In 2005, Bob Moyer was reviewing production costs for Mile High Cycles. Located in Denver, Colorado,...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

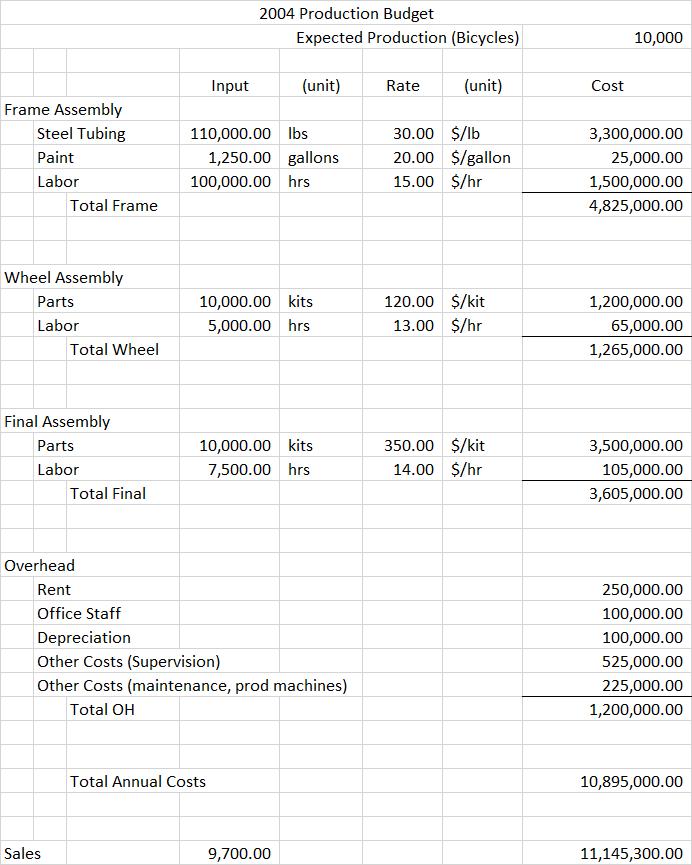

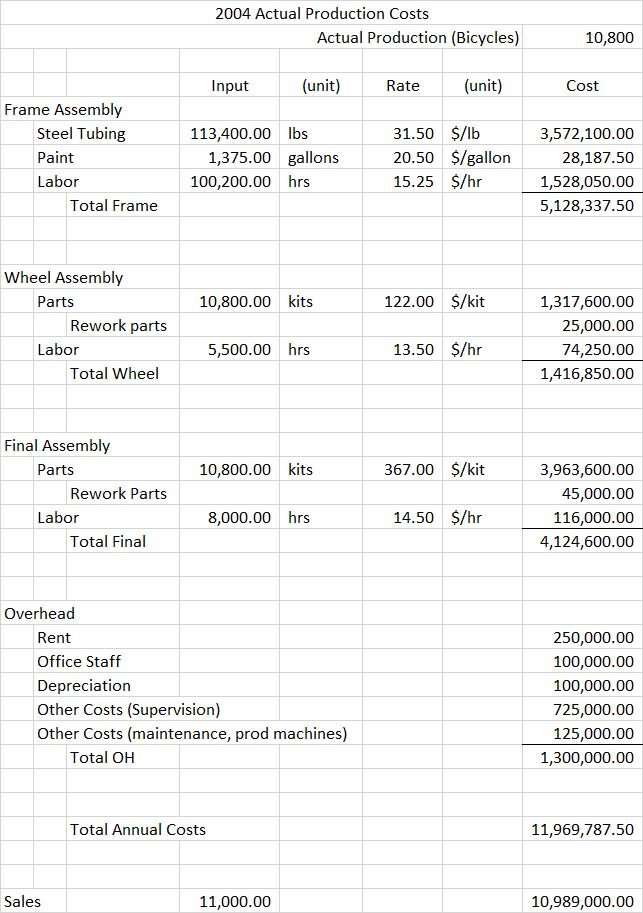

In 2005, Bob Moyer was reviewing production costs for Mile High Cycles. Located in Denver, Colorado, the company sold very high-quality, handcrafted mountain bikes to bicycle retailers throughout the country. Sales for the company were $13 million that year. Bob Moyer had been an avid cyclist in college, racing for the Stanford University cycling team while completing his degree in mechanical engineering. After working for a few years as a design engineer for a company in Denver, Bob decided to start his own business. As a hobby, he had designed and built several prototypes of a mountain bike, which had been enthusiastically received by his mountain-biking friends. Approaching several friends and relatives for start-up money, Mile High Cycles was founded in 2003. A mountain bike was a bicycle with 15 to 21 speeds, designed and built to take the punishment of riding on dirt trails and roads. The bikes were first made by avid cyclists who customized their 10- speed road bikes in order to ride on mountain trails and dirt roads. Some with framebuilding experience began to experiment making their own frames in order to handle better the additional demands of off-road riding. By 1992, several small companies had emerged selling bicycles specifically designed for riding under these conditions. During the rest of the 1990s, mountain bikes had taken off in popularity, not only for use off-road but also for use in the city, where their sturdy construction could withstand the pounding from potholes and curbs. In addition, many casual cyclists preferred the mountain bike's more upright riding position in comparison to that of the hunched position of the 10-speed road bike. Sales of all bicycles in the United States had declined in 2003. However, over the same time period, sales of mountain bikes increased to more than 2.0 million units. Bob Moyer had planned to produce 10,000 bikes in 2004, all of one model. Operations at Mile High Cycles consisted of three departments: frames, wheel assembly, and final assembly. In frames, steel tubing was cut to length for the components of the frame. Then the pieces were carefully welded together to form the completed frameset. This part of the process was quite time-consuming, requiring frequent inspection and measurement to ensure that the frameset was aligned perfectly. After welding, the frame was painted in one of 10 different color schemes and prepared for final assembly. In wheel assembly, front and rear wheels were assembled from their key components: hubs, spokes, and rims. All of the components were purchased from an outside supplier. Mile High Cycles used a high-quality automatic lacing and truing machine to build its wheels. This machine would lace the spokes between the hub and rim and then automatically tighten the spokes to the appropriate tension. The machine was quite precise but would occasionally damage spokes during the insertion process. In such a case, the operator would replace any damaged parts and restart the machine. Each wheel would also be inspected and trued by hand in order to insure that the wheels were in perfect alignment. In final assembly, the frame and wheels were combined with other purchased parts to create the final package that would then be shipped to bicycle dealers. In this area, the front fork and many other key components were attached to the frame, and the inner tubes and tires were mounted on the wheels. In order to minimize damage while shipping, some of the bicycles' components were left packaged for the bicycle dealer to assemble before selling the bike to the final customer. All of the components were purchased from outside suppliers and then were combined to form kits for the bicycles. Mile High Cycles carried an inventory of spare parts to replace any parts damaged during assembly or shipping, although such replacement was quite infrequent. In reviewing his costs, Bob noted that he had produced 10,800 bicycles in 2004, 800 more than planned. Bob thought that operations during the year had done well to meet the additional demand, but he wondered if Mile High Cycles was doing a good job in managing its costs. Exhibit 1 shows the planned material, labor, and overhead costs for 2004. Exhibit 2 shows the actual material, labor, and overhead costs for that year. Questions 1. Determine the direct cost and overhead variances. What might be causing each of the variances to occur? 2. Should Bob Moyer be concerned about Mile High Cycles's performance? Where should he be prepared to direct his attention? What additional information should he try to obtain? 3. Are there any purposes for which a total, per unit variance would be more useful than a series of functional variances? If so, for what? 2004 Production Budget Expected Production (Bicycles) 10,000 Input (unit) Rate (unit) Cost Frame Assembly 30.00 $/lb 20.00 $/gallon Steel Tubing 110,000.00 Ibs 3,300,000.00 Paint 1,250.00 gallons 25,000.00 Labor 100,000.00 hrs 15.00 $/hr 1,500,000.00 Total Frame 4,825,000.00 Wheel Assembly Parts 10,000.00 kits 120.00 $/kit 1,200,000.00 Labor 5,000.00 hrs 13.00 $/hr 65,000.00 Total Wheel 1,265,000.00 Final Assembly Parts 10,000.00 kits 350.00 $/kit 3,500,000.00 Labor 7,500.00 hrs 14.00 $/hr 105,000.00 Total Final 3,605,000.00 Overhead Rent 250,000.00 Office Staff 100,000.00 Depreciation 100,000.00 Other Costs (Supervision) 525,000.00 Other Costs (maintenance, prod machines) 225,000.00 Total OH 1,200,000.00 Total Annual Costs 10,895,000.00 Sales 9,700.00 11,145,300.00 2004 Actual Production Costs Actual Production (Bicycles) 10,800 Input (unit) Rate (unit) Cost Frame Assembly Steel Tubing 113,400.00 Ibs 31.50 $/lb 3,572,100.00 20.50 $/gallon 15.25 $/hr Paint 1,375.00 gallons 28,187.50 Labor 100,200.00 hrs 1,528,050.00 Total Frame 5,128,337.50 Wheel Assembly Parts 10,800.00 kits 122.00 $/kit 1,317,600.00 Rework parts 25,000.00 Labor 5,500.00 hrs 13.50 $/hr 74,250.00 Total Wheel 1,416,850.00 Final Assembly Parts 10,800.00 kits 367.00 $/kit 3,963,600.00 Rework Parts 45,000.00 Labor 8,000.00 hrs 14.50 $/hr 116,000.00 Total Final 4,124,600.00 Overhead Rent 250,000.00 Office Staff 100,000.00 Depreciation 100,000.00 Other Costs (Supervision) 725,000.00 Other Costs (maintenance, prod machines) 125,000.00 Total OH 1,300,000.00 Total Annual Costs 11,969,787.50 Sales 11,000.00 10,989,000.00 In 2005, Bob Moyer was reviewing production costs for Mile High Cycles. Located in Denver, Colorado, the company sold very high-quality, handcrafted mountain bikes to bicycle retailers throughout the country. Sales for the company were $13 million that year. Bob Moyer had been an avid cyclist in college, racing for the Stanford University cycling team while completing his degree in mechanical engineering. After working for a few years as a design engineer for a company in Denver, Bob decided to start his own business. As a hobby, he had designed and built several prototypes of a mountain bike, which had been enthusiastically received by his mountain-biking friends. Approaching several friends and relatives for start-up money, Mile High Cycles was founded in 2003. A mountain bike was a bicycle with 15 to 21 speeds, designed and built to take the punishment of riding on dirt trails and roads. The bikes were first made by avid cyclists who customized their 10- speed road bikes in order to ride on mountain trails and dirt roads. Some with framebuilding experience began to experiment making their own frames in order to handle better the additional demands of off-road riding. By 1992, several small companies had emerged selling bicycles specifically designed for riding under these conditions. During the rest of the 1990s, mountain bikes had taken off in popularity, not only for use off-road but also for use in the city, where their sturdy construction could withstand the pounding from potholes and curbs. In addition, many casual cyclists preferred the mountain bike's more upright riding position in comparison to that of the hunched position of the 10-speed road bike. Sales of all bicycles in the United States had declined in 2003. However, over the same time period, sales of mountain bikes increased to more than 2.0 million units. Bob Moyer had planned to produce 10,000 bikes in 2004, all of one model. Operations at Mile High Cycles consisted of three departments: frames, wheel assembly, and final assembly. In frames, steel tubing was cut to length for the components of the frame. Then the pieces were carefully welded together to form the completed frameset. This part of the process was quite time-consuming, requiring frequent inspection and measurement to ensure that the frameset was aligned perfectly. After welding, the frame was painted in one of 10 different color schemes and prepared for final assembly. In wheel assembly, front and rear wheels were assembled from their key components: hubs, spokes, and rims. All of the components were purchased from an outside supplier. Mile High Cycles used a high-quality automatic lacing and truing machine to build its wheels. This machine would lace the spokes between the hub and rim and then automatically tighten the spokes to the appropriate tension. The machine was quite precise but would occasionally damage spokes during the insertion process. In such a case, the operator would replace any damaged parts and restart the machine. Each wheel would also be inspected and trued by hand in order to insure that the wheels were in perfect alignment. In final assembly, the frame and wheels were combined with other purchased parts to create the final package that would then be shipped to bicycle dealers. In this area, the front fork and many other key components were attached to the frame, and the inner tubes and tires were mounted on the wheels. In order to minimize damage while shipping, some of the bicycles' components were left packaged for the bicycle dealer to assemble before selling the bike to the final customer. All of the components were purchased from outside suppliers and then were combined to form kits for the bicycles. Mile High Cycles carried an inventory of spare parts to replace any parts damaged during assembly or shipping, although such replacement was quite infrequent. In reviewing his costs, Bob noted that he had produced 10,800 bicycles in 2004, 800 more than planned. Bob thought that operations during the year had done well to meet the additional demand, but he wondered if Mile High Cycles was doing a good job in managing its costs. Exhibit 1 shows the planned material, labor, and overhead costs for 2004. Exhibit 2 shows the actual material, labor, and overhead costs for that year. Questions 1. Determine the direct cost and overhead variances. What might be causing each of the variances to occur? 2. Should Bob Moyer be concerned about Mile High Cycles's performance? Where should he be prepared to direct his attention? What additional information should he try to obtain? 3. Are there any purposes for which a total, per unit variance would be more useful than a series of functional variances? If so, for what? 2004 Production Budget Expected Production (Bicycles) 10,000 Input (unit) Rate (unit) Cost Frame Assembly 30.00 $/lb 20.00 $/gallon Steel Tubing 110,000.00 Ibs 3,300,000.00 Paint 1,250.00 gallons 25,000.00 Labor 100,000.00 hrs 15.00 $/hr 1,500,000.00 Total Frame 4,825,000.00 Wheel Assembly Parts 10,000.00 kits 120.00 $/kit 1,200,000.00 Labor 5,000.00 hrs 13.00 $/hr 65,000.00 Total Wheel 1,265,000.00 Final Assembly Parts 10,000.00 kits 350.00 $/kit 3,500,000.00 Labor 7,500.00 hrs 14.00 $/hr 105,000.00 Total Final 3,605,000.00 Overhead Rent 250,000.00 Office Staff 100,000.00 Depreciation 100,000.00 Other Costs (Supervision) 525,000.00 Other Costs (maintenance, prod machines) 225,000.00 Total OH 1,200,000.00 Total Annual Costs 10,895,000.00 Sales 9,700.00 11,145,300.00 2004 Actual Production Costs Actual Production (Bicycles) 10,800 Input (unit) Rate (unit) Cost Frame Assembly Steel Tubing 113,400.00 Ibs 31.50 $/lb 3,572,100.00 20.50 $/gallon 15.25 $/hr Paint 1,375.00 gallons 28,187.50 Labor 100,200.00 hrs 1,528,050.00 Total Frame 5,128,337.50 Wheel Assembly Parts 10,800.00 kits 122.00 $/kit 1,317,600.00 Rework parts 25,000.00 Labor 5,500.00 hrs 13.50 $/hr 74,250.00 Total Wheel 1,416,850.00 Final Assembly Parts 10,800.00 kits 367.00 $/kit 3,963,600.00 Rework Parts 45,000.00 Labor 8,000.00 hrs 14.50 $/hr 116,000.00 Total Final 4,124,600.00 Overhead Rent 250,000.00 Office Staff 100,000.00 Depreciation 100,000.00 Other Costs (Supervision) 725,000.00 Other Costs (maintenance, prod machines) 125,000.00 Total OH 1,300,000.00 Total Annual Costs 11,969,787.50 Sales 11,000.00 10,989,000.00

Expert Answer:

Answer rating: 100% (QA)

From the given details of a mountain bike manufacturing company the variance in direct cost and over head along with a description of causes for such variation is to be found Find the variance for Dir... View the full answer

Related Book For

Accounting concepts and applications

ISBN: 978-0538745482

11th Edition

Authors: Albrecht Stice, Stice Swain

Posted Date:

Students also viewed these organizational behavior questions

-

You are to research and write a paper in your own words about the WorldCom, Inc. scandal. In your paper, and in your own words, specifically discuss the following topics: Discuss Cynthia Coopers role...

-

In your own words describe a CFE.

-

Using an example, explain in your own words the function of a statement of cash flows. Why is it prepared? What does it communicate to the reader of financial statements? What is its advantage over a...

-

On 1 June 2019, Manchester United Ltd bought 48 million ordinary shares in Chelsea FC Ltd paying GHS 280 million cash. The summarised statement of financial position for the two entities as at 31...

-

A pizza place offers the choice of the following toppings: extra cheese, mushrooms, pepperoni, ham, sausage, onions, and green peppers. Assume that each pizza must have at least 1 topping and that...

-

Presented below is information related to copyrights owned by Wamser Corporation at December 31, 2008. Cost ................2700000 Carrying Amount ..........2400000 Expected Future Net Cash Flows...

-

Describe the differences between black box and white box component modeling.

-

Kelley Company has completed Octobers sales and purchases journals (Shown below). a. Total and post the journals to T accounts for the general ledger and the accounts receivable and accounts payable...

-

a. $30,000 W of supplies is purchased with casi. Supplies Cash Accounts Supplies Debit $30,000 Credit $30,000 $30,000 Cash $30,000 b. $10,000 worth of supplies is used to provide clients with goods...

-

Cinder and PQ are associated [ITA 256(1)(a)] and connected [ITA 186(4)] for tax purposes. Cinder Inc. is a Canadian-controlled private corporation based in your province. The company operates a...

-

Chris and Sarah Miller are both employed. Chris is a clinic business manager and Sarah is a registered nurse. Both work for employers that offer 401(k) plans. Chris will make $126,000 as an...

-

Define the following: shooting rights G&G costs carrying costs dry-hole contribution bottom-hole contribution

-

What is synthetic crude oil?

-

Which of the following are defined as exploration costs? a. Drilling and equipping exploratory wells b. Drilling exploratory-type stratigraphic test wells c. Dry-hole contributions d. Bottom-hole...

-

Which of the following type(s) of accounting uses the successful efforts method? a. Financial b. Tax c. Contract d. Managerial e. All of these

-

Discuss why each party to a test-well contribution situation would enter into the transaction.

-

Research and write how the difference between IFRS and GAAP has evolved since the video (The Difference between GAAP and IFRS) was produced in 2018. Identify the main differences and provide an...

-

Juarez worked for Westarz Homes at construction sites for five years. Bever was a superintendent at construction sites, supervising subcontractors and moving trash from sites to landfills. He...

-

Jethro Company, a retailer, had the following account balances as of April 30, 2012: During May, the company completed the following transactions. May 3 Paid one-half of 4/30/12 accounts payable. 4...

-

Muffin, Inc., located in Nauvoo, Illinois, manufactures high-end trumpets. The firms cost accountant, Lisa, has been assigned by the CEO to determine how many trumpets Muffin, Inc., needs to make and...

-

Athletic World is a sporting goods store. The following data are for use in preparing its forecast of cash needs for June: a. Current assets (May 31): Cash . . . . . . . . . . . . . . . . . . . . . ....

-

Given the four criteria necessary for a sale to be complete, which of the following is not one of those conditions? 1. Delivery has occurred or services rendered. 2. Cash has been collected. 3. The...

-

What is the difference between a business and a pure charity? Between a business and a governmental agency?

-

Sketch the \(P-V\) phase diagram for helium-4 using the sketch of the \(P-T\) phase diagram in Figure 4.3. Ps P S superfluid Pe T To T FIGURE 4.3 Sketch of the P-T phase diagram for helium-4. The...

Study smarter with the SolutionInn App