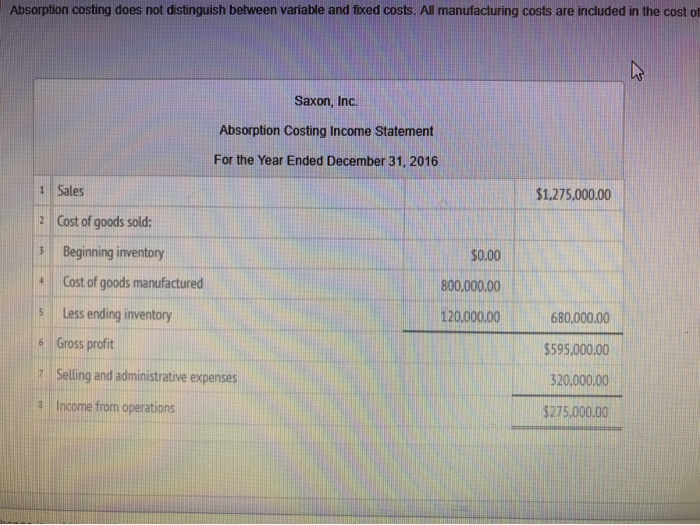

Question: Absorption costing does not distinguish between variable and fixed costs. All manufacturing costs are included in the cost of Saxon, Inc. Absorption Costing Income Statement

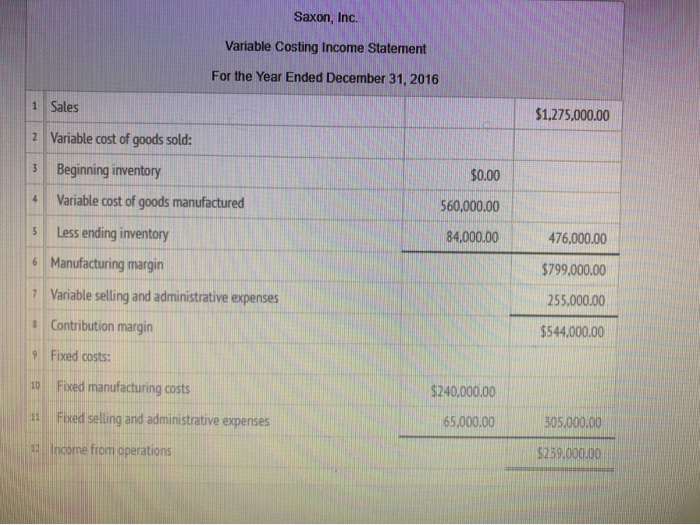

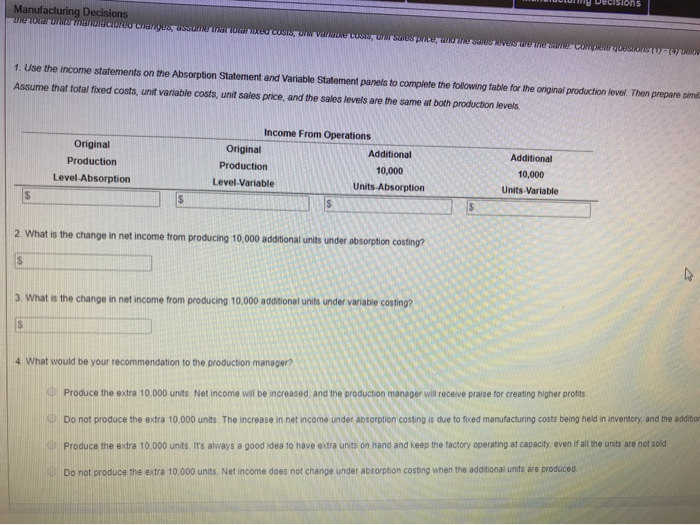

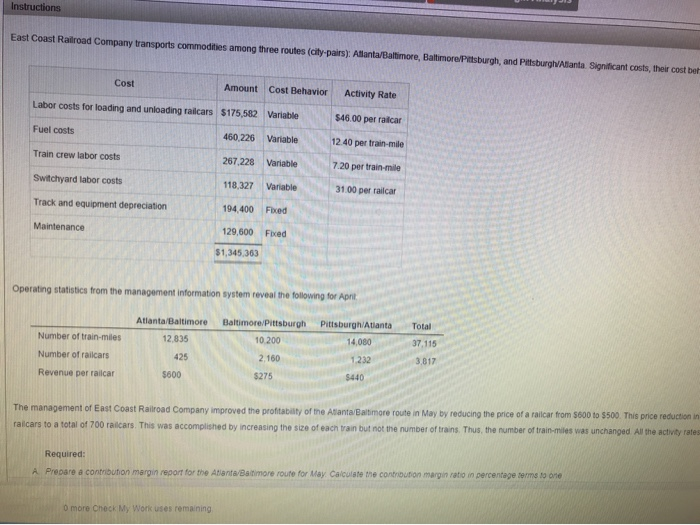

Absorption costing does not distinguish between variable and fixed costs. All manufacturing costs are included in the cost of Saxon, Inc. Absorption Costing Income Statement For the Year Ended December 31, 2016 1 Sales $1,275,000.00 2 Cost of goods sold: Beginning inventory $0.00 Cost of goods manufactured 4 800.000.00 Less ending inventory 120.000.00 680.000.00 Gross profit 6 $595.000.00 Selling and administrative expenses 320,000.00 3 Income from operations $275.000.00 Saxon, Inc. Variable Costing Income Statement For the Year Ended December 31, 2016 1 Sales $1.275,000.00 Variable cost of goods sold: 2 Beginning inventory $0.00 Variable cost of goods manufactured 560,000.00 Less ending inventory 84,000.00 476,000.00 6 Manufacturing margin $799,000.00 Variable selling and administrative expenses 7 255.000.00 Contribution margin $544,000.00 9 Fixed costs: Fixed manufacturing costs 10 $240.000.00 Ficed selling and administrative expenses 11 305.000.00 65.000.00 22 Income from operations $259,000.00 en ecisions Manufacturing Decisions Me1oururISTISTRrCINUUicKAUSUSuTH SLUGxedCOSS U VangoenUSIS UEBS ara rerstBSveste ve savcaCLe QOUSons AULOW 1. Use the income statements on the Absorption Statement and Variable Statement panels to complete the following table for the original production level. Then prepare simil Assume that total foxed costs, unit variable costs, unit sales price, and the sales levels are the same at both production levels Income From Operations Original Original Additional Additional Production Production 10,000 10,000 Level-Absorption Level-Variable Units-Absorption Units-Variable S S 2. What is the change in net income from producing 10,000 additional units under absorption costing? S 3. What is the change in net income from producing 10,000 addtional units under variable costing? 4 What would be your recommendation to the production manager? ALDProduce the extra 10,000 units. Net income wil be increased, and the production manager will receive praise for creating higher profits Do not produce the extra 10,000 units. The increase in net income under absorption costing is due to fixed manufacturing costs being held in inventory, and the addition Produce the extra 10.000 units. Its always a good idea to have extra units on hand and keep the factory operating at capacity, even if all the units are not sold Do not produce the extra 10.000 units, Net income does not change under absorption costing when the additional units are produced Instructions East Coast Railroad Company transports commodities among three routes (city-pairs). Alanta/Baltimore, Baltimore/Pittsburgh, and Pittsburgh/Alanta Significant costs, their cost bet Cost Amount Cost Behavior Activity Rate Labor costs for loading and unloading railcars $175,582 Variable $46.00 per railcar Fuel costs 460 226 Variable 12.40 per train-mile Train crew labor costs 267,228 Variable 7.20 per train-mile Switchyard labor costs 118.327 Variable 31.00 per railcar Track and equipment depreciation 194.400 Fixed Maintenance 129,600 Fxed $1,345.363 Operating statistics from the management information system reveal the following for Apri Baltimore/Pittsburgh Pittsburgh/Atlanta Total Atlanta/Baltimore 14,080 10.200 37.115 Number of train-miles 12,835 1,232 3,817 2.160 Number of railcars 425 $600 $440 $275 Revenue per railcar The management of East Coast Railroad Company improved the profitability of the Atanta/Baltimore route in May by reducing the price of a railcar from $600 to $500 This price reduction in railcars to a total of 700 railcars. This was accomplished by increasing the size of each train but not the number of trains. Thus, the number of train-miles was unchanged All the activity rates Required: Prepare a contribution margin report for the Atlianta/Balitimore route for May Calculate the contribution margin ratio in percentage tems to one A 0 more Check My Work uses remaining Absorption costing does not distinguish between variable and fixed costs. All manufacturing costs are included in the cost of Saxon, Inc. Absorption Costing Income Statement For the Year Ended December 31, 2016 1 Sales $1,275,000.00 2 Cost of goods sold: Beginning inventory $0.00 Cost of goods manufactured 4 800.000.00 Less ending inventory 120.000.00 680.000.00 Gross profit 6 $595.000.00 Selling and administrative expenses 320,000.00 3 Income from operations $275.000.00 Saxon, Inc. Variable Costing Income Statement For the Year Ended December 31, 2016 1 Sales $1.275,000.00 Variable cost of goods sold: 2 Beginning inventory $0.00 Variable cost of goods manufactured 560,000.00 Less ending inventory 84,000.00 476,000.00 6 Manufacturing margin $799,000.00 Variable selling and administrative expenses 7 255.000.00 Contribution margin $544,000.00 9 Fixed costs: Fixed manufacturing costs 10 $240.000.00 Ficed selling and administrative expenses 11 305.000.00 65.000.00 22 Income from operations $259,000.00 en ecisions Manufacturing Decisions Me1oururISTISTRrCINUUicKAUSUSuTH SLUGxedCOSS U VangoenUSIS UEBS ara rerstBSveste ve savcaCLe QOUSons AULOW 1. Use the income statements on the Absorption Statement and Variable Statement panels to complete the following table for the original production level. Then prepare simil Assume that total foxed costs, unit variable costs, unit sales price, and the sales levels are the same at both production levels Income From Operations Original Original Additional Additional Production Production 10,000 10,000 Level-Absorption Level-Variable Units-Absorption Units-Variable S S 2. What is the change in net income from producing 10,000 additional units under absorption costing? S 3. What is the change in net income from producing 10,000 addtional units under variable costing? 4 What would be your recommendation to the production manager? ALDProduce the extra 10,000 units. Net income wil be increased, and the production manager will receive praise for creating higher profits Do not produce the extra 10,000 units. The increase in net income under absorption costing is due to fixed manufacturing costs being held in inventory, and the addition Produce the extra 10.000 units. Its always a good idea to have extra units on hand and keep the factory operating at capacity, even if all the units are not sold Do not produce the extra 10.000 units, Net income does not change under absorption costing when the additional units are produced Instructions East Coast Railroad Company transports commodities among three routes (city-pairs). Alanta/Baltimore, Baltimore/Pittsburgh, and Pittsburgh/Alanta Significant costs, their cost bet Cost Amount Cost Behavior Activity Rate Labor costs for loading and unloading railcars $175,582 Variable $46.00 per railcar Fuel costs 460 226 Variable 12.40 per train-mile Train crew labor costs 267,228 Variable 7.20 per train-mile Switchyard labor costs 118.327 Variable 31.00 per railcar Track and equipment depreciation 194.400 Fixed Maintenance 129,600 Fxed $1,345.363 Operating statistics from the management information system reveal the following for Apri Baltimore/Pittsburgh Pittsburgh/Atlanta Total Atlanta/Baltimore 14,080 10.200 37.115 Number of train-miles 12,835 1,232 3,817 2.160 Number of railcars 425 $600 $440 $275 Revenue per railcar The management of East Coast Railroad Company improved the profitability of the Atanta/Baltimore route in May by reducing the price of a railcar from $600 to $500 This price reduction in railcars to a total of 700 railcars. This was accomplished by increasing the size of each train but not the number of trains. Thus, the number of train-miles was unchanged All the activity rates Required: Prepare a contribution margin report for the Atlianta/Balitimore route for May Calculate the contribution margin ratio in percentage tems to one A 0 more Check My Work uses remaining

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts