Question: ACC 640 Project Two Guidelines and Rubric Competency In this project, you will demonstrate your mastery of the following competency: Prepare standard audit reports in

ACC 640 Project Two Guidelines and Rubric

Competency

In this project, you will demonstrate your mastery of the following competency:

Prepare standard audit reports in compliance with Generally Accepted Auditing Standards

Overview

The executive summary audit report represents Part Three of the audit, following on from Part One and Part Two, which you completed as part of Project One.

Scenario

The auditing team of your CPA firm has performed an audit engagement for Keystone, which consists of testing financial statements, internal controls, and other factors that could have an impact on the company's position. At the end of the audit, the engagement partner has asked you to submit to all the firm's partners the final executive summary audit report. This will include an overall executive summary of the firm's internal control effectiveness in providing reasonable assurance on the company's financial statements and an explanation of the choice of an unqualified opinion versus a different opinion type.

Audit Findings

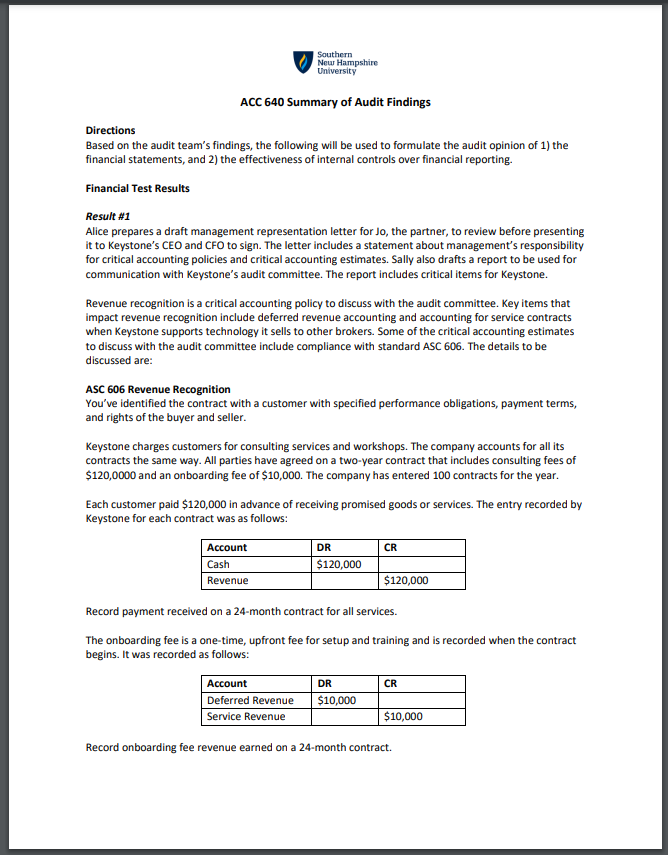

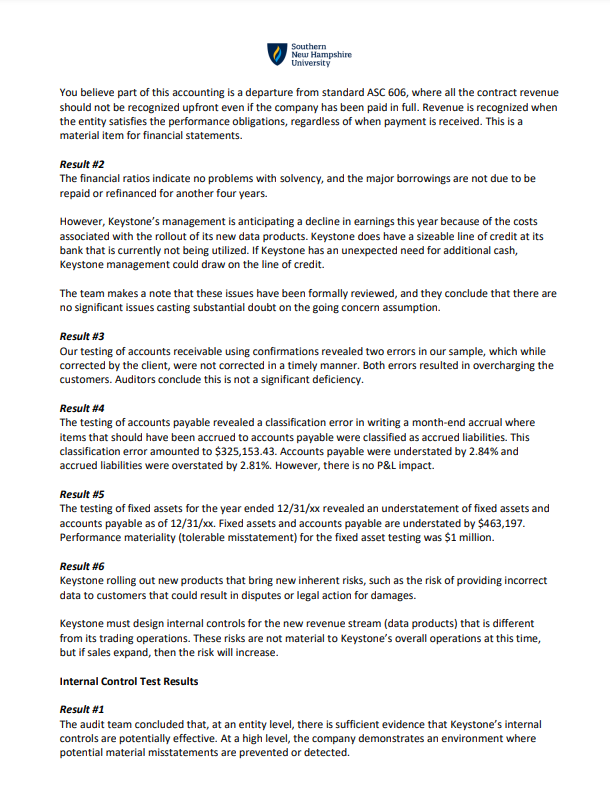

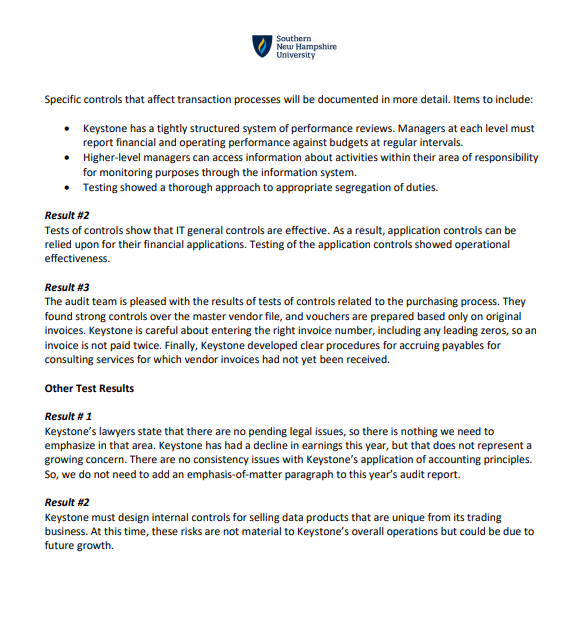

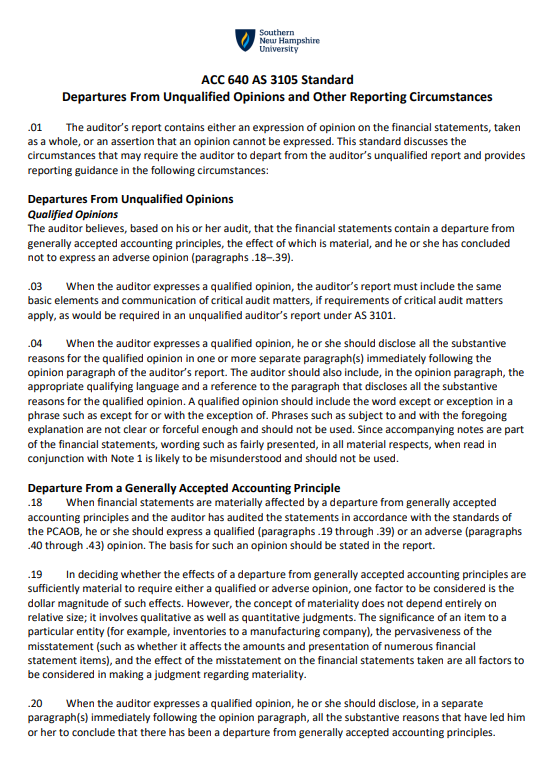

Southern Mour Hampshim Urniversity ACC 640 Summary of Audit Findings Directions Based on the audit team's findings, the following will be used to formulate the audit opinion of 1) the financial statements, and 2) the effectiveness of internal controls over financial reporting. Financial Test Results Result #1 Allce prepares a draft management representation letter for Jo, the partner, to review befare presenting it to Keystone's CEQ and CFO to sign. The letter includes a statement about management's responsibility for critical accounting policies and critical accounting estimates. Sally also drafts a report to be used for communication with Keystone's audit committee. The report includes critical items for Keystane. Revenue recognition 15 a critical accounting policy to discuss with the audit committes. Key items that impact revenue recognition include deferred revenue accounting and accounting for service contracts when Keystone supports technology it sells to other brokers. Some of the critical accounting estimates to discuss with the audit committee include compliance with standard ASC 606. The details to be discussed are: ASC 606 Revenue Recognition You've identified the contract with a customer with specified performance obligations, payment terms, and rights of the buyer and seller. Keystone charges customers for consulting services and warkshops. The company accounts for all its contracts the same way. All parties have agreed on a two-year contract that includes consulting fees of 5120,0000 and an onboarding fee of 510,000, The company has entered 100 contracts for the year. Each customer paid 5120,000 in advance of recelving promised goods or services. The entry recorded by Keystone for each contract was as follows: Aecows Jor | 100 Record payment received on a 24-month contract for all services. The enboarding fee is a one-time, upfront fee for setup and training and is recorded when the contract begins. It was recorded as follows: [ServceReverwe | [ 510,00 Record onboarding fee revenue eamed on a 24-month contract. Southern Meur Hampshire University You believe part of this accounting is a departure from standard ASC 806, where all the contract revenue should not be recognized upfront even If the company has been paid in full. Revenue is recognized when the entity satisfies the performance obligations, regardless of when payment is received. This is a material itern for financial statements. Result #2 The financial ratios indicate no problems with solvency, and the major borrowings are not due to be repaid or refinanced for another four years. However, Keystone's management is anticipating a decline in earnings this year because of the costs associated with the rollout of its new data products. Keystone does have a sizeable line of credit at its bank that is currently not being utilized. If Keystone has an unexpected need for additional cash, Keystone management could draw on the line of credit. The team makes a note that these issues have been formally reviewed, and they conclude that there are no significant issues casting substantial doubt on the going concern assumption. Result #3 Our testing of accounts receivable using confirmations revealed two errars in our sample, which while corrected by the client, were not corrected in a timely manner. Both errors resulted in overcharging the customers. Auditors conclude this is not a significant deficiency. Result #4 The testing of accounts payable revealed a classification error in writing a month-end accrual where items that should have been accrued to accounts payable were classified as accrued liabilities. This classification error amounted to 5325,153.43. Accounts payable were understated by 2.84% and accrued liabilities were overstated by 2.81%. However, there is no P&L impact. Result #5 The testing of fixed assets for the year ended 12/31/xx revealed an understatement of fixed assets amd accounts payable as of 12/31/ . Fixed assets and accounts payable are understated by $463,197. Performance materiality {tolerable misstatement) for the fixed asset testing was 51 million. Result #6 Keystone rolling out new products that bring new inherent risks, such as the risk of providing incorrect data to customers that could result in disputes or legal action for damages. Keystone must design internal contrals for the new revenue stream (data products) that is different from its trading operations. These risks are not material to Keystone's overall operations at this time, but if sales expand, then the risk will increase. Internal Control Test Results Result #1 The audit team concluded that, at an entity level, there is sufficient evidence that Keystone's internal controls are potentially effective. At a high level, the company demonstrates an environment where potential material misstatements are prevented or detected. Southern New Hampshire University Specific controls that affect transaction processes will be documented in more detail. Items to include: Keystone has a tightly structured system of performance reviews. Managers at each level must report financial and operating performance against budgets at regular intervals. Higher-level managers can access information about activities within their area of responsibility for monitoring purposes through the information system. Testing showed a thorough approach to appropriate segregation of duties. Result #2 Tests of controls show that IT general controls are effective. As a result, application controls can be relied upon for their financial applications. Testing of the application controls showed operational effectiveness. Result #3 The audit team is pleased with the results of tests of controls related to the purchasing process. They found strong controls over the master vendor file, and vouchers are prepared based only on original invoices. Keystone is careful about entering the right invoice number, including any leading zeros, so an invoice is not paid twice. Finally, Keystone developed clear procedures for accruing payables for consulting services for which vendor invoices had not yet been received. Other Test Results Result # 1 Keystone's lawyers state that there are no pending legal issues, so there is nothing we need to emphasize in that area. Keystone has had a decline in earnings this year, but that does not represent a growing concern. There are no consistency issues with Keystone's application of accounting principles. So, we do not need to add an emphasis-of-matter paragraph to this year's audit report. Result #2 Keystone must design internal controls for selling data products that are unique from its trading business. At this time, these risks are not material to Keystone's overall operations but could be due to future growth.Southern Nour Hampshire University ACC 640 AS 3105 Standard Departures From Unqualified Opinions and Other Reporting Circumstances .01 The auditor's report contains either an expression of opinion on the financial statements, taken as a whole, or an assertion that an opinion cannot be expressed. This standard discusses the circumstances that may require the auditor to depart from the auditor's unqualified report and provides reporting guidance in the following circumstances: Departures From Unqualified Opinions Qualified Opinions The auditor believes, based on his or her audit, that the financial statements contain a departure from generally accepted accounting principles, the effect of which is material, and he or she has concluded not to express an adverse opinion (paragraphs .18-.39). 03 When the auditor expresses a qualified opinion, the auditor's report must include the same basic elements and communication of critical audit matters, if requirements of critical audit matters apply, as would be required in an unqualified auditor's report under AS 3101. .04 When the auditor expresses a qualified opinion, he or she should disclose all the substantive reasons for the qualified opinion in one or more separate paragraph(s) immediately following the opinion paragraph of the auditor's report. The auditor should also include, in the opinion paragraph, the appropriate qualifying language and a reference to the paragraph that discloses all the substantive reasons for the qualified opinion. A qualified opinion should include the word except or exception in a phrase such as except for or with the exception of. Phrases such as subject to and with the foregoing explanation are not clear or forceful enough and should not be used. Since accompanying notes are part of the financial statements, wording such as fairly presented, in all material respects, when read in conjunction with Note 1 is likely to be misunderstood and should not be used. Departure From a Generally Accepted Accounting Principle 18 When financial statements are materially affected by a departure from generally accepted accounting principles and the auditor has audited the statements in accordance with the standards of the PCAOB, he or she should express a qualified (paragraphs .19 through .39) or an adverse (paragraphs 40 through .43) opinion. The basis for such an opinion should be stated in the report. .19 In deciding whether the effects of a departure from generally accepted accounting principles are sufficiently material to require either a qualified or adverse opinion, one factor to be considered is the dollar magnitude of such effects. However, the concept of materiality does not depend entirely on relative size; it involves qualitative as well as quantitative judgments. The significance of an item to a particular entity (for example, inventories to a manufacturing company), the pervasiveness of the misstatement (such as whether it affects the amounts and presentation of numerous financial statement items), and the effect of the misstatement on the financial statements taken are all factors to be considered in making a judgment regarding materiality. .20 When the auditor expresses a qualified opinion, he or she should disclose, in a separate paragraph(s) immediately following the opinion paragraph, all the substantive reasons that have led him or her to conclude that there has been a departure from generally accepted accounting principles.Southern Mour Hampshire University Furthermore, the opinion paragraph should include the appropriate gualifying language and a reference to the paragraph(s) that describe the substantive reasons for the gualified opinion. 21 The paragraph(s) immediately following the opinion paragraph that describes the substantive reasans that led the auditor to conclude that there has been a departure from generally accepted accounting principles should also disclose the principal effects of the subject matter of the qualification on the financial position, results of operations, and cash flows, if practicable. If the effects are not reasonably determinable, the report should so state. If such disclosures are made in a note to the financial statements, the paragraph(s) that describe the substantive reasons for the qualified opinion may be shortened by referring to it. Financial Statement Audit Report for a Qualified Opinion Example 22 An example of a repart in which the apinion is gualified because of the use of an accounting principle at variance with generally accepted accounting principles follows (assuming the effects are such that the auditor has concluded that an adverse opinion is not appropriate): Report of Independent Registered Public Accounting Firm To the shareholders and the board of directors of X Company Opinion on the Financial Statements We have audited the accompanying balance sheets of X Company (the "Company\") as of December 31, 2062 and 2001, the related statements of [titles of the financial statements, e.g., income, comprehensive income, stockholders' equity, and cash flows] for each of the years then ended, and the related notes [and schedules] (collectively referred to as the \"Financial statements\"). In our opinion, except for the effects of not capitalizing certain lease obligations as discussed in the following paragraph, the financial statements referred to above prasent fairly, in all material respects, the financial position of the Company as of December 31, 20X2 and 20X1, and the results of its operations and its cash flows for the years then ended in confermity with accounting principles generally accepted in the United States of America. The Company has excluded from property and debt in the accompanying balance sheets, certain lease obligations that, in our opinion, should be capitalized to conform with accounting principles generally accepted in the United States of America. If these lease obligations were capitalized, the property would be increased by 5 and 5 long-term debt by 5 and & and retained earnings by S and & as of December 31, 20%2, and 20X1, respectively. Additionally, net income would be increased (decreased) by 5 and % and earnings per share would be increased (decreased) by S and 5 respectively, for the years then ended. Basis for Opinion [Same basic elements as the Basis for Opinion section of the auditor's ungualified report in AS 3101] Critical Audit Matters [if applicable] [Include critical audit matters) [Signature] We have served as the Company's auditor since [year]. [City and State or Country] [Date]

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Accounting Questions!