1. The misstatements below are included in the accounting records of the Dilon Manufacturing Company Read...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

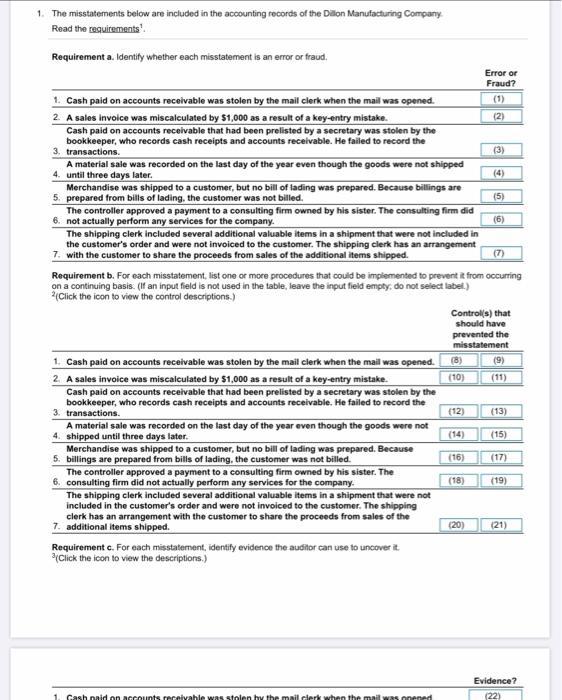

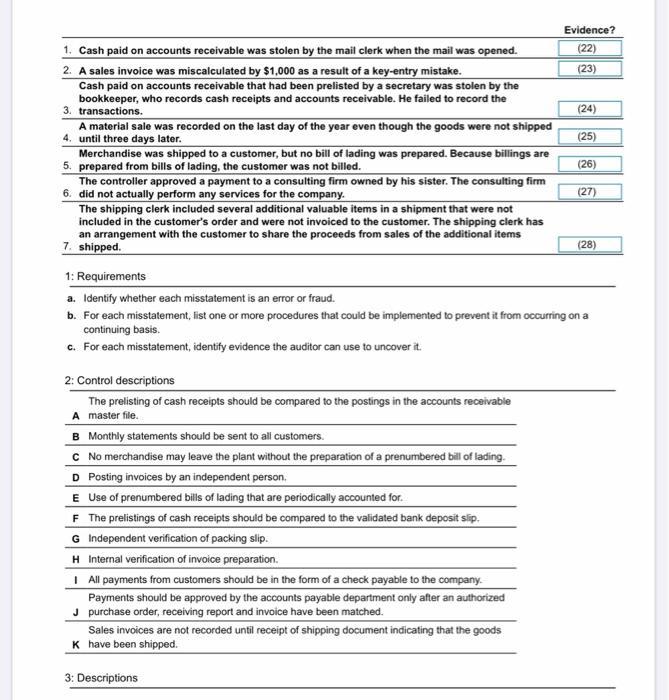

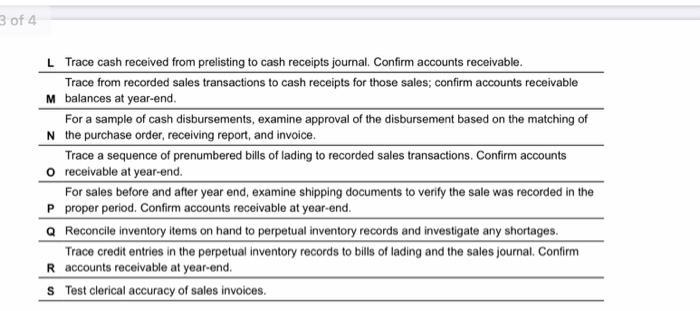

1. The misstatements below are included in the accounting records of the Dilon Manufacturing Company Read the requirements'. Requirement a. Identify whether each misstatement is an error or fraud. Error or Fraud? 1. Cash paid on accounts receivable was stolen by the mail clerk when the mail was opened. 2. A sales invoice was miscalculated by $1,000 as a result of a key-entry mistake. (1) (2) Cash paid on acounts receivable that had been prelisted by a secretary was stolen by the bookkeeper, who records cash receipts and accounts receivable. He failed to record the 3. transactions. A material sale was recorded on the last day of the year even though the goods were not shipped 4. until three days later. (3) (4) Merchandise was shipped to a customer, but no bill of lading was prepared. Because billings are 5. prepared from bills of lading. the customer was not billed. The controller approved a payment to a consulting firm owned by his sister. The consulting firm did 6. not actually perform any services for the company. The shipping clerk included several additional valuable items in a shipment that were not included in the customer's order and were not invoiced to the customer. The shipping clerk has an arrangement 7. with the customer to share the proceeds from sales of the additional items shipped. (5) (6) (7) Requirement b. For each misstatement, list one or more procedures that could be implemented to prevent it from occurring on a continuing basis. (If an input field is not used in the table, leave the input field empty: do not select label.) (Click the icon to view the control descriptions.) Control(s) that should have prevented the misstatement 1. Cash paid on accounts receivable was stolen by the mail clerk when the mail was opened. (8) (9) (10) 2. A sales invoice was miscalculated by $1,000 as a result of a key-entry mistake. Cash paid on accounts receivable that had been prelisted by a secretary was stolen by the bookkeeper, who records cash receipts and accounts receivable. He failed to record the 3. transactions. A material sale was recorded on the last day of the year even though the goods were not 4. shipped until three days later. Merchandise was shipped to a customer, but no bill of lading was prepared. Because 5. billings are prepared from bills of lading, the customer was not billed. The controller approved a payment to a consulting firm owned by his sister. The 6. consulting firm did not actually perform any services for the company. The shipping clerk included several additional valuable items in a shipment that were not included in the customer's order and were not invoiced to the customer. The shipping clerk has an arrangement with the customer to share the proceeds from sales of the 7. additional items shipped. (11) (12) (13) (14) (15) (16) (17) (18) (19) (20) (21) Requirement c. For each misstatement, identify evidence the auditor can use to uncover it. (Click the icon to view the descriptions.) Evidence? 1. Cash naid on accounts receivahle was stolen hy the mail clerk when the mail was onened (22) Evidence? 1. Cash paid on accounts receivable was stolen by the mail clerk when the mail was opened. (22) (23) 2. A sales invoice was miscalculated by $1,000 as a result of a key-entry mistake. Cash paid on accounts receivable that had been prelisted by a secretary was stolen by the bookkeeper, who records cash receipts and accounts receivable. He failed to record the 3. transactions. A material sale was recorded on the last day of the year even though the goods were not shipped 4. until three days later. (24) (25) Merchandise was shipped to a customer, but no bill of lading was prepared. Because billings are 5. prepared from bills of lading, the customer was not billed. The controller approved a payment to a consulting firm owned by his sister. The consulting firm 6. did not actually perform any services for the company. (26) (27) The shipping clerk included several additional valuable items in a shipment that were not included in the customer's order and were not invoiced to the customer. The shipping clerk has an arrangement with the customer to share the proceeds from sales of the additional items 7. shipped. (28) 1: Requirements a. Identify whether each misstatement is an error or fraud. b. For each misstatement, list one or more procedures that could be implemented to prevent it from occurring on a continuing basis. c. For each misstatement, identify evidence the auditor can use to uncover it. 2: Control descriptions The prelisting of cash receipts should be compared to the postings in the accounts receivable A master file. B Monthly statements should be sent to all customers. C No merchandise may leave the plant without the preparation of a prenumbered bill of lading. D Posting invoices by an independent person. E Use of prenumbered bills of lading that are periodically accounted for. F The prelistings of cash receipts should be compared to the validated bank deposit slip. G Independent verification of packing slip. H Internal verification of invoice preparation. I All payments from customers should be in the form of a check payable to the company. Payments should be approved by the accounts payable department only after an authorized J purchase order, receiving report and invoice have been matched. Sales invoices are not recorded until receipt of shipping document indicating that the goods K have been shipped. 3: Descriptions 3 of 4 L Trace cash received from prelisting to cash receipts journal. Confirm accounts receivable. Trace from recorded sales transactions to cash receipts for those sales; confirm accounts receivable M balances at year-end. For a sample of cash disbursements, examine approval of the disbursement based on the matching of N the purchase order, receiving report, and invoice. Trace a sequence of prenumbered bills of lading to recorded sales transactions. Confirm accounts O receivable at year-end. For sales before and after year end, examine shipping documents to verify the sale was recorded in the P proper period. Confirm accounts receivable at year-end. Q Reconcile inventory items on hand to perpetual inventory records and investigate any shortages. Trace credit entries in the perpetual inventory records to bills of lading and the sales journal. Confirm R accounts receivable at year-end. S Test clerical accuracy of sales invoices. 1. The misstatements below are included in the accounting records of the Dilon Manufacturing Company Read the requirements'. Requirement a. Identify whether each misstatement is an error or fraud. Error or Fraud? 1. Cash paid on accounts receivable was stolen by the mail clerk when the mail was opened. 2. A sales invoice was miscalculated by $1,000 as a result of a key-entry mistake. (1) (2) Cash paid on acounts receivable that had been prelisted by a secretary was stolen by the bookkeeper, who records cash receipts and accounts receivable. He failed to record the 3. transactions. A material sale was recorded on the last day of the year even though the goods were not shipped 4. until three days later. (3) (4) Merchandise was shipped to a customer, but no bill of lading was prepared. Because billings are 5. prepared from bills of lading. the customer was not billed. The controller approved a payment to a consulting firm owned by his sister. The consulting firm did 6. not actually perform any services for the company. The shipping clerk included several additional valuable items in a shipment that were not included in the customer's order and were not invoiced to the customer. The shipping clerk has an arrangement 7. with the customer to share the proceeds from sales of the additional items shipped. (5) (6) (7) Requirement b. For each misstatement, list one or more procedures that could be implemented to prevent it from occurring on a continuing basis. (If an input field is not used in the table, leave the input field empty: do not select label.) (Click the icon to view the control descriptions.) Control(s) that should have prevented the misstatement 1. Cash paid on accounts receivable was stolen by the mail clerk when the mail was opened. (8) (9) (10) 2. A sales invoice was miscalculated by $1,000 as a result of a key-entry mistake. Cash paid on accounts receivable that had been prelisted by a secretary was stolen by the bookkeeper, who records cash receipts and accounts receivable. He failed to record the 3. transactions. A material sale was recorded on the last day of the year even though the goods were not 4. shipped until three days later. Merchandise was shipped to a customer, but no bill of lading was prepared. Because 5. billings are prepared from bills of lading, the customer was not billed. The controller approved a payment to a consulting firm owned by his sister. The 6. consulting firm did not actually perform any services for the company. The shipping clerk included several additional valuable items in a shipment that were not included in the customer's order and were not invoiced to the customer. The shipping clerk has an arrangement with the customer to share the proceeds from sales of the 7. additional items shipped. (11) (12) (13) (14) (15) (16) (17) (18) (19) (20) (21) Requirement c. For each misstatement, identify evidence the auditor can use to uncover it. (Click the icon to view the descriptions.) Evidence? 1. Cash naid on accounts receivahle was stolen hy the mail clerk when the mail was onened (22) Evidence? 1. Cash paid on accounts receivable was stolen by the mail clerk when the mail was opened. (22) (23) 2. A sales invoice was miscalculated by $1,000 as a result of a key-entry mistake. Cash paid on accounts receivable that had been prelisted by a secretary was stolen by the bookkeeper, who records cash receipts and accounts receivable. He failed to record the 3. transactions. A material sale was recorded on the last day of the year even though the goods were not shipped 4. until three days later. (24) (25) Merchandise was shipped to a customer, but no bill of lading was prepared. Because billings are 5. prepared from bills of lading, the customer was not billed. The controller approved a payment to a consulting firm owned by his sister. The consulting firm 6. did not actually perform any services for the company. (26) (27) The shipping clerk included several additional valuable items in a shipment that were not included in the customer's order and were not invoiced to the customer. The shipping clerk has an arrangement with the customer to share the proceeds from sales of the additional items 7. shipped. (28) 1: Requirements a. Identify whether each misstatement is an error or fraud. b. For each misstatement, list one or more procedures that could be implemented to prevent it from occurring on a continuing basis. c. For each misstatement, identify evidence the auditor can use to uncover it. 2: Control descriptions The prelisting of cash receipts should be compared to the postings in the accounts receivable A master file. B Monthly statements should be sent to all customers. C No merchandise may leave the plant without the preparation of a prenumbered bill of lading. D Posting invoices by an independent person. E Use of prenumbered bills of lading that are periodically accounted for. F The prelistings of cash receipts should be compared to the validated bank deposit slip. G Independent verification of packing slip. H Internal verification of invoice preparation. I All payments from customers should be in the form of a check payable to the company. Payments should be approved by the accounts payable department only after an authorized J purchase order, receiving report and invoice have been matched. Sales invoices are not recorded until receipt of shipping document indicating that the goods K have been shipped. 3: Descriptions 3 of 4 L Trace cash received from prelisting to cash receipts journal. Confirm accounts receivable. Trace from recorded sales transactions to cash receipts for those sales; confirm accounts receivable M balances at year-end. For a sample of cash disbursements, examine approval of the disbursement based on the matching of N the purchase order, receiving report, and invoice. Trace a sequence of prenumbered bills of lading to recorded sales transactions. Confirm accounts O receivable at year-end. For sales before and after year end, examine shipping documents to verify the sale was recorded in the P proper period. Confirm accounts receivable at year-end. Q Reconcile inventory items on hand to perpetual inventory records and investigate any shortages. Trace credit entries in the perpetual inventory records to bills of lading and the sales journal. Confirm R accounts receivable at year-end. S Test clerical accuracy of sales invoices.

Expert Answer:

Answer rating: 100% (QA)

a 1 Fraud 2 Error 3 Fraud 4 Fraud 5 Error 6 Fraud 7 Fraud b The following procedures may be deployed to avoid such fraud or errors 1 Daily bank deposi... View the full answer

Related Book For

Auditing and Assurance services an integrated approach

ISBN: 978-0132575959

14th Edition

Authors: Alvin a. arens, Randal j. elder, Mark s. Beasley

Posted Date:

Students also viewed these general management questions

-

The following misstatements are included in the accounting records of the Joyce Manufacturing Company: 1. A shipment to a customer was not billed because of the loss of the bill of lading. 2. A sales...

-

The following misstatements are included in the accounting records of Lathen Manufacturing Company: 1. Joe Block and Frank Demery take turns punching in for each other every few days. The absent...

-

The following misstatements are included in the accounting records of Lathen Manufacturing Company: 1. Joe Block and Frank Demery take turns "punching in" for each other every few days. The absent...

-

If a particular glucose fermentation process is 87.0% efficient, how many grams of glucose would be required for the production of 51.0 g of ethyl alcohol (C 2 H 5 OH)? C 6 H 12 O 6 2C 2 H 5 OH +...

-

How should the target population be defined?

-

The ball of Figure 10.32 is launched from the origin of an \(x y\) coordinate system. Write expressions giving, at the top of its trajectory, the ball's rectangular coordinates in terms of the...

-

With reference to the preceding exercise, for which temperature is the probability 0.05 that it will be exceeded during one day? Data From Preceding Exercise Determining a joint cumulative...

-

Two Wheeler, a bike shop, opened for business on April 1. It uses a periodic inventory system. The following transactions occurred during the first month of business: April 1: Purchased five units...

-

A sales budget is given below for one of the products manufactured by the Key Co: January-20 000 units, February-35 000 units, March-60 000 units, April - 40 000 units. The inventory of finished...

-

The number 6 has four divisorsnamely, 1, 2, 3, and 6. List all numbers less than 20 that have exactly four divisors.

-

what is the difference between explicit and implicit memory? evaluate experimental tests of implicit memory.

-

When can an employer be liable for the intentional torts of an employee?

-

True Or False Absolute privileges are enjoyed by judges, lawyers, parties, and witnesses during judicial proceedings unless their motive is defamation.

-

False-light claims require proof that a. the plaintiff is put before the public in a false light that would be highly offensive to a reasonable person. b. the defendant deliberately portrayed the...

-

True Or False Under the common law majority rule, a bailor is not vicariously liable for the acts of a bailee unless the bailor is negligent in entrusting their goods into the care of a bailee they...

-

Give an example of a situation in which negligence would be imputed. a. Give an example of a situation in which negligence would not be imputed. b. What is the general rule today regarding the...

-

What is the latest brand value for Fair and Lovely? 2. Illustrate FIVE (5) brand elements associated with Fair and Lovely.

-

Simplify the expression. Assume that all variables are positive. 23VI1 2 V44 8

-

You are doing the audit of Peckinpah Tire and Parts, a wholesale auto parts company. You have decided to use monetary unit sampling (MUS) for the audit of accounts receivable and inventory. The...

-

State what is meant by a representative sample and explain its importance in sampling audit populations.

-

The first standard of field work requires the performance of the audit by a person or persons having adequate technical training and proficiency as an auditor. What are the various ways in which...

-

In a study of casino size (square feet) and revenue, the value of r = 0.445 is obtained. Find the value of r2. What does that value tell us?

-

In a study of global warming, assume that we have found a strong positive correlation between carbon dioxide concentration and temperature. Identify three possible explanations for this correlation.

-

For 10 pairs of sample data, the correlation coefficient is computed to be r = -1. What do you know about the scatterplot?

Study smarter with the SolutionInn App