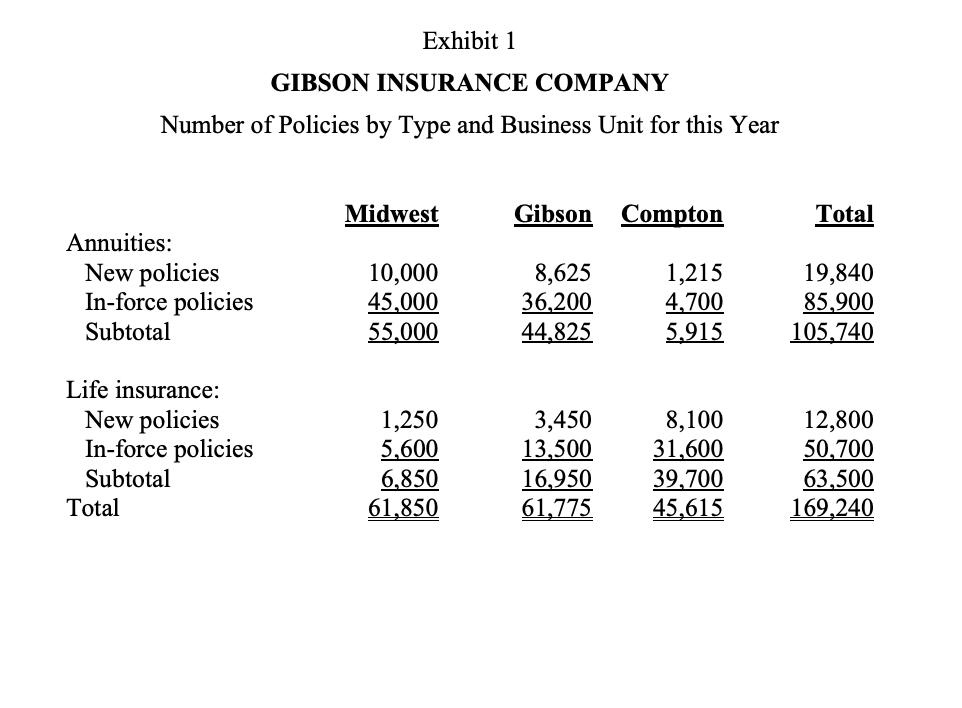

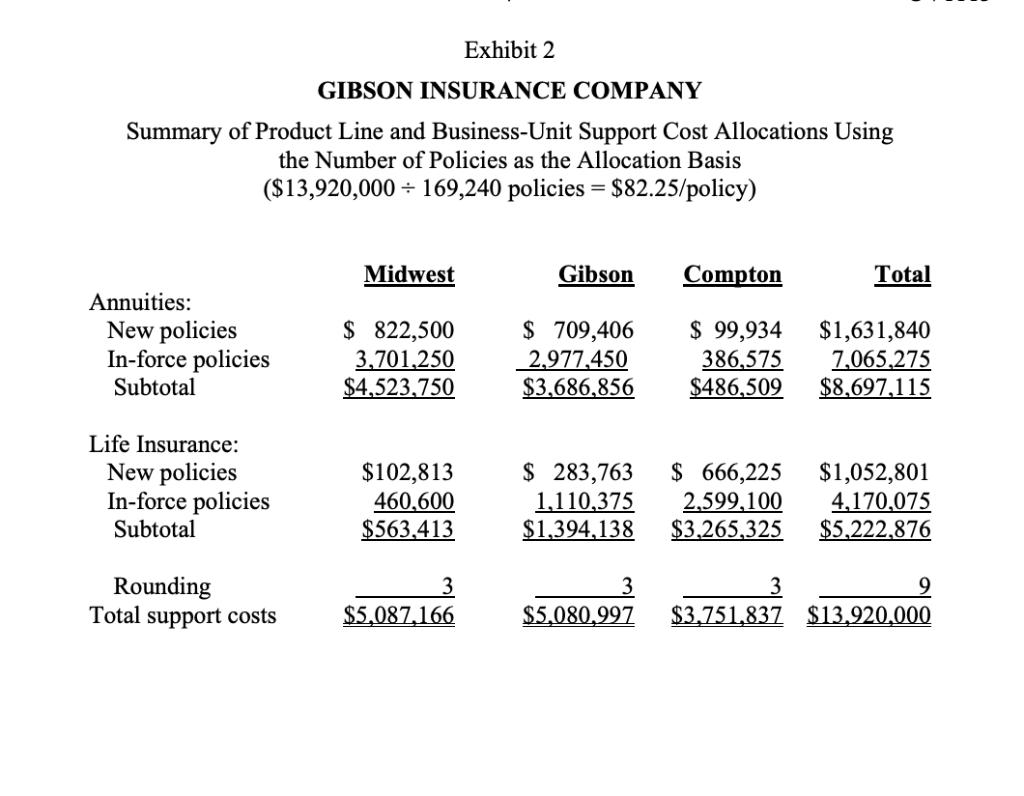

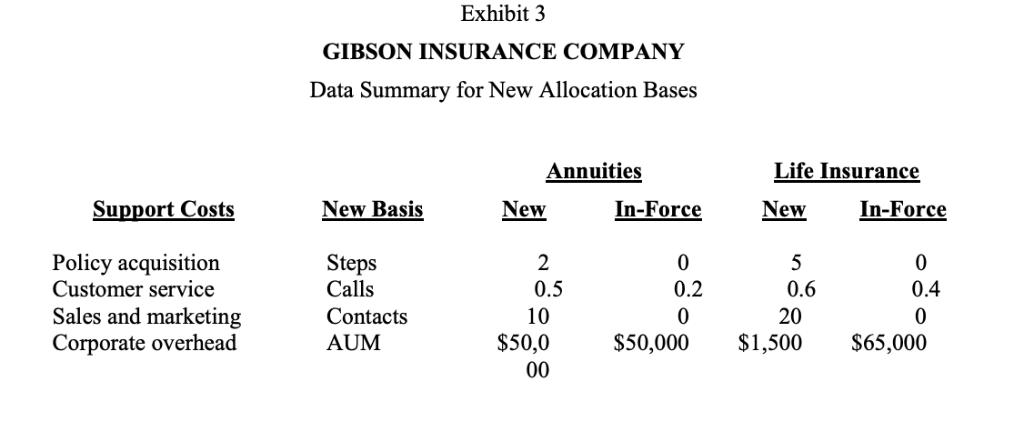

Exhibit 1 GIBSON INSURANCE COMPANY Number of Policies by Type and Business Unit for this Year...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

Exhibit 1 GIBSON INSURANCE COMPANY Number of Policies by Type and Business Unit for this Year Midwest Gibson Compton Total Annuities: New policies In-force policies 10,000 45,000 55.000 8,625 36.200 44.825 1,215 4,700 5.915 19,840 85,900 105,740 Subtotal Life insurance: New policies In-force policies 1,250 5,600 6,850 61.850 3,450 13,500 16.950 61,775 8,100 31,600 39,700 45,615 12,800 50,700 63,500 169,240 Subtotal Total Exhibit 2 GIBSON INSURANCE COMPANY Summary of Product Line and Business-Unit Support Cost Allocations Using the Number of Policies as the Allocation Basis ($13,920,000 + 169,240 policies = $82.25/policy) %3D Midwest Gibson Compton Total Annuities: New policies In-force policies Subtotal $ 822,500 3,701,250 $4,523,750 $ 709,406 2,977,450 $3,686,856 $ 99,934 386,575 $486,509 $1,631,840 7.065,275 $8,697,115 Life Insurance: New policies In-force policies Subtotal $102,813 460,600 $563.413 $ 283,763 1,110,375 $1,394,138 $ 666,225 2.599,100 $3.265,325 $1,052,801 4,170,075 $5,222.876 Rounding Total support costs 3 $5,087,166 $5,080,997 $3,751,837 $13,920,000 Exhibit 3 GIBSON INSURANCE COMPANY Data Summary for New Allocation Bases Annuities Life Insurance Support Costs New Basis New In-Force New In-Force Policy acquisition Steps Calls 5 Customer service Sales and marketing Corporate overhead 0.5 0.2 0.6 0.4 Contacts 10 20 AUM $50,0 $50,000 $1,500 $65,000 00 outcome. After some thought and effort, she was able to collapse nearly 50 different corporate cost accounts into these 4 categories. Aggregated Corporate Support Costs for this Year $ 4,375,000 2,426,000 4,552,000 2,567,000 $ 13,920,000 Policy acquisition Customer service Sales and marketing Other corporate support Total Hampton knew that some of those aggregated costs were incurred to support new policies that had been issued during this year, while others supported in-force policies issued in previous years. As she dug further into the effort to issue and service policies, it was clear to her that there were distinct tasks repeated in, and different among, the various products. Those tasks, for example, included items such as underwriting reviews, health screenings/evaluations, billings, collections, records creation/maintenance, and responding to customer queries. It seemed like the sale of a policy spawned a flurry of corporate activity. She wondered if Gibson's processes were as streamlined and efficient as they could be, but she filed that thought away for a later date-the new cost allocation approach was her current imperative. It seemed to Hampton that there were a host of potential allocation bases that could be adopted in lieu of the currently used basis of the number of policies. She decided that there was merit in keeping the new approach simple (as best reflected in an underlying root cause for the cost), and acceptable to the departmental managers and product line managers who would be evaluated, in part, on their financial performance that involved the resulting allocations. Finally, Hampton decided to make her first attempt at using the new allocation bases as noted below. For each of the four new allocation bases, she presented herself with a test, which was to summarize her rationale for the allocation base in a brief, coherent, logical fashion. If she could not do that, then she must interpret that as a signal that she needed to investigate the proposed basis in more detail to settle on an intuitively defensible basis for that one. 1) Policy acquisition costs: New allocation basis: Number of steps involved in moving new policy applications to an in-force status. Rationale for new basis: The administrative staff at Gibson's headquarters processed new policy applications for all three legal entities and for both life insurance and annuity products. From an administrative staff resources perspective, annuities required two major steps to issue a policy: a review of the application data and the electronic imaging of the application. Life insurance policies required the same two steps as annuities, but they also required additional steps for the following administrative tasks pertaining to the underwriting work involved: generate files for reinsurance, review medical information Questions 1) Calculate the unit support cost per policy for new and in-force annuity and life insurance policies using the new allocation bases. In addition, calculate the total support costs to be reported by product for each legal business unit entity. 2) Why would Hampton want to track that information by product even if that level of detail was not required by regulators? 3) Will the new support cost allocation information help Gibson Insurance establish better pricing guidelines for the various annuities and life insurance products sold by each legal business unit entity? Why or why not? 4) Is there room for improvement in the means by which the corporate support costs are allocated under Hampton's new approach? If yes, in what way(s)? If no, why not? Exhibit 1 GIBSON INSURANCE COMPANY Number of Policies by Type and Business Unit for this Year Midwest Gibson Compton Total Annuities: New policies In-force policies 10,000 45,000 55.000 8,625 36.200 44.825 1,215 4,700 5.915 19,840 85,900 105,740 Subtotal Life insurance: New policies In-force policies 1,250 5,600 6,850 61.850 3,450 13,500 16.950 61,775 8,100 31,600 39,700 45,615 12,800 50,700 63,500 169,240 Subtotal Total Exhibit 2 GIBSON INSURANCE COMPANY Summary of Product Line and Business-Unit Support Cost Allocations Using the Number of Policies as the Allocation Basis ($13,920,000 + 169,240 policies = $82.25/policy) %3D Midwest Gibson Compton Total Annuities: New policies In-force policies Subtotal $ 822,500 3,701,250 $4,523,750 $ 709,406 2,977,450 $3,686,856 $ 99,934 386,575 $486,509 $1,631,840 7.065,275 $8,697,115 Life Insurance: New policies In-force policies Subtotal $102,813 460,600 $563.413 $ 283,763 1,110,375 $1,394,138 $ 666,225 2.599,100 $3.265,325 $1,052,801 4,170,075 $5,222.876 Rounding Total support costs 3 $5,087,166 $5,080,997 $3,751,837 $13,920,000 Exhibit 3 GIBSON INSURANCE COMPANY Data Summary for New Allocation Bases Annuities Life Insurance Support Costs New Basis New In-Force New In-Force Policy acquisition Steps Calls 5 Customer service Sales and marketing Corporate overhead 0.5 0.2 0.6 0.4 Contacts 10 20 AUM $50,0 $50,000 $1,500 $65,000 00 outcome. After some thought and effort, she was able to collapse nearly 50 different corporate cost accounts into these 4 categories. Aggregated Corporate Support Costs for this Year $ 4,375,000 2,426,000 4,552,000 2,567,000 $ 13,920,000 Policy acquisition Customer service Sales and marketing Other corporate support Total Hampton knew that some of those aggregated costs were incurred to support new policies that had been issued during this year, while others supported in-force policies issued in previous years. As she dug further into the effort to issue and service policies, it was clear to her that there were distinct tasks repeated in, and different among, the various products. Those tasks, for example, included items such as underwriting reviews, health screenings/evaluations, billings, collections, records creation/maintenance, and responding to customer queries. It seemed like the sale of a policy spawned a flurry of corporate activity. She wondered if Gibson's processes were as streamlined and efficient as they could be, but she filed that thought away for a later date-the new cost allocation approach was her current imperative. It seemed to Hampton that there were a host of potential allocation bases that could be adopted in lieu of the currently used basis of the number of policies. She decided that there was merit in keeping the new approach simple (as best reflected in an underlying root cause for the cost), and acceptable to the departmental managers and product line managers who would be evaluated, in part, on their financial performance that involved the resulting allocations. Finally, Hampton decided to make her first attempt at using the new allocation bases as noted below. For each of the four new allocation bases, she presented herself with a test, which was to summarize her rationale for the allocation base in a brief, coherent, logical fashion. If she could not do that, then she must interpret that as a signal that she needed to investigate the proposed basis in more detail to settle on an intuitively defensible basis for that one. 1) Policy acquisition costs: New allocation basis: Number of steps involved in moving new policy applications to an in-force status. Rationale for new basis: The administrative staff at Gibson's headquarters processed new policy applications for all three legal entities and for both life insurance and annuity products. From an administrative staff resources perspective, annuities required two major steps to issue a policy: a review of the application data and the electronic imaging of the application. Life insurance policies required the same two steps as annuities, but they also required additional steps for the following administrative tasks pertaining to the underwriting work involved: generate files for reinsurance, review medical information Questions 1) Calculate the unit support cost per policy for new and in-force annuity and life insurance policies using the new allocation bases. In addition, calculate the total support costs to be reported by product for each legal business unit entity. 2) Why would Hampton want to track that information by product even if that level of detail was not required by regulators? 3) Will the new support cost allocation information help Gibson Insurance establish better pricing guidelines for the various annuities and life insurance products sold by each legal business unit entity? Why or why not? 4) Is there room for improvement in the means by which the corporate support costs are allocated under Hampton's new approach? If yes, in what way(s)? If no, why not? Exhibit 1 GIBSON INSURANCE COMPANY Number of Policies by Type and Business Unit for this Year Midwest Gibson Compton Total Annuities: New policies In-force policies 10,000 45,000 55.000 8,625 36.200 44.825 1,215 4,700 5.915 19,840 85,900 105,740 Subtotal Life insurance: New policies In-force policies 1,250 5,600 6,850 61.850 3,450 13,500 16.950 61,775 8,100 31,600 39,700 45,615 12,800 50,700 63,500 169,240 Subtotal Total Exhibit 2 GIBSON INSURANCE COMPANY Summary of Product Line and Business-Unit Support Cost Allocations Using the Number of Policies as the Allocation Basis ($13,920,000 + 169,240 policies = $82.25/policy) %3D Midwest Gibson Compton Total Annuities: New policies In-force policies Subtotal $ 822,500 3,701,250 $4,523,750 $ 709,406 2,977,450 $3,686,856 $ 99,934 386,575 $486,509 $1,631,840 7.065,275 $8,697,115 Life Insurance: New policies In-force policies Subtotal $102,813 460,600 $563.413 $ 283,763 1,110,375 $1,394,138 $ 666,225 2.599,100 $3.265,325 $1,052,801 4,170,075 $5,222.876 Rounding Total support costs 3 $5,087,166 $5,080,997 $3,751,837 $13,920,000 Exhibit 3 GIBSON INSURANCE COMPANY Data Summary for New Allocation Bases Annuities Life Insurance Support Costs New Basis New In-Force New In-Force Policy acquisition Steps Calls 5 Customer service Sales and marketing Corporate overhead 0.5 0.2 0.6 0.4 Contacts 10 20 AUM $50,0 $50,000 $1,500 $65,000 00 outcome. After some thought and effort, she was able to collapse nearly 50 different corporate cost accounts into these 4 categories. Aggregated Corporate Support Costs for this Year $ 4,375,000 2,426,000 4,552,000 2,567,000 $ 13,920,000 Policy acquisition Customer service Sales and marketing Other corporate support Total Hampton knew that some of those aggregated costs were incurred to support new policies that had been issued during this year, while others supported in-force policies issued in previous years. As she dug further into the effort to issue and service policies, it was clear to her that there were distinct tasks repeated in, and different among, the various products. Those tasks, for example, included items such as underwriting reviews, health screenings/evaluations, billings, collections, records creation/maintenance, and responding to customer queries. It seemed like the sale of a policy spawned a flurry of corporate activity. She wondered if Gibson's processes were as streamlined and efficient as they could be, but she filed that thought away for a later date-the new cost allocation approach was her current imperative. It seemed to Hampton that there were a host of potential allocation bases that could be adopted in lieu of the currently used basis of the number of policies. She decided that there was merit in keeping the new approach simple (as best reflected in an underlying root cause for the cost), and acceptable to the departmental managers and product line managers who would be evaluated, in part, on their financial performance that involved the resulting allocations. Finally, Hampton decided to make her first attempt at using the new allocation bases as noted below. For each of the four new allocation bases, she presented herself with a test, which was to summarize her rationale for the allocation base in a brief, coherent, logical fashion. If she could not do that, then she must interpret that as a signal that she needed to investigate the proposed basis in more detail to settle on an intuitively defensible basis for that one. 1) Policy acquisition costs: New allocation basis: Number of steps involved in moving new policy applications to an in-force status. Rationale for new basis: The administrative staff at Gibson's headquarters processed new policy applications for all three legal entities and for both life insurance and annuity products. From an administrative staff resources perspective, annuities required two major steps to issue a policy: a review of the application data and the electronic imaging of the application. Life insurance policies required the same two steps as annuities, but they also required additional steps for the following administrative tasks pertaining to the underwriting work involved: generate files for reinsurance, review medical information Questions 1) Calculate the unit support cost per policy for new and in-force annuity and life insurance policies using the new allocation bases. In addition, calculate the total support costs to be reported by product for each legal business unit entity. 2) Why would Hampton want to track that information by product even if that level of detail was not required by regulators? 3) Will the new support cost allocation information help Gibson Insurance establish better pricing guidelines for the various annuities and life insurance products sold by each legal business unit entity? Why or why not? 4) Is there room for improvement in the means by which the corporate support costs are allocated under Hampton's new approach? If yes, in what way(s)? If no, why not? Exhibit 1 GIBSON INSURANCE COMPANY Number of Policies by Type and Business Unit for this Year Midwest Gibson Compton Total Annuities: New policies In-force policies 10,000 45,000 55.000 8,625 36.200 44.825 1,215 4,700 5.915 19,840 85,900 105,740 Subtotal Life insurance: New policies In-force policies 1,250 5,600 6,850 61.850 3,450 13,500 16.950 61,775 8,100 31,600 39,700 45,615 12,800 50,700 63,500 169,240 Subtotal Total Exhibit 2 GIBSON INSURANCE COMPANY Summary of Product Line and Business-Unit Support Cost Allocations Using the Number of Policies as the Allocation Basis ($13,920,000 + 169,240 policies = $82.25/policy) %3D Midwest Gibson Compton Total Annuities: New policies In-force policies Subtotal $ 822,500 3,701,250 $4,523,750 $ 709,406 2,977,450 $3,686,856 $ 99,934 386,575 $486,509 $1,631,840 7.065,275 $8,697,115 Life Insurance: New policies In-force policies Subtotal $102,813 460,600 $563.413 $ 283,763 1,110,375 $1,394,138 $ 666,225 2.599,100 $3.265,325 $1,052,801 4,170,075 $5,222.876 Rounding Total support costs 3 $5,087,166 $5,080,997 $3,751,837 $13,920,000 Exhibit 3 GIBSON INSURANCE COMPANY Data Summary for New Allocation Bases Annuities Life Insurance Support Costs New Basis New In-Force New In-Force Policy acquisition Steps Calls 5 Customer service Sales and marketing Corporate overhead 0.5 0.2 0.6 0.4 Contacts 10 20 AUM $50,0 $50,000 $1,500 $65,000 00 outcome. After some thought and effort, she was able to collapse nearly 50 different corporate cost accounts into these 4 categories. Aggregated Corporate Support Costs for this Year $ 4,375,000 2,426,000 4,552,000 2,567,000 $ 13,920,000 Policy acquisition Customer service Sales and marketing Other corporate support Total Hampton knew that some of those aggregated costs were incurred to support new policies that had been issued during this year, while others supported in-force policies issued in previous years. As she dug further into the effort to issue and service policies, it was clear to her that there were distinct tasks repeated in, and different among, the various products. Those tasks, for example, included items such as underwriting reviews, health screenings/evaluations, billings, collections, records creation/maintenance, and responding to customer queries. It seemed like the sale of a policy spawned a flurry of corporate activity. She wondered if Gibson's processes were as streamlined and efficient as they could be, but she filed that thought away for a later date-the new cost allocation approach was her current imperative. It seemed to Hampton that there were a host of potential allocation bases that could be adopted in lieu of the currently used basis of the number of policies. She decided that there was merit in keeping the new approach simple (as best reflected in an underlying root cause for the cost), and acceptable to the departmental managers and product line managers who would be evaluated, in part, on their financial performance that involved the resulting allocations. Finally, Hampton decided to make her first attempt at using the new allocation bases as noted below. For each of the four new allocation bases, she presented herself with a test, which was to summarize her rationale for the allocation base in a brief, coherent, logical fashion. If she could not do that, then she must interpret that as a signal that she needed to investigate the proposed basis in more detail to settle on an intuitively defensible basis for that one. 1) Policy acquisition costs: New allocation basis: Number of steps involved in moving new policy applications to an in-force status. Rationale for new basis: The administrative staff at Gibson's headquarters processed new policy applications for all three legal entities and for both life insurance and annuity products. From an administrative staff resources perspective, annuities required two major steps to issue a policy: a review of the application data and the electronic imaging of the application. Life insurance policies required the same two steps as annuities, but they also required additional steps for the following administrative tasks pertaining to the underwriting work involved: generate files for reinsurance, review medical information Questions 1) Calculate the unit support cost per policy for new and in-force annuity and life insurance policies using the new allocation bases. In addition, calculate the total support costs to be reported by product for each legal business unit entity. 2) Why would Hampton want to track that information by product even if that level of detail was not required by regulators? 3) Will the new support cost allocation information help Gibson Insurance establish better pricing guidelines for the various annuities and life insurance products sold by each legal business unit entity? Why or why not? 4) Is there room for improvement in the means by which the corporate support costs are allocated under Hampton's new approach? If yes, in what way(s)? If no, why not? Exhibit 1 GIBSON INSURANCE COMPANY Number of Policies by Type and Business Unit for this Year Midwest Gibson Compton Total Annuities: New policies In-force policies 10,000 45,000 55.000 8,625 36.200 44.825 1,215 4,700 5.915 19,840 85,900 105,740 Subtotal Life insurance: New policies In-force policies 1,250 5,600 6,850 61.850 3,450 13,500 16.950 61,775 8,100 31,600 39,700 45,615 12,800 50,700 63,500 169,240 Subtotal Total Exhibit 2 GIBSON INSURANCE COMPANY Summary of Product Line and Business-Unit Support Cost Allocations Using the Number of Policies as the Allocation Basis ($13,920,000 + 169,240 policies = $82.25/policy) %3D Midwest Gibson Compton Total Annuities: New policies In-force policies Subtotal $ 822,500 3,701,250 $4,523,750 $ 709,406 2,977,450 $3,686,856 $ 99,934 386,575 $486,509 $1,631,840 7.065,275 $8,697,115 Life Insurance: New policies In-force policies Subtotal $102,813 460,600 $563.413 $ 283,763 1,110,375 $1,394,138 $ 666,225 2.599,100 $3.265,325 $1,052,801 4,170,075 $5,222.876 Rounding Total support costs 3 $5,087,166 $5,080,997 $3,751,837 $13,920,000 Exhibit 3 GIBSON INSURANCE COMPANY Data Summary for New Allocation Bases Annuities Life Insurance Support Costs New Basis New In-Force New In-Force Policy acquisition Steps Calls 5 Customer service Sales and marketing Corporate overhead 0.5 0.2 0.6 0.4 Contacts 10 20 AUM $50,0 $50,000 $1,500 $65,000 00 outcome. After some thought and effort, she was able to collapse nearly 50 different corporate cost accounts into these 4 categories. Aggregated Corporate Support Costs for this Year $ 4,375,000 2,426,000 4,552,000 2,567,000 $ 13,920,000 Policy acquisition Customer service Sales and marketing Other corporate support Total Hampton knew that some of those aggregated costs were incurred to support new policies that had been issued during this year, while others supported in-force policies issued in previous years. As she dug further into the effort to issue and service policies, it was clear to her that there were distinct tasks repeated in, and different among, the various products. Those tasks, for example, included items such as underwriting reviews, health screenings/evaluations, billings, collections, records creation/maintenance, and responding to customer queries. It seemed like the sale of a policy spawned a flurry of corporate activity. She wondered if Gibson's processes were as streamlined and efficient as they could be, but she filed that thought away for a later date-the new cost allocation approach was her current imperative. It seemed to Hampton that there were a host of potential allocation bases that could be adopted in lieu of the currently used basis of the number of policies. She decided that there was merit in keeping the new approach simple (as best reflected in an underlying root cause for the cost), and acceptable to the departmental managers and product line managers who would be evaluated, in part, on their financial performance that involved the resulting allocations. Finally, Hampton decided to make her first attempt at using the new allocation bases as noted below. For each of the four new allocation bases, she presented herself with a test, which was to summarize her rationale for the allocation base in a brief, coherent, logical fashion. If she could not do that, then she must interpret that as a signal that she needed to investigate the proposed basis in more detail to settle on an intuitively defensible basis for that one. 1) Policy acquisition costs: New allocation basis: Number of steps involved in moving new policy applications to an in-force status. Rationale for new basis: The administrative staff at Gibson's headquarters processed new policy applications for all three legal entities and for both life insurance and annuity products. From an administrative staff resources perspective, annuities required two major steps to issue a policy: a review of the application data and the electronic imaging of the application. Life insurance policies required the same two steps as annuities, but they also required additional steps for the following administrative tasks pertaining to the underwriting work involved: generate files for reinsurance, review medical information Questions 1) Calculate the unit support cost per policy for new and in-force annuity and life insurance policies using the new allocation bases. In addition, calculate the total support costs to be reported by product for each legal business unit entity. 2) Why would Hampton want to track that information by product even if that level of detail was not required by regulators? 3) Will the new support cost allocation information help Gibson Insurance establish better pricing guidelines for the various annuities and life insurance products sold by each legal business unit entity? Why or why not? 4) Is there room for improvement in the means by which the corporate support costs are allocated under Hampton's new approach? If yes, in what way(s)? If no, why not? Exhibit 1 GIBSON INSURANCE COMPANY Number of Policies by Type and Business Unit for this Year Midwest Gibson Compton Total Annuities: New policies In-force policies 10,000 45,000 55.000 8,625 36.200 44.825 1,215 4,700 5.915 19,840 85,900 105,740 Subtotal Life insurance: New policies In-force policies 1,250 5,600 6,850 61.850 3,450 13,500 16.950 61,775 8,100 31,600 39,700 45,615 12,800 50,700 63,500 169,240 Subtotal Total Exhibit 2 GIBSON INSURANCE COMPANY Summary of Product Line and Business-Unit Support Cost Allocations Using the Number of Policies as the Allocation Basis ($13,920,000 + 169,240 policies = $82.25/policy) %3D Midwest Gibson Compton Total Annuities: New policies In-force policies Subtotal $ 822,500 3,701,250 $4,523,750 $ 709,406 2,977,450 $3,686,856 $ 99,934 386,575 $486,509 $1,631,840 7.065,275 $8,697,115 Life Insurance: New policies In-force policies Subtotal $102,813 460,600 $563.413 $ 283,763 1,110,375 $1,394,138 $ 666,225 2.599,100 $3.265,325 $1,052,801 4,170,075 $5,222.876 Rounding Total support costs 3 $5,087,166 $5,080,997 $3,751,837 $13,920,000 Exhibit 3 GIBSON INSURANCE COMPANY Data Summary for New Allocation Bases Annuities Life Insurance Support Costs New Basis New In-Force New In-Force Policy acquisition Steps Calls 5 Customer service Sales and marketing Corporate overhead 0.5 0.2 0.6 0.4 Contacts 10 20 AUM $50,0 $50,000 $1,500 $65,000 00 outcome. After some thought and effort, she was able to collapse nearly 50 different corporate cost accounts into these 4 categories. Aggregated Corporate Support Costs for this Year $ 4,375,000 2,426,000 4,552,000 2,567,000 $ 13,920,000 Policy acquisition Customer service Sales and marketing Other corporate support Total Hampton knew that some of those aggregated costs were incurred to support new policies that had been issued during this year, while others supported in-force policies issued in previous years. As she dug further into the effort to issue and service policies, it was clear to her that there were distinct tasks repeated in, and different among, the various products. Those tasks, for example, included items such as underwriting reviews, health screenings/evaluations, billings, collections, records creation/maintenance, and responding to customer queries. It seemed like the sale of a policy spawned a flurry of corporate activity. She wondered if Gibson's processes were as streamlined and efficient as they could be, but she filed that thought away for a later date-the new cost allocation approach was her current imperative. It seemed to Hampton that there were a host of potential allocation bases that could be adopted in lieu of the currently used basis of the number of policies. She decided that there was merit in keeping the new approach simple (as best reflected in an underlying root cause for the cost), and acceptable to the departmental managers and product line managers who would be evaluated, in part, on their financial performance that involved the resulting allocations. Finally, Hampton decided to make her first attempt at using the new allocation bases as noted below. For each of the four new allocation bases, she presented herself with a test, which was to summarize her rationale for the allocation base in a brief, coherent, logical fashion. If she could not do that, then she must interpret that as a signal that she needed to investigate the proposed basis in more detail to settle on an intuitively defensible basis for that one. 1) Policy acquisition costs: New allocation basis: Number of steps involved in moving new policy applications to an in-force status. Rationale for new basis: The administrative staff at Gibson's headquarters processed new policy applications for all three legal entities and for both life insurance and annuity products. From an administrative staff resources perspective, annuities required two major steps to issue a policy: a review of the application data and the electronic imaging of the application. Life insurance policies required the same two steps as annuities, but they also required additional steps for the following administrative tasks pertaining to the underwriting work involved: generate files for reinsurance, review medical information Questions 1) Calculate the unit support cost per policy for new and in-force annuity and life insurance policies using the new allocation bases. In addition, calculate the total support costs to be reported by product for each legal business unit entity. 2) Why would Hampton want to track that information by product even if that level of detail was not required by regulators? 3) Will the new support cost allocation information help Gibson Insurance establish better pricing guidelines for the various annuities and life insurance products sold by each legal business unit entity? Why or why not? 4) Is there room for improvement in the means by which the corporate support costs are allocated under Hampton's new approach? If yes, in what way(s)? If no, why not?

Expert Answer:

Answer rating: 100% (QA)

1 2 Better and appropriate allocation approach can help management obtain more accurate insight on p... View the full answer

Related Book For

Principles of Auditing and Other Assurance Services

ISBN: 978-0078025617

19th edition

Authors: Ray Whittington, Kurt Pany

Posted Date:

Students also viewed these finance questions

-

Recall that Yield Curve is the graph of bond yields as a function of their maturity (2y, 3y, 5y, 10y, ...). Assume a 2-year bond with semi-annual coupon rate of 2.25% p.a. has semi-annual yield of 2%...

-

Estimate the amount of money accounts payable and cash disbursements departments could save if a basic batch-processing system were implemented. Assume that the clerical workers cost the firm $12 per...

-

Estimate the amount of energy required to sublimate the 4 kg of water contained in the frozen clothes in a northern state which are at - 20°C. See Fig. 2.35. Figure 2.35

-

What is the result of executing the following method? A. The declaration of name does not compile. B. The declaration of _number does not compile. C. The declaration of profit$$$ does not compile. D....

-

Pineapple Ltd uses three activity pools to assign costs to customers in order to assess customer profitability. Each activity cost pool has a unique cost driver to apply indirect costs to customers....

-

An inventor claims to have built a machine that operates as follows: 100 kg/min of steam at T = 400C and P = 5 bar enters the machine. 100 kg/min of saturated liquid water at 40C leaves the machine....

-

In a differential pulley block, the diameter of the smaller pulley is 9/10 th of the larger pulley. Find the load lifted by the block with an effort of 200 N if the efficiency is 45%.

-

A little more than 10 months ago, Luke Weaver, a mortgage banker in Phoenix, bought 300 shares of stock at $40 per share. Since then, the price of the stock has risen to $75 per share. It is now near...

-

What does the textbook, Introduction to Forensic Psychology recommend regarding a specialized degree in forensic psychology?

-

The propeller in Prob. 9.1 is replaced with a six-blade turbine 400 mm in diameter, and the fluid to be agitated is a pseudoplastic power law liquid having an apparent viscosity of 15 P when the...

-

Spending the money on opening a new locatioSelect all that apply The required rate of return (Check all that apply.) Multiple select question. is the minimum rate of return a project must yield to be...

-

Research market data and trends in portfolio management and summarize the trend that you believe will impact portfolio management the greatest in the years ahead, use your independent research to...

-

A loan of $ 1 0 , 0 0 0 is being repaid with annual payments of $ 1 , 5 0 0 for n years. The total principal paid in the first payment is $ 6 8 5 . 5 8 . Calculate the interest rate on the loan....

-

What causes the most uncertainty about your personal finance? getting started, taking action, or evaluating progress and taking the necessary corrective action with regards to your finances? How is...

-

Review Tesla's economic profit trend for the past five years. Is this trending in the right direction, too high, too low, misrepresented because of some factor? How or why?

-

A. Three and a half years ago, Bob purchased 1200 units of a fund with an NAV of $16.75. The NAV is now $36.50 and the fund had a 7 percent redemption fee declining at 1 percent per year and based on...

-

calculate the following financial rations for the clements. liquid assets / monthly nondescretionary expenses

-

You've been asked to take over leadership of a group of paralegals that once had a reputation for being a tight-knit, supportive team, but you quickly figure out that this team is in danger of...

-

Trend analysis, common-size financial statements, and ratios are presented for the Brody Corporation in Figure. Assume that you are auditing Brodys financial statements for the year ended 12/31/X8....

-

Wanda Young, doing business as Wanda Young Fashions, engaged the CPA partnership of Scott & Green to audit her financial statements. During the audit, Scott & Green discovered certain irregularities...

-

The controller of a new client company informs you that most of the inventories are stored in bonded public warehouses. He presents warehouse receipts to account for the inventories. Will careful...

-

Suppose you increase the gauge pressure in the tires of your car by \(10 \%\). (a) How does the area of the tires in contact with a level road change? (b) If the gauge pressure in the tires is \(2.0...

-

In a service station's hydraulic lift, the diameter of the large piston is \(200 \mathrm{~mm}\) and the diameter of the small piston is \(30 \mathrm{~mm}\). Force is exerted on the small piston by an...

-

Initially, both legs of a mercury manometer are open to the atmosphere, and the mercury height in the left leg is \(40.0 \mathrm{~mm}\). You inflate a balloon until it has a surface area of \(0.300...

Study smarter with the SolutionInn App