Question: According to ValueLine estimates in Figure 1, James River’s expected annual dividend growth rate from the 91–93 to 97–99 period is 5.50%, and the next

According to ValueLine estimates in Figure 1, James River’s expected annual dividend growth rate from the 91–93 to 97–99 period is 5.50%, and the next dividend (1995) is expected to be $0.60. Assume that the required return for James River was 8.36% on January 1 1995 and that the 5.50% growth rate was expected to continue indefinitely.

a. Based on the Constant Growth Rate or Gordon Model, what was James River’s price at the beginning of 1995?

b. What conditions must hold to use the constant growth model? Do many “real world” stocks satisfy the constant growth assumptions?

2) The Wall Street Journal (WSJ) lists the current price of James River common stock at $27.00.

a. Based on this information, the ValueLine 1995 expected dividend, and the annual rate of dividend change for the growth estimate, what is the company’s return on common stock using the constant growth model? What is the expected dividend yield and expected capital gains yield? Explain the difference in the required return estimates from the ValueLine (see question 1a) to the WSJ price data.

b. What is the relationship between dividend yield and capital gains yield over time under constant growth assumptions?

Figure 1

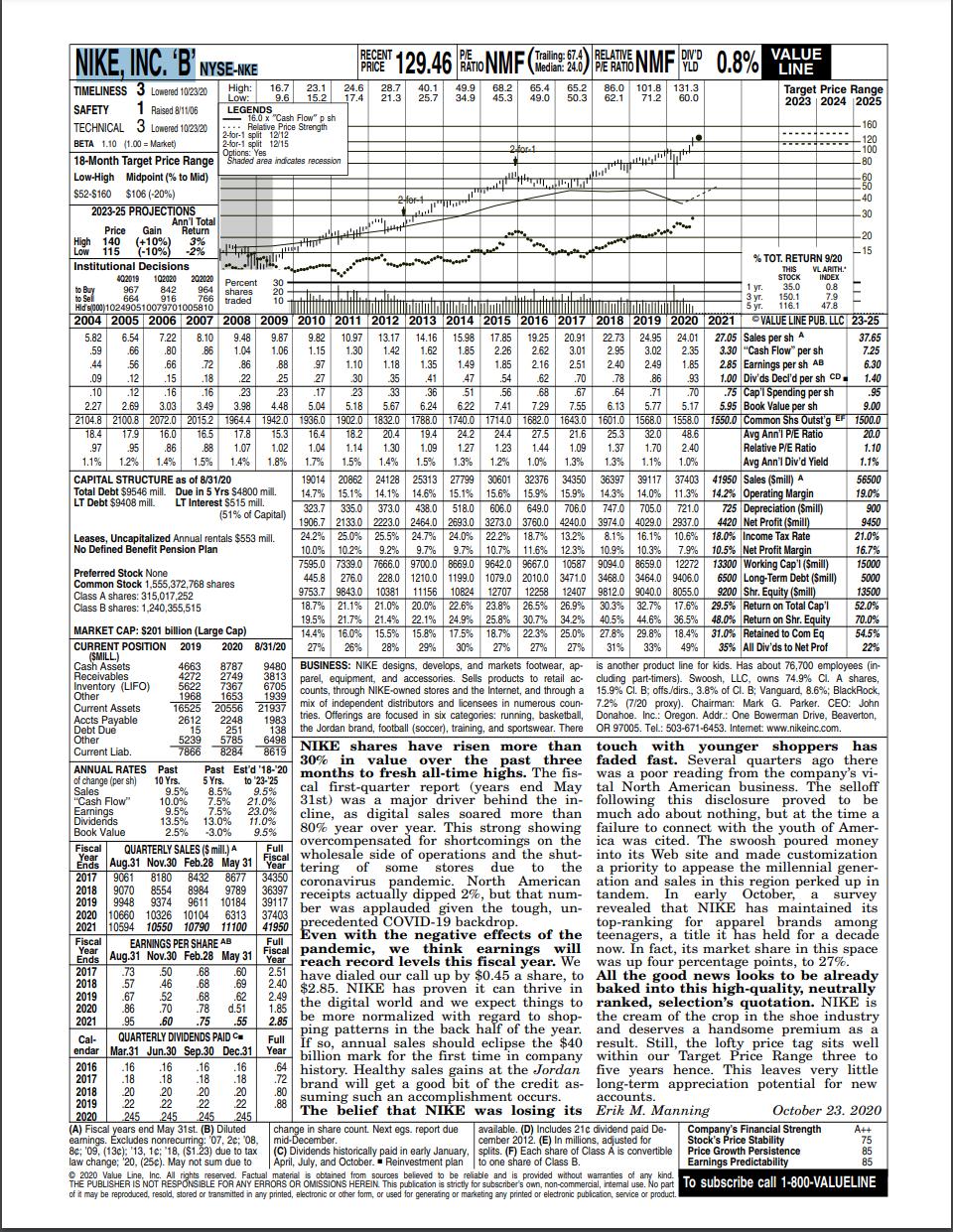

NIKE, INC. 'B' NYSE-NKE High: Low: LEGENDS TIMELINESS 3 Lowered 10/23/20 SAFETY 1 Raised 8/11/06 TECHNICAL 3 Lowered 10/23/20 BETA 1.10 (1.00 = Market) 18-Month Target Price Range Low-High Midpoint (% to Mid) $52-$160 $106 (-20%) 2023-25 PROJECTIONS Price Gain High 140 (+10%) Low 115 (-10%) -2% 402019 967 664 Ann'l Total Return 3% Preferred Stock None Common Stock 1,555,372,768 shares Class A shares: 315,017,252 Class B shares: 1,240,355,515 16.7 23.1 9.6 15.2 Leases, Uncapitalized Annual rentals $553 mill. Defined Benefit Pension Plan Accts Payable Debt Due Other 16.0 x "Cash Flow" p sh Relative Price Strength 12/12 2-for-1 split 2-for-1 split 12/15 Options: Yes Shaded area indicates recession Current Liab. ANNUAL RATES of change (per sh) Sales "Cash Flow" Earnings Dividends Book Value MARKET CAP: $201 billion (Large Cap) CURRENT POSITION 2019 2020 8/31/20 (SMILL.) Cash Assets Receivables Inventory (LIFO) Other Current Assets - 4663 8787 9480 4272 2749 3813 5622 7367 6705 1968 1653 1939 16525 20556 21937 2612 2248 1983 15 251 138 5239 5785 6498 7866 8284 8619 | Institutional Decisions Ti to Buy 102020 202020 842 964 to Sell 916 766 Hid's 000)102490510079701005810 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 Percent 30 shares 20 traded 10 minining Indir 13.17 14.16 15.98 17.85 19.25 20.91 5.82 6.54 7.22 8.10 9.48 9.87 9.82 10.97 1.15 1.30 1.10 59 .66 .80 86 1.04 1.06 1.42 1.62 1.18 1.35 1.85 2.26 2.62 1.49 1.85 2.16 22.73 24.95 24.01 2.95 3.02 2.35 2.49 1.85 .86 93 44 56 .66 .72 .86 88 3.01 2.51 .70 97 2.40 .09 .12 .15 .18 .22 25 30 35 .41 47 54 .78 10 .12 16 16 23 23 23 33 .36 51 56 .67 .71 70 .64 7.55 6.13 5.77 5.17 2.27 2.69 3.03 3.49 3.98 4.48 5.04 5.18 5.67 6.24 6.22 7.41 7.29 2104.8 2100.8 2072.0 2015.2 18.4 17.9 16.0 16.5 .97 95 .86 .88 1.1% 1.2% 1.4% 1.5% CAPITAL STRUCTURE as of 8/31/20 Total Debt $9546 mill. Due in 5 Yrs $4800 mill. LT Debt $9408 mill. LT Interest $515 mill. (51% of Capital) 900 9450 21.0% 1964.4 1942.0 1936.0 1902.0 1832.0 1788.0 1740.0 1714.0 1682.0 1643.0 1601.0 1568.0 1558.0 17.8 15.3 16.4 18.2 20.4 19.4 24.2 24.4 27.5 21.6 25.3 32.0 48.6 1.07 1.02 1.04 1.14 1.30 1.09 1.27 1.23 1.44 1.09 1.37 1.70 2.40 1.4% 1.8% 1.7% 1.5% 1.4% 1.5% 1.3% 1.2% 1.0% 1.3% 1.3% 1.1% 1.0% 19014 20862 24128 25313 27799 30601 32376 34350 36397 39117 37403 14.7% 15.1% 14.1% 14.6% 15.1% 15.6 % 15.9% 15.9% 14.3% 14.0% 11.3% 323.7 335.0 373.0 438.0 518.0 606.0 649.0 706.0 747.0 705.0 721.0 1906.7 2133.0 2223.0 2464.0 2693.0 3273.0 3760.0 4240.0 3974.0 4029.0 2937.0 24.2% 25.0% 25.5% 24.7% 24.0% 22.2% 18.7% 13.2% 8.1% 16.1% 10.6% 10.0% 10.2% 9.2% 9.7% 9.7% 10.7% 10.7% 11.6 % 12.3% 10.9% 10.3% 7.9% 7595.0 7339.0 7666.0 9700.0 8669.0 9642.0 9667.0 10587 9094.0 8659.0 12272 445.8 276.0 228.0 1210.0 1199.0 1079.0 2010.0 3471.0 3468.0 3464.0 9406.0 10381 9753.7 9843.0 11156 10824 12707 12258 12407 9812.0 9040.0 8055.0 18.7% 21.1% 21.0% 20.0% 22.6% 23.8% 26.5% 26.9% 30.3% 32.7% 17.6% 19.5% 21.7% 21.4% 22.1% 24.9% 25.8% 30.7% 34.2% 40.5% 44.6% 36.5% 14.4% 16.0% 15.5% 15.8 % 17.5% 18.7% 22.3% 25.0 % 27.8% 29.8% 18.4% 27% 26% 28% 29% 30% 27% 27% 27% 31% 33% 49% is another product line for kids. Has about 76,700 employees (in- cluding part-timers). Swoosh, LLC, owns 74.9 % Cl. A shares, 15.9% Cl. B; offs./dirs., 3.8% of Cl. B; Vanguard, 8.6%; BlackRock, 7.2% (7/20 proxy). Chairman: Mark G. Parker. CEO: John Donahoe. Inc.: Oregon. Addr.: One Bowerman Drive, Beaverton, OR 97005. Tel.: 503-671-6453. Internet: www.nikeinc.com. touch with younger shoppers has faded fast. Several quarters ago there was a poor reading from the company's vi- tal North American business. The selloff following this disclosure proved to be much ado about nothing, but at the time a failure to connect with the youth of Amer- ica was cited. The swoosh poured money into its Web site and made customization 725 Depreciation (Smill) 4420 Net Profit (Smill) 18.0% Income Tax Rate 10.5% Net Profit Margin 13300 Working Cap'l (Smill) 6500 Long-Term Debt (Smill) 9200 Shr. Equity (Smill) 29.5% Return on Total Cap'l 48.0% Return on Shr. Equity 31.0% Retained to Com Eq 35% All Div'ds to Net Prof 16.7% 15000 5000 13500 52.0% 70.0% 54.5% 22% BUSINESS: NIKE designs, develops, and markets footwear, ap- parel, equipment, and accessories. Sells products to retail ac- counts, through NIKE-owned stores and the Internet, and through a oun mix of independent distributors and licensees in numerous coun- tries. Offerings are focused in six categories: running, basketball, the Jordan brand, football (soccer), training, and sportswear. There a priority to appease the millennial gener- ation and sales in this region perked up in tandem. In early October, a survey revealed that NIKE has maintained its top-ranking for apparel brands among teenagers, a title it has held for a decade now. In fact, its market share in this space was up four percentage points, to 27%. All the good news looks to be already baked into this high-quality, neutrally ranked, selection's quotation. NIKE is the cream of the crop in the shoe industry and deserves a handsome premium as a result. Still, the lofty price tag sits well within our Target Price Range three to five years hence. This leaves very little long-term appreciation potential for new accounts. 27 17 RECENT P/E PRICE 129.46 RATIO NMF (Teding: 576) PLATONMF DVD 0.8% VALUE Trailing: 67.4 24.0 RELATIVE P/E YLD LINE 24.6 28.7 40.1 49.9 68.2 65.4 65.2 86.0 101.8 131.3 17.4 21.3 25.7 34.9 45.3 49.0 50.3 62.1 71.2 60.0 Se 2-for-1 62 68 .f NIKE shares have risen more than 30% in value over the past three Past Est'd '18-20 months to fresh all-time highs. The fis- to '23-25 cal first-quarter report (years end May 31st) was a major driver behind the in- cline, as digital sales soared more than 80% year over year. This strong showing overcompensated for shortcomings on the Fiscal wholesale side of operations and the shut Year of some stores due to 34350 coronavirus pandemic. North American 36397 receipts actually dipped 2%, but that num- 39117 ber was applauded given the tough, un- 41950 precedented COVID-19 backdrop. Past 10 Yrs. 5 Yrs. 9.5% 8.5% 9.5% 10.0% 7.5% 21.0% 9.5% 7.5% 23.0% 13.5% 13.0% 11.0% 2.5% -3.0% 9.5% Fiscal QUARTERLY SALES ($ mill.) A Full Ends Aug.31 Nov.30 Feb.28 May 31 2017 9061 8180 8432 8677 2018 9070 8554 8984 9789 2019 9948 9374 9611 10184 2020 10660 10326 10104 6313 37403 2021 10594 10550 10790 11100 Fiscal PER AB Full Year Aug.31 Nov.30 Feb.28 May 31 Fiscal Year 2.51 2.40 2.49 1.85 2017 .73 .50 .68 .60 2018 57 46 68 .69 2019 .67 52 .68 .62 2020 .86 .70 78 d.51 2021 95 .60 .75 .55 Cal- QUARTERLY DIVIDENDS PAID C Full endar Mar.31 Jun.30 Sep.30 Dec.31 Year 2016 16 .16 .16 16 2017 .18 .18 .18 .18 2018 20 20 20 .20 2019 22 .22 22 .22 2020 245 245 245 245 (A) Fiscal years end May 31st. (B) Diluted earnings. Excludes nonrecurring: '07, 2c; '08. 8c; '09, (13c); '13, 1c; '18, ($1.23) due to tax law change; '20, (25c). May not sum due to Value Line, material obtained from kind. THE PUBLISHER IS NOT RESPONSIBLE FOR ANY ERRORS OR OMISSIONS HEREIN. This publication is strictly for subscriber's own, non-commercial, internal use. No part of it may be reproduced, resold, stored or transmitted in any printed, electronic or other form, or used for generating or marketing any printed or electronic publication, service or product. Even with the negative effects of the pandemic, we think earnings will reach record levels this fiscal year. We have dialed our call up by $0.45 a share, to $2.85. NIKE has proven it can thrive in the digital world and we expect things to 2.85 be more normalized with regard to shop- ping patterns in the back half of the year If so, annual sales should eclipse the $40 billion mark for the first time in company 64 history. Healthy sales gains at the Jordan brand will get a good bit of the credit as- suming such an accomplishment occurs. The belief that NIKE was losing its .72 .80 .88 change in share count. Next egs. report due mid-December. (C) Dividends historically paid in early January, April, July, and October. Reinvestment plan to reliable and is without warranties of Target Price Range 2023 2024 2025 . % TOT. RETURN 9/20 THIS VL ARITH.' 0.8 STOCK INDEX 35.0 150.1 116.1 1 yr. 3 yr. 5 yr. 7.9 47.8 27.05 Sales per sh A 3.30 "Cash Flow" per sh 2.85 Earnings per sh AB 1.00 Div'ds Decl'd per sh CD 75 Cap'l Spending per sh 5.95 Book Value per sh 1550.0 Common Shs Outst'g Avg Ann'l P/E Ratio Relative P/E Ratio EF 160 120 -100 -80 -60 .50 .40 -30 VALUE LINE PUB. LLC 23-25 Avg Ann'l Div'd Yield 41950 Sales (Smill) A 14.2% Operating Margin -20 -15 T 37.65 7.25 6.30 1.40 .95 9.00 1500.0 20.0 1.10 1.1% 56500 19.0% Erik M. Manning October 23. 2020 available. (D) Includes 21c dividend paid De- Company's Financial Strength A++ cember 2012. (E) In millions, adjusted for Stock's Price Stability splits. (F) Each share of Class A is convertible Price Growth Persistence to one share of Class B. 75 85 Earnings Predictability 85 To subscribe call 1-800-VALUELINE

Step by Step Solution

3.46 Rating (159 Votes )

There are 3 Steps involved in it

a Based on the Constant Growth Rate or Gordon Model the price of James Rivers stock at the beginning of 1995 is calculated as Price D1 r g Where D1 is the expected dividend for 1995 060 r is the requi... View full answer

Get step-by-step solutions from verified subject matter experts