Question: about the accounting question 015 SECTION II 1. Process Costs: Spoilage; FIFO and Weighted Average. (CPA adapted]. The King Process Company manufacturers one product, processing

![FIFO and Weighted Average. (CPA adapted]. The King Process Company manufacturers one](https://s3.amazonaws.com/si.experts.images/answers/2024/06/66762425bc2e4_5336676242583c69.jpg)

about the accounting question

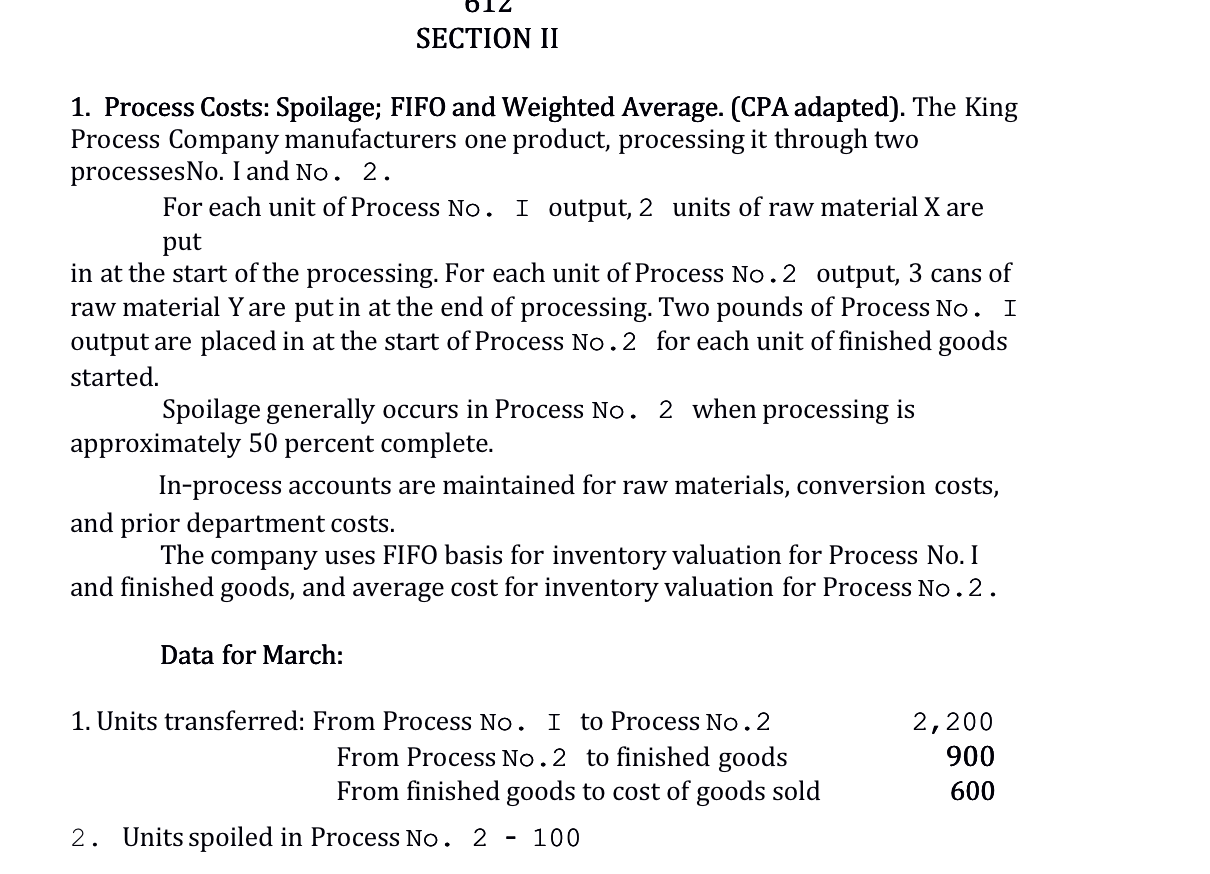

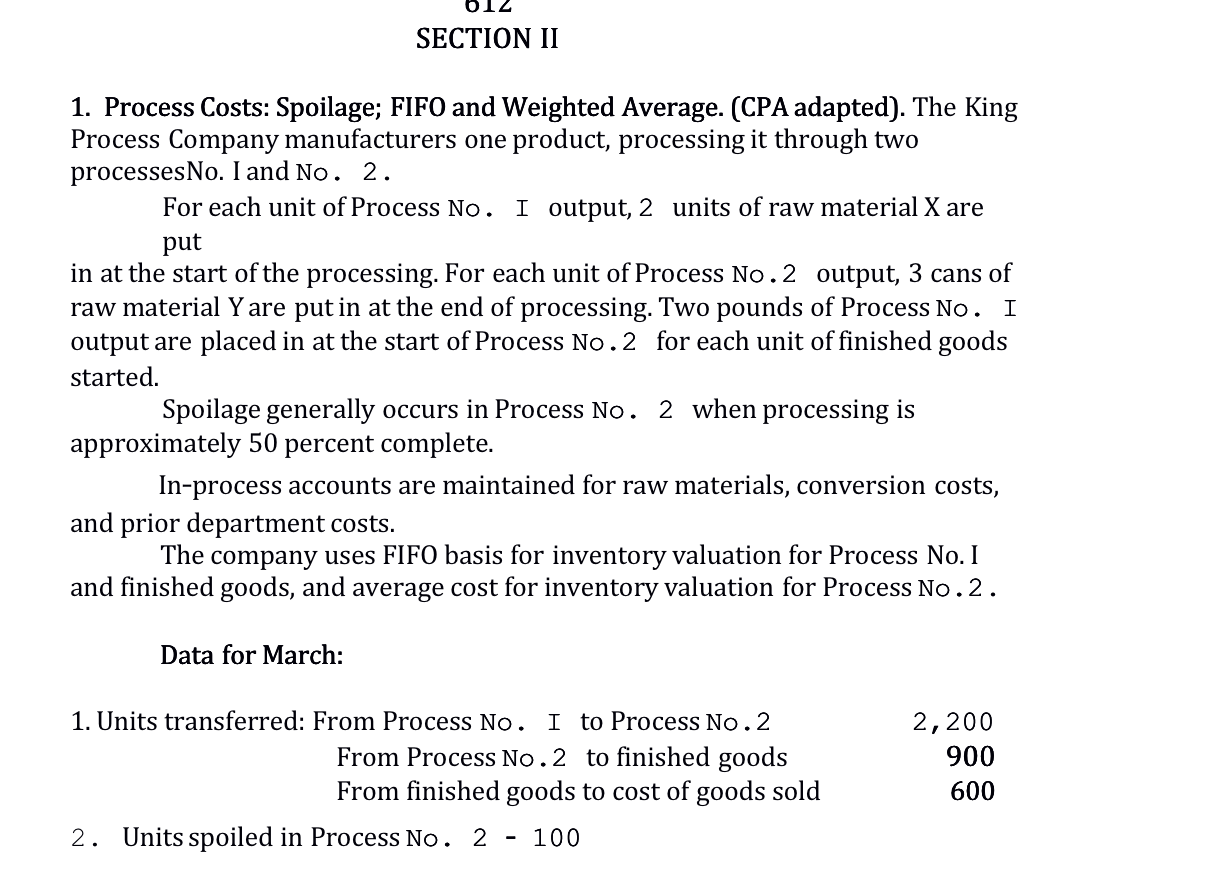

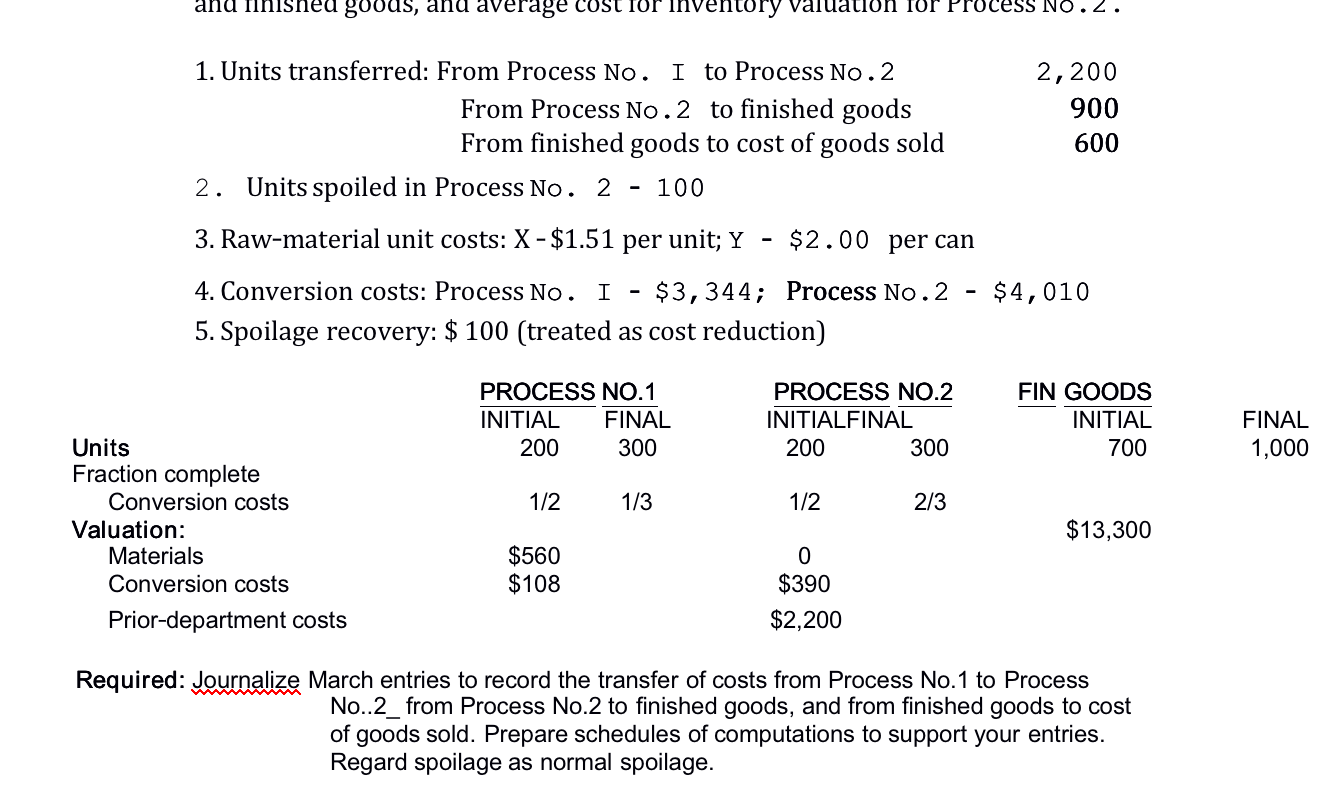

015 SECTION II 1. Process Costs: Spoilage; FIFO and Weighted Average. (CPA adapted]. The King Process Company manufacturers one product, processing it through two processesNo. I and No . 2 . For each unit of Process No . I output, 2 units of raw material X are put in at the start of the processing. For each unit of Process No . 2 output, 3 cans of raw material Y are put in at the end of processing. Two pounds of Process No . I output are placed in at the start of Process No . 2 for each unit of nished goods started. Spoilage generally occurs in Process No . 2 when processing is approximately 50 percent complete. In-process accounts are maintained for raw materials, conversion costs, and prior department costs. The company uses FIFO basis for inventory valuation for Process No.1 and nished goods, and average cost for inventory valuation for Process No . 2 . Data for March: 1. Units transferred: From Process No . I to Process No . 2 2 , 200 From Process No . 2 to nished goods 900 From nished goods to cost of goods sold 600 2 . Units spoiled in Process No. 2 - 100 and finished goods, and average cost for inventory valuation for Process No . Z . 1. Units transferred: From Process No. I to Process No . 2 2, 200 From Process No . 2 to finished goods 900 From finished goods to cost of goods sold 600 2. Units spoiled in Process No. 2 - 100 3. Raw-material unit costs: X - $1.51 per unit; Y - $2.00 per can 4. Conversion costs: Process No. I - $3, 344; Process No. 2 - $4, 010 5. Spoilage recovery: $ 100 (treated as cost reduction) PROCESS NO. 1 PROCESS NO.2 FIN GOODS INITIAL FINAL INITIALFINAL INITIAL FINAL Units 200 300 200 300 700 1,000 Fraction complete Conversion costs 1/2 1/3 1/2 2/3 Valuation: $13,300 Materials $560 0 Conversion costs $108 $390 Prior-department costs $2,200 Required: Journalize March entries to record the transfer of costs from Process No.1 to Process No..2_from Process No.2 to finished goods, and from finished goods to cost of goods sold. Prepare schedules of computations to support your entries. Regard spoilage as normal spoilage

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts