546 $ 2,800,000 Direct costs $ 5.500,000 $ 14,144.050 $ 5.571,694 $ 5.728,546 Total costs Total indirect costs - $8,644.050 + $2,271,694 $2,928,546 = $13.844.290. Total costs - $14,144.050 + $5.571.694 + $5.728,546 - $25.444.290. Note: Because of rounding in the allocation process, the totals here differ slightly from the values contained in Exhibit 6.3

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts