Question: a. You are given the following information in the table below for security A, B and C. The market portfolio has a standard deviation of

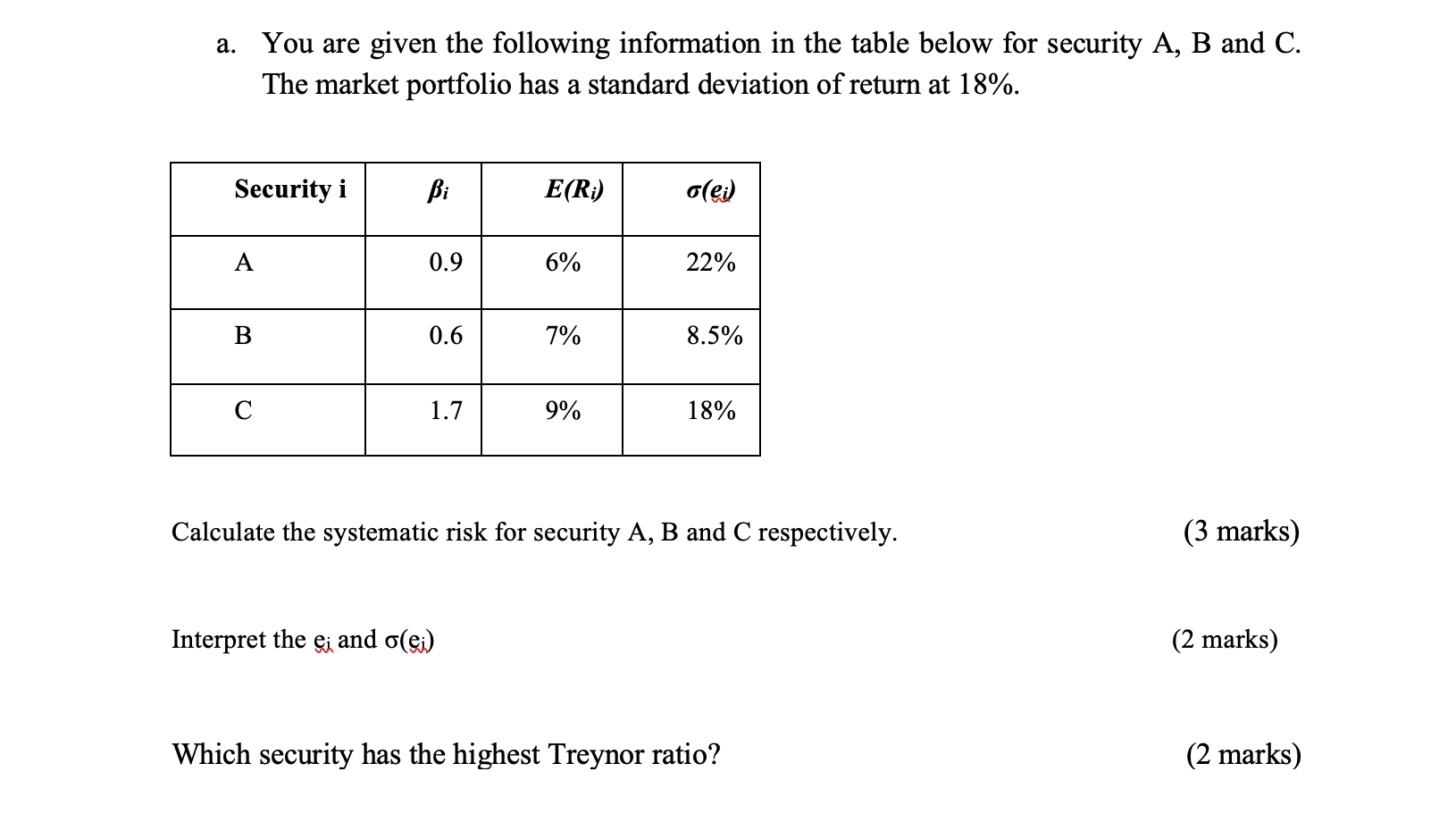

a. You are given the following information in the table below for security A, B and C. The market portfolio has a standard deviation of return at 18%.

Security i i E(Ri) (ei) A 0.9 6% 22% B 0.6 7% 8.5% C 1.7 9% 18%

Calculate the systematic risk for security A, B and C respectively. (3 marks)

Interpret the ei and (ei) (2 marks)

Which security has the highest Treynor ratio? (2 marks)

a. You are given the following information in the table below for security A, B and C. The market portfolio has a standard deviation of return at 18%. Security i Bi E(Ri) o(ei) A 0.9 6% 22% B 0.6 7% 8.5% C 1.7 9% 18% Calculate the systematic risk for security A, B and C respectively. (3 marks) Interpret the e; and o() Which security has the highest Treynor ratio? (2 marks) (2 marks)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts