Question: AaBbCc AaBbCeDd ABCcDd AaBbce Heading 4 Default Par. Hyperlink Normal Q & o (D Word Typesetting Find and Select Settings Replace Student 1 1 2

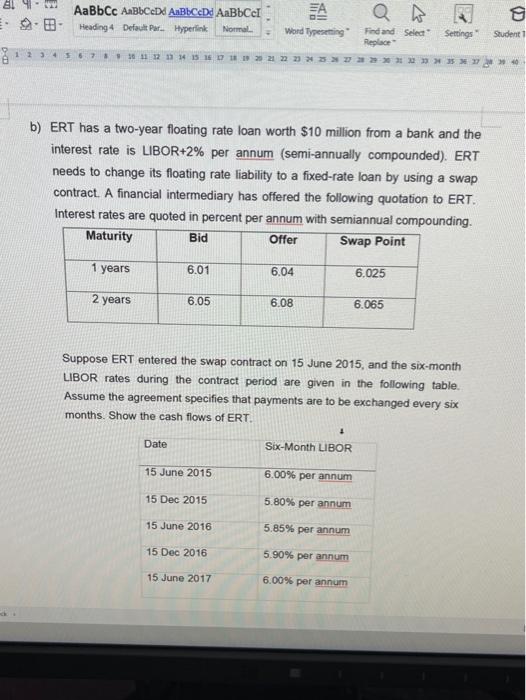

AaBbCc AaBbCeDd ABCcDd AaBbce Heading 4 Default Par. Hyperlink Normal Q & o (D Word Typesetting Find and Select Settings Replace Student 1 1 2 3 4 5 8 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 33 35 940 b) ERT has a two-year floating rate loan worth $10 million from a bank and the interest rate is LIBOR+2% per annum (semi-annually compounded). ERT needs to change its floating rate liability to a fixed-rate loan by using a swap contract. A financial intermediary has offered the following quotation to ERT. Interest rates are quoted in percent per annum with semiannual compounding. Maturity Bid Offer Swap Point 1 years 6.01 6.04 6.025 2 years 6.05 6.08 6.065 Suppose ERT entered the swap contract on 15 June 2015, and the six-month LIBOR rates during the contract period are given in the following table. Assume the agreement specifies that payments are to be exchanged every six months. Show the cash flows of ERT . Date Six-Month LIBOR 15 June 2015 6.00% per annum 15 Dec 2015 5.80% per annum 15 June 2016 5.85% per annum 15 Dec 2016 5.90% per annum 15 June 2017 6.00% per annum

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts