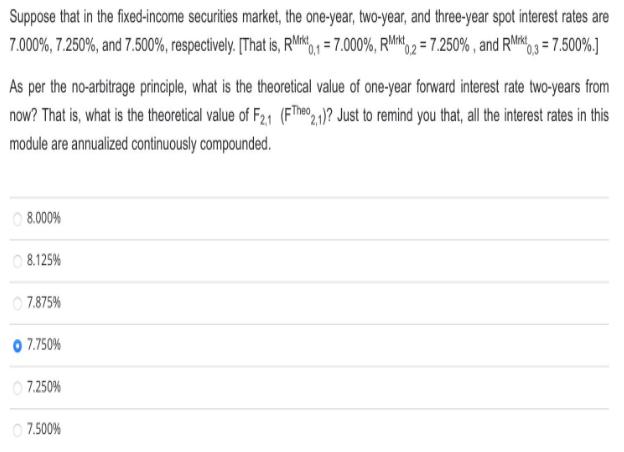

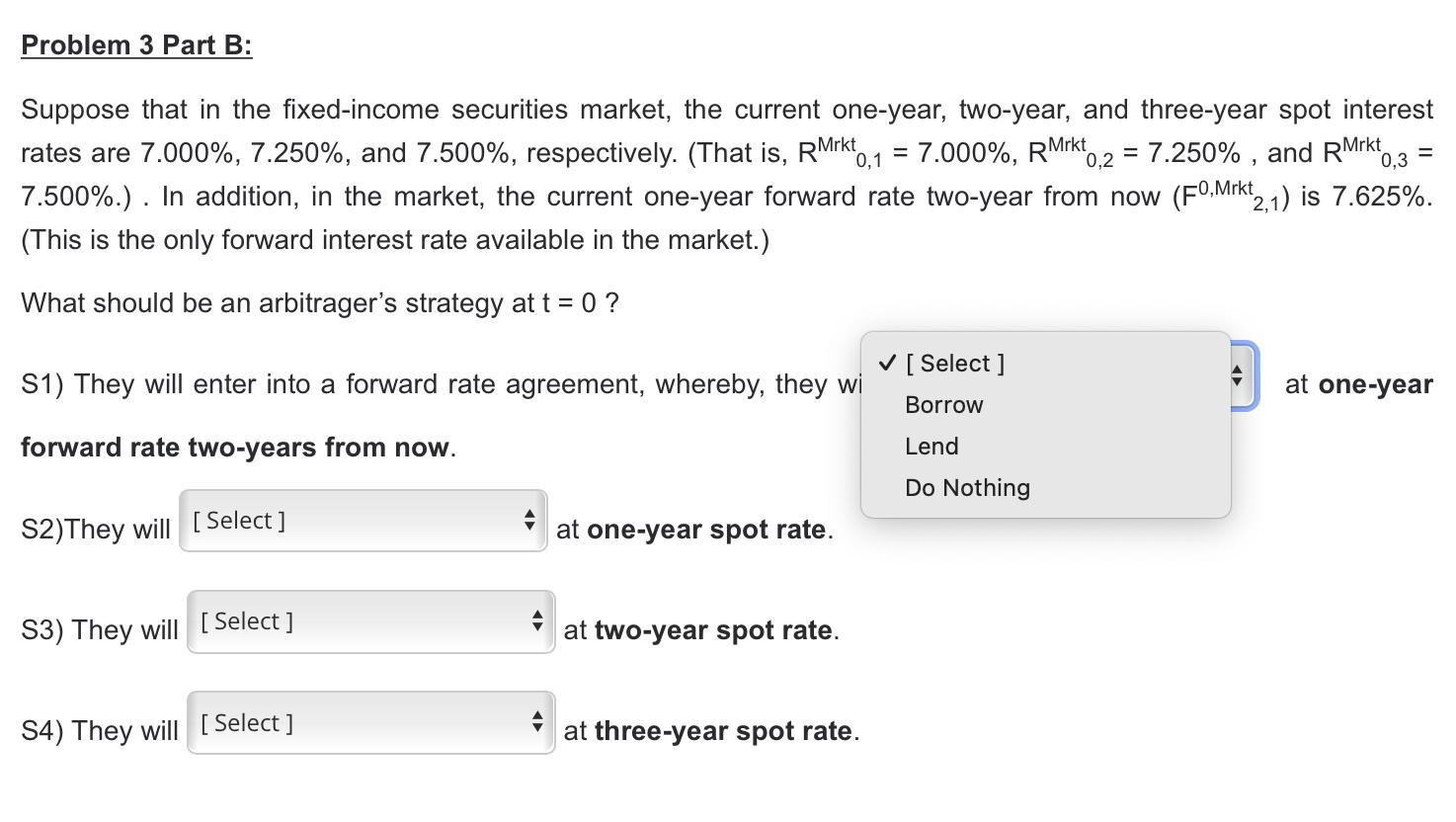

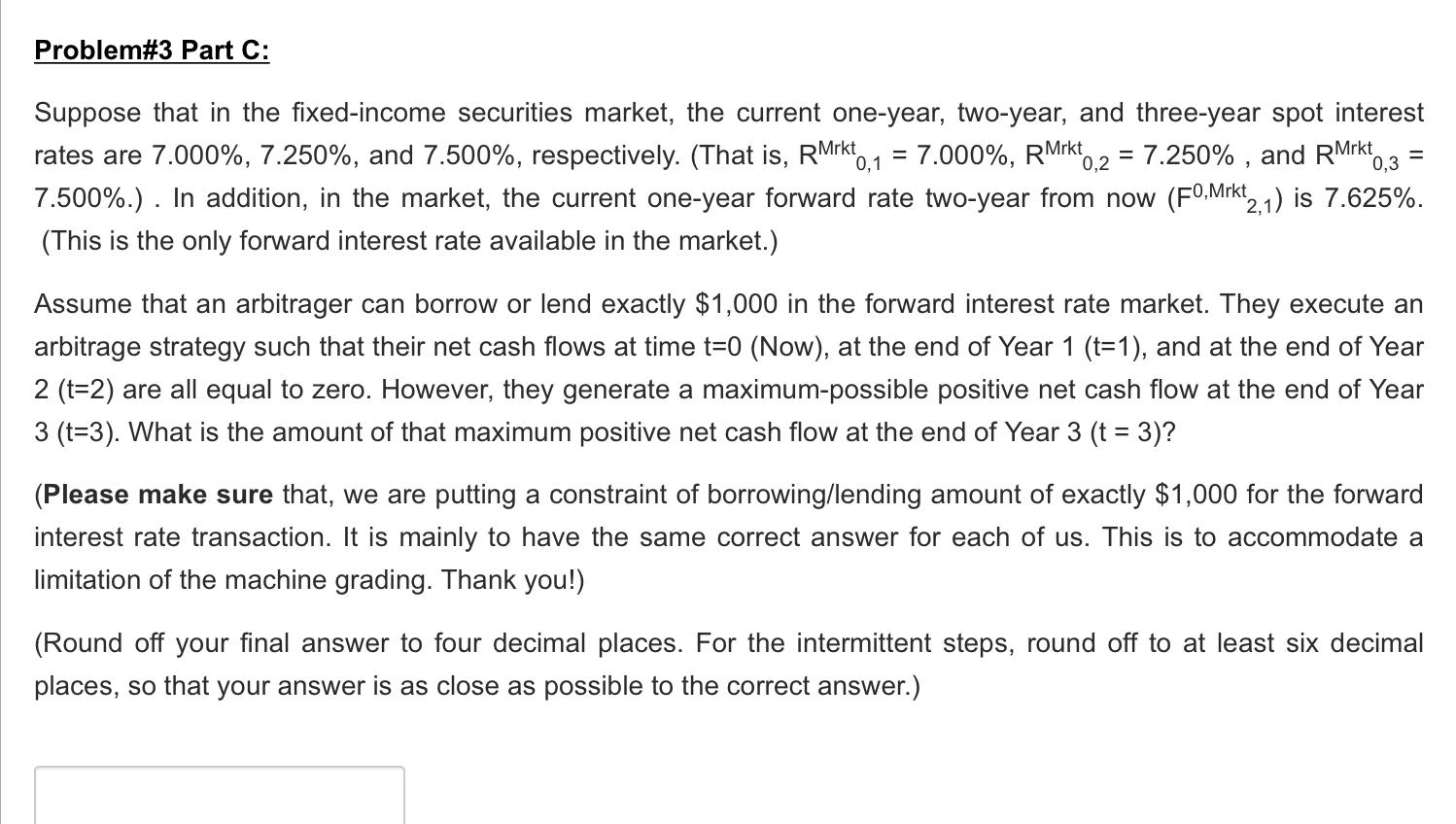

Suppose that in the fixed-income securities market, the one-year, two-year, and three-year spot interest rates are...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Related Book For

Concepts in Federal Taxation

ISBN: 9780324379556

19th Edition

Authors: Kevin E. Murphy, Mark Higgins, Tonya K. Flesher

Posted Date: