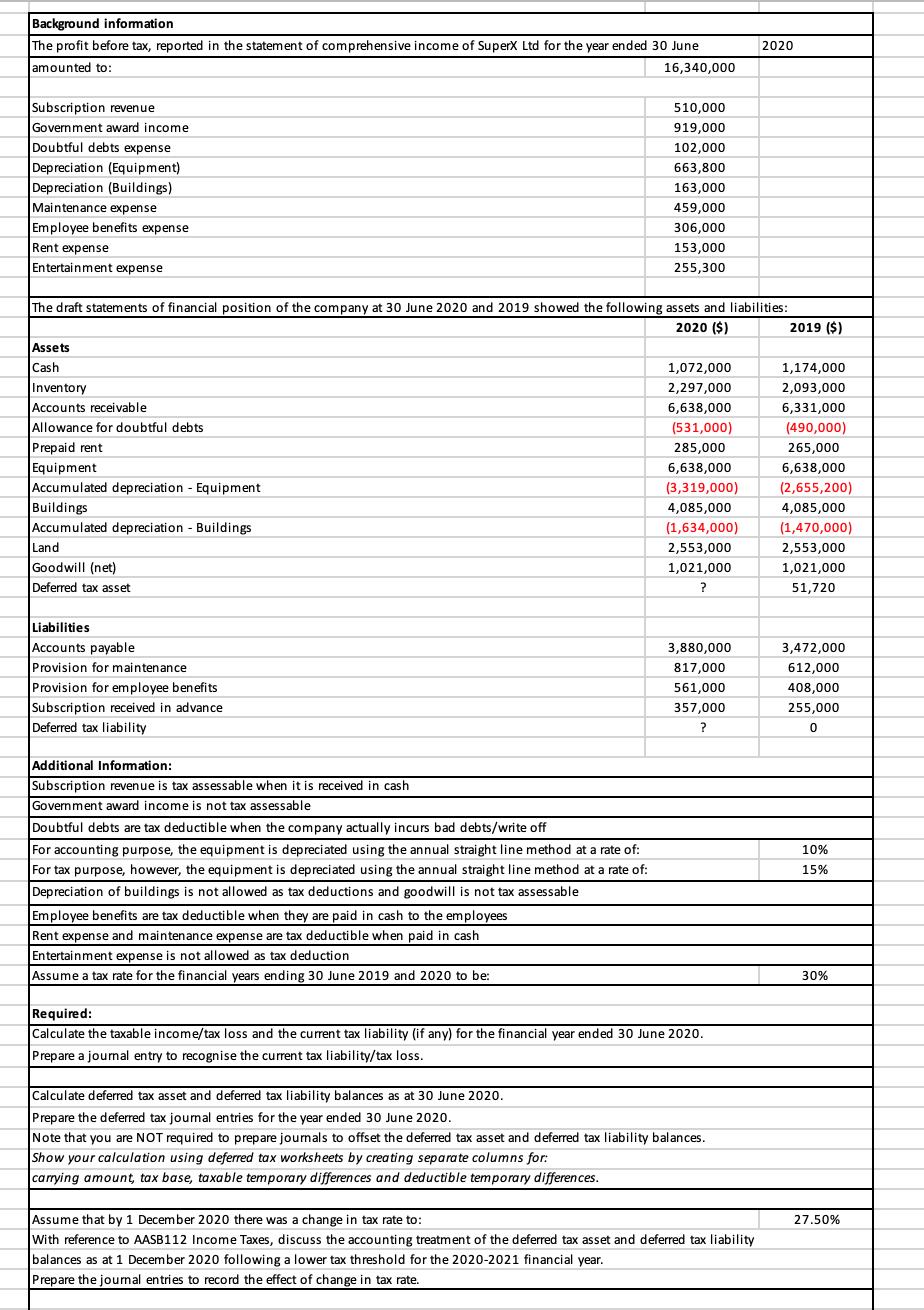

Assume that by 1 December 2020 there was a change in the tax rate. With reference to

Fantastic news! We've Found the answer you've been seeking!

Question:

Assume that by 1 December 2020 there was a change in the tax rate. With reference to AASB112 Income Taxes, discuss the accounting treatment of the deferred tax asset and deferred tax liability balances as of 1 December 2020 following a lower tax threshold for the 2020-2021 financial year. Prepare the journal entries to record the effect of change in the tax rate.

Expert Answer:

Computation of taxable incomeTax loss for the year ended 3062020 Particulars Value Profit as per BOA 16340000 Add back Doubtful debt expense 102000 De... View the full answer

Related Book For

Federal Taxation 2017 Comprehensive

ISBN: 9780134421438

30th edition

Authors: Thomas R. Pope, Timothy J. Rupert, Kenneth E. Anderson

Posted Date: