Question: #Accounting Answer problem 10-7 and problem 10-8 Problem 10-7 Other Components of Shareholders' Equity Share capital, 10,000 shares at P100 par Share premium P1,000,000 Subscribed

#Accounting

Answer problem 10-7 and problem 10-8

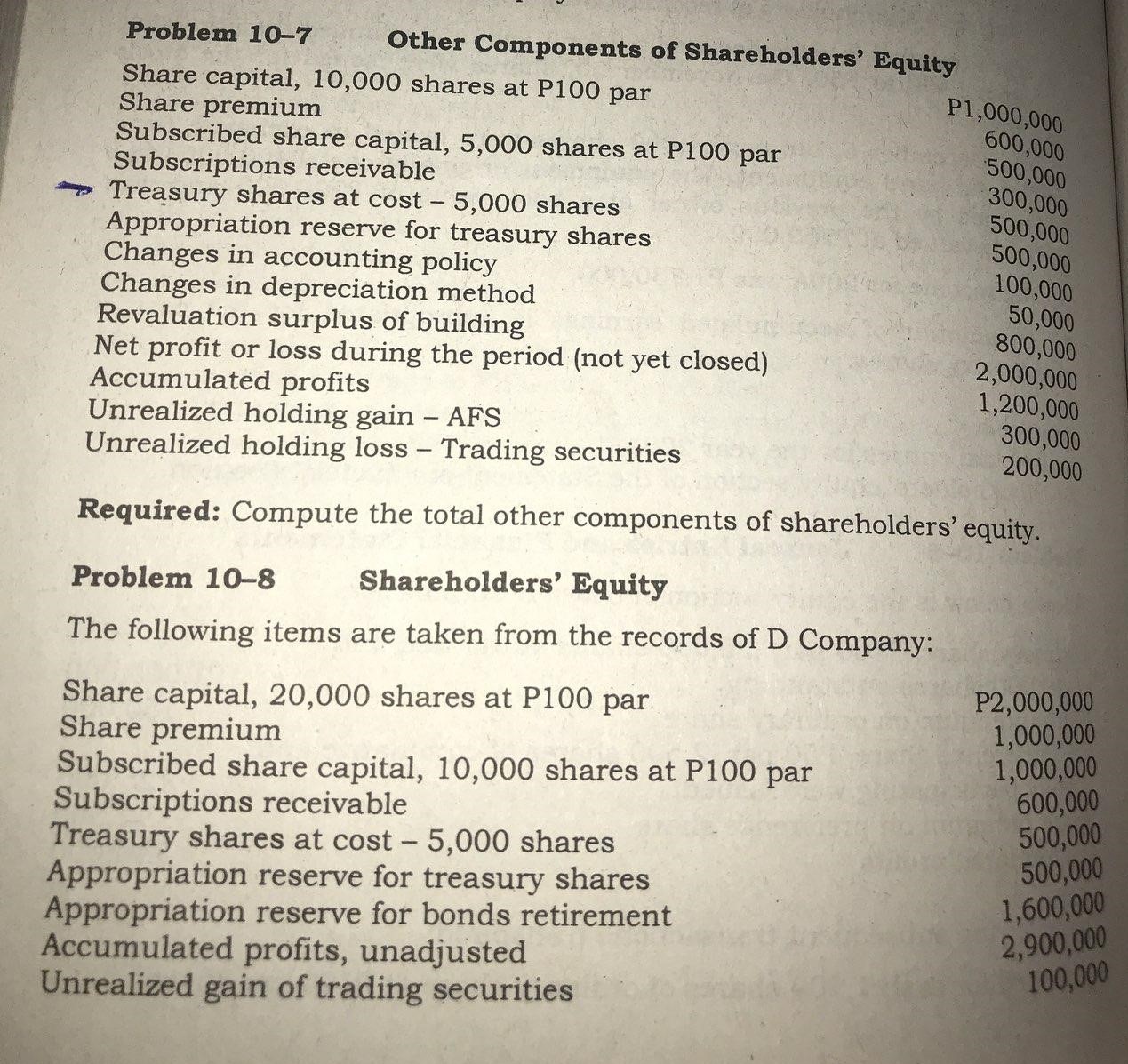

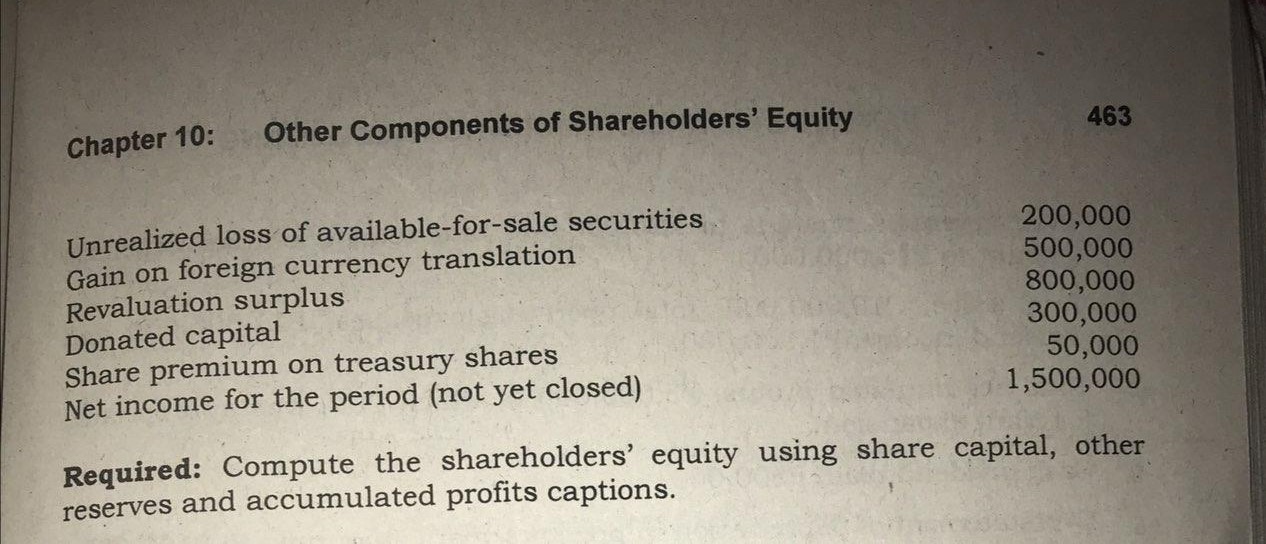

Problem 10-7 Other Components of Shareholders' Equity Share capital, 10,000 shares at P100 par Share premium P1,000,000 Subscribed share capital, 5,000 shares at P100 par 600,000 Subscriptions receivable 500,000 Treasury shares at cost - 5,000 shares 300,000 Appropriation reserve for treasury shares 500,000 Changes in accounting policy 500,000 Changes in depreciation method 100,000 Revaluation surplus of building 50,000 Net profit or loss during the period (not yet closed) 800,000 Accumulated profits 2,000,000 Unrealized holding gain - AFS 1,200,000 300,000 Unrealized holding loss - Trading securities 200,000 Required: Compute the total other components of shareholders' equity. Problem 10-8 Shareholders' Equity The following items are taken from the records of D Company: Share capital, 20,000 shares at P100 par P2,000,000 Share premium 1,000,000 Subscribed share capital, 10,000 shares at P100 par 1,000,000 Subscriptions receivable 600,000 Treasury shares at cost - 5,000 shares 500,000 Appropriation reserve for treasury shares 500,000 Appropriation reserve for bonds retirement 1,600,000 Accumulated profits, unadjusted 2,900,000 Unrealized gain of trading securities 100,000Chapter 10: Other Components of Shareholders' Equity 463 Unrealized loss of available-for-sale securities Gain on foreign currency translation 200,000 Revaluation surplus 500,000 Donated capital 800,000 300,000 Share premium on treasury shares Net income for the period (not yet closed) 50,000 1,500,000 Required: Compute the shareholders' equity using share capital, other reserves and accumulated profits captions

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts