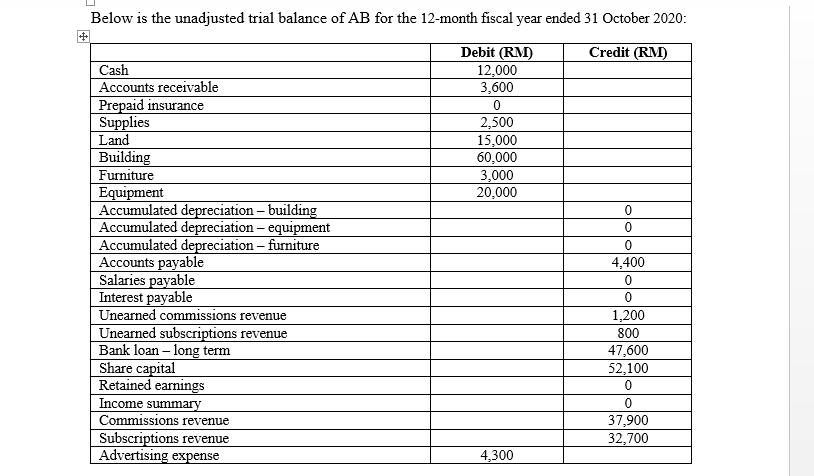

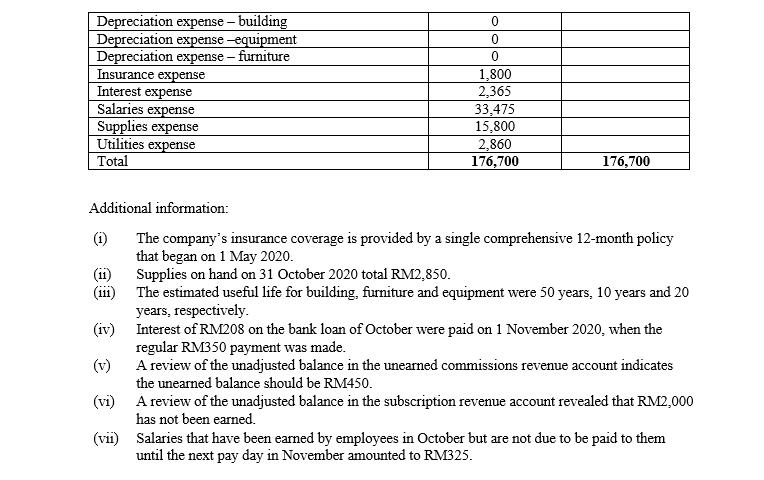

COMPREHENSIVE CASE OF AIRA ASIA BHD Aira Asia Bhd (AAB) is principally engaged in the cultivation...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

COMPREHENSIVE CASE OF AIRA ASIA BHD Aira Asia Bhd (AAB) is principally engaged in the cultivation of oil palm, civil engineering, construction works, and property development. AAB just recently listed on the main board of Bursa Malaysia. As a public listed company, AAB should strictly follow the requirements of presenting the accounting information. The accountant of AAB, Mr. Adhnan should decide on the accounting information that should be presented in its financial statement. For example, should AAB provide information on how much it costs to acquire its assets, or how much the assets are currently worth? Should AAB combine all the activities and show as one segment, or should it report all the activities as a separate segment? Mr Adhnan also in a state of agitation on the requested by one of the executive directors. He asked Mr Adhnan to suppress the information about the lawsuit that has been filed towards the company. His argument was captured as below. "For a newly listed company, this kind of disclosure is damaging to the company and should be hidden. Besides, the chances for AAB to win the case was relatively high". Director X AAB also acquired a new subsidiary, Antanah Bhd (AB). This new subsidiary just operated for one year, and since then, AB outsourced the company's account. Thus, for consolidation purpose, the great challenges for AAB after taking over AB are to scrutinize the accounting method used and to adjust the subsidiary company's year-end to make it similar to AAB's accounting year-end which is on 31 December. However, the account of AB has to be closed first as the company's year-end is approaching, which is on 31 October. Below is the unadjusted trial balance of AB for the 12-month fiscal year ended 31 October 2020: Debit (RM) 12,000 3,600 Credit (RM) Cash Accounts receivable Prepaid insurance Supplies Land 2,500 15,000 60,000 Building Furniture Equipment Accumulated depreciation – building Accumulated depreciation - equipment Accumulated depreciation- furniture Accounts payable Salaries payable Interest payable Unearned commissions revenue Unearned subscriptions revenue Bank loan – long term Share capital Retained earnings Income summary Commissions revenue 3,000 20,000 4,400 1,200 800 47,600 52,100 37,900 32,700 Subscriptions revenue Advertising expense 4,300 Depreciation expense - building Depreciation expense -equipment Depreciation expense - Insurance expense Interest expense Salaries expense Supplies expense Utilities expense Total - furniture 1,800 2,365 33,475 15,800 2,860 176,700 176,700 Additional information: (i) The company's insurance coverage is provided by a single comprehensive 12-month policy that began on 1 May 2020. Supplies on hand on 31 October 2020 total RM2,850. (ii) (iii) The estimated useful life for building, furniture and equipment were 50 years, 10 years and 20 years, respectively. (iv) Interest of RM208 on the bank loan of October were paid on 1 November 2020, when the regular RM350 payment was made. A review of the unadjusted balance in the unearned commissions revenue account indicates the unearned balance should be RM450. (v) (vi) A review of the unadjusted balance in the subscription revenue account revealed that RM2,000 has not been earned. (vii) Salaries that have been eared by employees in October but are not due to be paid to them until the next pay day in November amounted to RM325. QUESTIONS: 1. In the first paragraph, identify the issue that is facing by the accountant of AAB? (СТPS) 2. Based on the issue identified, how does the accountant of AAB could resolve it? (CTPS) 3. For the law suit case facing by AAB, identify which fundamental quality and ingredient of a fundamental quality that was violated if Mr Adhnan follows the director's request? 4. "The lawsuit against the company should be disclosed". Do you agree or disagree? Discuss. (CTPS) 5. How will the prudence concept help to explain the lawsuit issue? 6. Why the accounting year-end of parent and subsidiary companies should be matched? Explain based on any appropriate concept of the qualitative characteristic of accounting information. 7. As a resut of the took over AB by AAB, the responsibility of preparing the accounting information was also taken over by Mr Adhnan department. Thus, he instructed his staff to complete the following task for AB: a. Prepare all necessary adjusting journal entries on 31 October 2020. b. Prepare a statement of profit or loss and other comprehensive income for the year ended 31 October 2020. c. Prepare a statement of financial position as at 31 October 2020. -END OF QUESTIONS- COMPREHENSIVE CASE OF AIRA ASIA BHD Aira Asia Bhd (AAB) is principally engaged in the cultivation of oil palm, civil engineering, construction works, and property development. AAB just recently listed on the main board of Bursa Malaysia. As a public listed company, AAB should strictly follow the requirements of presenting the accounting information. The accountant of AAB, Mr. Adhnan should decide on the accounting information that should be presented in its financial statement. For example, should AAB provide information on how much it costs to acquire its assets, or how much the assets are currently worth? Should AAB combine all the activities and show as one segment, or should it report all the activities as a separate segment? Mr Adhnan also in a state of agitation on the requested by one of the executive directors. He asked Mr Adhnan to suppress the information about the lawsuit that has been filed towards the company. His argument was captured as below. "For a newly listed company, this kind of disclosure is damaging to the company and should be hidden. Besides, the chances for AAB to win the case was relatively high". Director X AAB also acquired a new subsidiary, Antanah Bhd (AB). This new subsidiary just operated for one year, and since then, AB outsourced the company's account. Thus, for consolidation purpose, the great challenges for AAB after taking over AB are to scrutinize the accounting method used and to adjust the subsidiary company's year-end to make it similar to AAB's accounting year-end which is on 31 December. However, the account of AB has to be closed first as the company's year-end is approaching, which is on 31 October. Below is the unadjusted trial balance of AB for the 12-month fiscal year ended 31 October 2020: Debit (RM) 12,000 3,600 Credit (RM) Cash Accounts receivable Prepaid insurance Supplies Land 2,500 15,000 60,000 Building Furniture Equipment Accumulated depreciation – building Accumulated depreciation - equipment Accumulated depreciation- furniture Accounts payable Salaries payable Interest payable Unearned commissions revenue Unearned subscriptions revenue Bank loan – long term Share capital Retained earnings Income summary Commissions revenue 3,000 20,000 4,400 1,200 800 47,600 52,100 37,900 32,700 Subscriptions revenue Advertising expense 4,300 Depreciation expense - building Depreciation expense -equipment Depreciation expense - Insurance expense Interest expense Salaries expense Supplies expense Utilities expense Total - furniture 1,800 2,365 33,475 15,800 2,860 176,700 176,700 Additional information: (i) The company's insurance coverage is provided by a single comprehensive 12-month policy that began on 1 May 2020. Supplies on hand on 31 October 2020 total RM2,850. (ii) (iii) The estimated useful life for building, furniture and equipment were 50 years, 10 years and 20 years, respectively. (iv) Interest of RM208 on the bank loan of October were paid on 1 November 2020, when the regular RM350 payment was made. A review of the unadjusted balance in the unearned commissions revenue account indicates the unearned balance should be RM450. (v) (vi) A review of the unadjusted balance in the subscription revenue account revealed that RM2,000 has not been earned. (vii) Salaries that have been eared by employees in October but are not due to be paid to them until the next pay day in November amounted to RM325. QUESTIONS: 1. In the first paragraph, identify the issue that is facing by the accountant of AAB? (СТPS) 2. Based on the issue identified, how does the accountant of AAB could resolve it? (CTPS) 3. For the law suit case facing by AAB, identify which fundamental quality and ingredient of a fundamental quality that was violated if Mr Adhnan follows the director's request? 4. "The lawsuit against the company should be disclosed". Do you agree or disagree? Discuss. (CTPS) 5. How will the prudence concept help to explain the lawsuit issue? 6. Why the accounting year-end of parent and subsidiary companies should be matched? Explain based on any appropriate concept of the qualitative characteristic of accounting information. 7. As a resut of the took over AB by AAB, the responsibility of preparing the accounting information was also taken over by Mr Adhnan department. Thus, he instructed his staff to complete the following task for AB: a. Prepare all necessary adjusting journal entries on 31 October 2020. b. Prepare a statement of profit or loss and other comprehensive income for the year ended 31 October 2020. c. Prepare a statement of financial position as at 31 October 2020. -END OF QUESTIONS- COMPREHENSIVE CASE OF AIRA ASIA BHD Aira Asia Bhd (AAB) is principally engaged in the cultivation of oil palm, civil engineering, construction works, and property development. AAB just recently listed on the main board of Bursa Malaysia. As a public listed company, AAB should strictly follow the requirements of presenting the accounting information. The accountant of AAB, Mr. Adhnan should decide on the accounting information that should be presented in its financial statement. For example, should AAB provide information on how much it costs to acquire its assets, or how much the assets are currently worth? Should AAB combine all the activities and show as one segment, or should it report all the activities as a separate segment? Mr Adhnan also in a state of agitation on the requested by one of the executive directors. He asked Mr Adhnan to suppress the information about the lawsuit that has been filed towards the company. His argument was captured as below. "For a newly listed company, this kind of disclosure is damaging to the company and should be hidden. Besides, the chances for AAB to win the case was relatively high". Director X AAB also acquired a new subsidiary, Antanah Bhd (AB). This new subsidiary just operated for one year, and since then, AB outsourced the company's account. Thus, for consolidation purpose, the great challenges for AAB after taking over AB are to scrutinize the accounting method used and to adjust the subsidiary company's year-end to make it similar to AAB's accounting year-end which is on 31 December. However, the account of AB has to be closed first as the company's year-end is approaching, which is on 31 October. Below is the unadjusted trial balance of AB for the 12-month fiscal year ended 31 October 2020: Debit (RM) 12,000 3,600 Credit (RM) Cash Accounts receivable Prepaid insurance Supplies Land 2,500 15,000 60,000 Building Furniture Equipment Accumulated depreciation – building Accumulated depreciation - equipment Accumulated depreciation- furniture Accounts payable Salaries payable Interest payable Unearned commissions revenue Unearned subscriptions revenue Bank loan – long term Share capital Retained earnings Income summary Commissions revenue 3,000 20,000 4,400 1,200 800 47,600 52,100 37,900 32,700 Subscriptions revenue Advertising expense 4,300 Depreciation expense - building Depreciation expense -equipment Depreciation expense - Insurance expense Interest expense Salaries expense Supplies expense Utilities expense Total - furniture 1,800 2,365 33,475 15,800 2,860 176,700 176,700 Additional information: (i) The company's insurance coverage is provided by a single comprehensive 12-month policy that began on 1 May 2020. Supplies on hand on 31 October 2020 total RM2,850. (ii) (iii) The estimated useful life for building, furniture and equipment were 50 years, 10 years and 20 years, respectively. (iv) Interest of RM208 on the bank loan of October were paid on 1 November 2020, when the regular RM350 payment was made. A review of the unadjusted balance in the unearned commissions revenue account indicates the unearned balance should be RM450. (v) (vi) A review of the unadjusted balance in the subscription revenue account revealed that RM2,000 has not been earned. (vii) Salaries that have been eared by employees in October but are not due to be paid to them until the next pay day in November amounted to RM325. QUESTIONS: 1. In the first paragraph, identify the issue that is facing by the accountant of AAB? (СТPS) 2. Based on the issue identified, how does the accountant of AAB could resolve it? (CTPS) 3. For the law suit case facing by AAB, identify which fundamental quality and ingredient of a fundamental quality that was violated if Mr Adhnan follows the director's request? 4. "The lawsuit against the company should be disclosed". Do you agree or disagree? Discuss. (CTPS) 5. How will the prudence concept help to explain the lawsuit issue? 6. Why the accounting year-end of parent and subsidiary companies should be matched? Explain based on any appropriate concept of the qualitative characteristic of accounting information. 7. As a resut of the took over AB by AAB, the responsibility of preparing the accounting information was also taken over by Mr Adhnan department. Thus, he instructed his staff to complete the following task for AB: a. Prepare all necessary adjusting journal entries on 31 October 2020. b. Prepare a statement of profit or loss and other comprehensive income for the year ended 31 October 2020. c. Prepare a statement of financial position as at 31 October 2020. -END OF QUESTIONS- COMPREHENSIVE CASE OF AIRA ASIA BHD Aira Asia Bhd (AAB) is principally engaged in the cultivation of oil palm, civil engineering, construction works, and property development. AAB just recently listed on the main board of Bursa Malaysia. As a public listed company, AAB should strictly follow the requirements of presenting the accounting information. The accountant of AAB, Mr. Adhnan should decide on the accounting information that should be presented in its financial statement. For example, should AAB provide information on how much it costs to acquire its assets, or how much the assets are currently worth? Should AAB combine all the activities and show as one segment, or should it report all the activities as a separate segment? Mr Adhnan also in a state of agitation on the requested by one of the executive directors. He asked Mr Adhnan to suppress the information about the lawsuit that has been filed towards the company. His argument was captured as below. "For a newly listed company, this kind of disclosure is damaging to the company and should be hidden. Besides, the chances for AAB to win the case was relatively high". Director X AAB also acquired a new subsidiary, Antanah Bhd (AB). This new subsidiary just operated for one year, and since then, AB outsourced the company's account. Thus, for consolidation purpose, the great challenges for AAB after taking over AB are to scrutinize the accounting method used and to adjust the subsidiary company's year-end to make it similar to AAB's accounting year-end which is on 31 December. However, the account of AB has to be closed first as the company's year-end is approaching, which is on 31 October. Below is the unadjusted trial balance of AB for the 12-month fiscal year ended 31 October 2020: Debit (RM) 12,000 3,600 Credit (RM) Cash Accounts receivable Prepaid insurance Supplies Land 2,500 15,000 60,000 Building Furniture Equipment Accumulated depreciation – building Accumulated depreciation - equipment Accumulated depreciation- furniture Accounts payable Salaries payable Interest payable Unearned commissions revenue Unearned subscriptions revenue Bank loan – long term Share capital Retained earnings Income summary Commissions revenue 3,000 20,000 4,400 1,200 800 47,600 52,100 37,900 32,700 Subscriptions revenue Advertising expense 4,300 Depreciation expense - building Depreciation expense -equipment Depreciation expense - Insurance expense Interest expense Salaries expense Supplies expense Utilities expense Total - furniture 1,800 2,365 33,475 15,800 2,860 176,700 176,700 Additional information: (i) The company's insurance coverage is provided by a single comprehensive 12-month policy that began on 1 May 2020. Supplies on hand on 31 October 2020 total RM2,850. (ii) (iii) The estimated useful life for building, furniture and equipment were 50 years, 10 years and 20 years, respectively. (iv) Interest of RM208 on the bank loan of October were paid on 1 November 2020, when the regular RM350 payment was made. A review of the unadjusted balance in the unearned commissions revenue account indicates the unearned balance should be RM450. (v) (vi) A review of the unadjusted balance in the subscription revenue account revealed that RM2,000 has not been earned. (vii) Salaries that have been eared by employees in October but are not due to be paid to them until the next pay day in November amounted to RM325. QUESTIONS: 1. In the first paragraph, identify the issue that is facing by the accountant of AAB? (СТPS) 2. Based on the issue identified, how does the accountant of AAB could resolve it? (CTPS) 3. For the law suit case facing by AAB, identify which fundamental quality and ingredient of a fundamental quality that was violated if Mr Adhnan follows the director's request? 4. "The lawsuit against the company should be disclosed". Do you agree or disagree? Discuss. (CTPS) 5. How will the prudence concept help to explain the lawsuit issue? 6. Why the accounting year-end of parent and subsidiary companies should be matched? Explain based on any appropriate concept of the qualitative characteristic of accounting information. 7. As a resut of the took over AB by AAB, the responsibility of preparing the accounting information was also taken over by Mr Adhnan department. Thus, he instructed his staff to complete the following task for AB: a. Prepare all necessary adjusting journal entries on 31 October 2020. b. Prepare a statement of profit or loss and other comprehensive income for the year ended 31 October 2020. c. Prepare a statement of financial position as at 31 October 2020. -END OF QUESTIONS- COMPREHENSIVE CASE OF AIRA ASIA BHD Aira Asia Bhd (AAB) is principally engaged in the cultivation of oil palm, civil engineering, construction works, and property development. AAB just recently listed on the main board of Bursa Malaysia. As a public listed company, AAB should strictly follow the requirements of presenting the accounting information. The accountant of AAB, Mr. Adhnan should decide on the accounting information that should be presented in its financial statement. For example, should AAB provide information on how much it costs to acquire its assets, or how much the assets are currently worth? Should AAB combine all the activities and show as one segment, or should it report all the activities as a separate segment? Mr Adhnan also in a state of agitation on the requested by one of the executive directors. He asked Mr Adhnan to suppress the information about the lawsuit that has been filed towards the company. His argument was captured as below. "For a newly listed company, this kind of disclosure is damaging to the company and should be hidden. Besides, the chances for AAB to win the case was relatively high". Director X AAB also acquired a new subsidiary, Antanah Bhd (AB). This new subsidiary just operated for one year, and since then, AB outsourced the company's account. Thus, for consolidation purpose, the great challenges for AAB after taking over AB are to scrutinize the accounting method used and to adjust the subsidiary company's year-end to make it similar to AAB's accounting year-end which is on 31 December. However, the account of AB has to be closed first as the company's year-end is approaching, which is on 31 October. Below is the unadjusted trial balance of AB for the 12-month fiscal year ended 31 October 2020: Debit (RM) 12,000 3,600 Credit (RM) Cash Accounts receivable Prepaid insurance Supplies Land 2,500 15,000 60,000 Building Furniture Equipment Accumulated depreciation – building Accumulated depreciation - equipment Accumulated depreciation- furniture Accounts payable Salaries payable Interest payable Unearned commissions revenue Unearned subscriptions revenue Bank loan – long term Share capital Retained earnings Income summary Commissions revenue 3,000 20,000 4,400 1,200 800 47,600 52,100 37,900 32,700 Subscriptions revenue Advertising expense 4,300 Depreciation expense - building Depreciation expense -equipment Depreciation expense - Insurance expense Interest expense Salaries expense Supplies expense Utilities expense Total - furniture 1,800 2,365 33,475 15,800 2,860 176,700 176,700 Additional information: (i) The company's insurance coverage is provided by a single comprehensive 12-month policy that began on 1 May 2020. Supplies on hand on 31 October 2020 total RM2,850. (ii) (iii) The estimated useful life for building, furniture and equipment were 50 years, 10 years and 20 years, respectively. (iv) Interest of RM208 on the bank loan of October were paid on 1 November 2020, when the regular RM350 payment was made. A review of the unadjusted balance in the unearned commissions revenue account indicates the unearned balance should be RM450. (v) (vi) A review of the unadjusted balance in the subscription revenue account revealed that RM2,000 has not been earned. (vii) Salaries that have been eared by employees in October but are not due to be paid to them until the next pay day in November amounted to RM325. QUESTIONS: 1. In the first paragraph, identify the issue that is facing by the accountant of AAB? (СТPS) 2. Based on the issue identified, how does the accountant of AAB could resolve it? (CTPS) 3. For the law suit case facing by AAB, identify which fundamental quality and ingredient of a fundamental quality that was violated if Mr Adhnan follows the director's request? 4. "The lawsuit against the company should be disclosed". Do you agree or disagree? Discuss. (CTPS) 5. How will the prudence concept help to explain the lawsuit issue? 6. Why the accounting year-end of parent and subsidiary companies should be matched? Explain based on any appropriate concept of the qualitative characteristic of accounting information. 7. As a resut of the took over AB by AAB, the responsibility of preparing the accounting information was also taken over by Mr Adhnan department. Thus, he instructed his staff to complete the following task for AB: a. Prepare all necessary adjusting journal entries on 31 October 2020. b. Prepare a statement of profit or loss and other comprehensive income for the year ended 31 October 2020. c. Prepare a statement of financial position as at 31 October 2020. -END OF QUESTIONS- COMPREHENSIVE CASE OF AIRA ASIA BHD Aira Asia Bhd (AAB) is principally engaged in the cultivation of oil palm, civil engineering, construction works, and property development. AAB just recently listed on the main board of Bursa Malaysia. As a public listed company, AAB should strictly follow the requirements of presenting the accounting information. The accountant of AAB, Mr. Adhnan should decide on the accounting information that should be presented in its financial statement. For example, should AAB provide information on how much it costs to acquire its assets, or how much the assets are currently worth? Should AAB combine all the activities and show as one segment, or should it report all the activities as a separate segment? Mr Adhnan also in a state of agitation on the requested by one of the executive directors. He asked Mr Adhnan to suppress the information about the lawsuit that has been filed towards the company. His argument was captured as below. "For a newly listed company, this kind of disclosure is damaging to the company and should be hidden. Besides, the chances for AAB to win the case was relatively high". Director X AAB also acquired a new subsidiary, Antanah Bhd (AB). This new subsidiary just operated for one year, and since then, AB outsourced the company's account. Thus, for consolidation purpose, the great challenges for AAB after taking over AB are to scrutinize the accounting method used and to adjust the subsidiary company's year-end to make it similar to AAB's accounting year-end which is on 31 December. However, the account of AB has to be closed first as the company's year-end is approaching, which is on 31 October. Below is the unadjusted trial balance of AB for the 12-month fiscal year ended 31 October 2020: Debit (RM) 12,000 3,600 Credit (RM) Cash Accounts receivable Prepaid insurance Supplies Land 2,500 15,000 60,000 Building Furniture Equipment Accumulated depreciation – building Accumulated depreciation - equipment Accumulated depreciation- furniture Accounts payable Salaries payable Interest payable Unearned commissions revenue Unearned subscriptions revenue Bank loan – long term Share capital Retained earnings Income summary Commissions revenue 3,000 20,000 4,400 1,200 800 47,600 52,100 37,900 32,700 Subscriptions revenue Advertising expense 4,300 Depreciation expense - building Depreciation expense -equipment Depreciation expense - Insurance expense Interest expense Salaries expense Supplies expense Utilities expense Total - furniture 1,800 2,365 33,475 15,800 2,860 176,700 176,700 Additional information: (i) The company's insurance coverage is provided by a single comprehensive 12-month policy that began on 1 May 2020. Supplies on hand on 31 October 2020 total RM2,850. (ii) (iii) The estimated useful life for building, furniture and equipment were 50 years, 10 years and 20 years, respectively. (iv) Interest of RM208 on the bank loan of October were paid on 1 November 2020, when the regular RM350 payment was made. A review of the unadjusted balance in the unearned commissions revenue account indicates the unearned balance should be RM450. (v) (vi) A review of the unadjusted balance in the subscription revenue account revealed that RM2,000 has not been earned. (vii) Salaries that have been eared by employees in October but are not due to be paid to them until the next pay day in November amounted to RM325. QUESTIONS: 1. In the first paragraph, identify the issue that is facing by the accountant of AAB? (СТPS) 2. Based on the issue identified, how does the accountant of AAB could resolve it? (CTPS) 3. For the law suit case facing by AAB, identify which fundamental quality and ingredient of a fundamental quality that was violated if Mr Adhnan follows the director's request? 4. "The lawsuit against the company should be disclosed". Do you agree or disagree? Discuss. (CTPS) 5. How will the prudence concept help to explain the lawsuit issue? 6. Why the accounting year-end of parent and subsidiary companies should be matched? Explain based on any appropriate concept of the qualitative characteristic of accounting information. 7. As a resut of the took over AB by AAB, the responsibility of preparing the accounting information was also taken over by Mr Adhnan department. Thus, he instructed his staff to complete the following task for AB: a. Prepare all necessary adjusting journal entries on 31 October 2020. b. Prepare a statement of profit or loss and other comprehensive income for the year ended 31 October 2020. c. Prepare a statement of financial position as at 31 October 2020. -END OF QUESTIONS- COMPREHENSIVE CASE OF AIRA ASIA BHD Aira Asia Bhd (AAB) is principally engaged in the cultivation of oil palm, civil engineering, construction works, and property development. AAB just recently listed on the main board of Bursa Malaysia. As a public listed company, AAB should strictly follow the requirements of presenting the accounting information. The accountant of AAB, Mr. Adhnan should decide on the accounting information that should be presented in its financial statement. For example, should AAB provide information on how much it costs to acquire its assets, or how much the assets are currently worth? Should AAB combine all the activities and show as one segment, or should it report all the activities as a separate segment? Mr Adhnan also in a state of agitation on the requested by one of the executive directors. He asked Mr Adhnan to suppress the information about the lawsuit that has been filed towards the company. His argument was captured as below. "For a newly listed company, this kind of disclosure is damaging to the company and should be hidden. Besides, the chances for AAB to win the case was relatively high". Director X AAB also acquired a new subsidiary, Antanah Bhd (AB). This new subsidiary just operated for one year, and since then, AB outsourced the company's account. Thus, for consolidation purpose, the great challenges for AAB after taking over AB are to scrutinize the accounting method used and to adjust the subsidiary company's year-end to make it similar to AAB's accounting year-end which is on 31 December. However, the account of AB has to be closed first as the company's year-end is approaching, which is on 31 October. Below is the unadjusted trial balance of AB for the 12-month fiscal year ended 31 October 2020: Debit (RM) 12,000 3,600 Credit (RM) Cash Accounts receivable Prepaid insurance Supplies Land 2,500 15,000 60,000 Building Furniture Equipment Accumulated depreciation – building Accumulated depreciation - equipment Accumulated depreciation- furniture Accounts payable Salaries payable Interest payable Unearned commissions revenue Unearned subscriptions revenue Bank loan – long term Share capital Retained earnings Income summary Commissions revenue 3,000 20,000 4,400 1,200 800 47,600 52,100 37,900 32,700 Subscriptions revenue Advertising expense 4,300 Depreciation expense - building Depreciation expense -equipment Depreciation expense - Insurance expense Interest expense Salaries expense Supplies expense Utilities expense Total - furniture 1,800 2,365 33,475 15,800 2,860 176,700 176,700 Additional information: (i) The company's insurance coverage is provided by a single comprehensive 12-month policy that began on 1 May 2020. Supplies on hand on 31 October 2020 total RM2,850. (ii) (iii) The estimated useful life for building, furniture and equipment were 50 years, 10 years and 20 years, respectively. (iv) Interest of RM208 on the bank loan of October were paid on 1 November 2020, when the regular RM350 payment was made. A review of the unadjusted balance in the unearned commissions revenue account indicates the unearned balance should be RM450. (v) (vi) A review of the unadjusted balance in the subscription revenue account revealed that RM2,000 has not been earned. (vii) Salaries that have been eared by employees in October but are not due to be paid to them until the next pay day in November amounted to RM325. QUESTIONS: 1. In the first paragraph, identify the issue that is facing by the accountant of AAB? (СТPS) 2. Based on the issue identified, how does the accountant of AAB could resolve it? (CTPS) 3. For the law suit case facing by AAB, identify which fundamental quality and ingredient of a fundamental quality that was violated if Mr Adhnan follows the director's request? 4. "The lawsuit against the company should be disclosed". Do you agree or disagree? Discuss. (CTPS) 5. How will the prudence concept help to explain the lawsuit issue? 6. Why the accounting year-end of parent and subsidiary companies should be matched? Explain based on any appropriate concept of the qualitative characteristic of accounting information. 7. As a resut of the took over AB by AAB, the responsibility of preparing the accounting information was also taken over by Mr Adhnan department. Thus, he instructed his staff to complete the following task for AB: a. Prepare all necessary adjusting journal entries on 31 October 2020. b. Prepare a statement of profit or loss and other comprehensive income for the year ended 31 October 2020. c. Prepare a statement of financial position as at 31 October 2020. -END OF QUESTIONS- COMPREHENSIVE CASE OF AIRA ASIA BHD Aira Asia Bhd (AAB) is principally engaged in the cultivation of oil palm, civil engineering, construction works, and property development. AAB just recently listed on the main board of Bursa Malaysia. As a public listed company, AAB should strictly follow the requirements of presenting the accounting information. The accountant of AAB, Mr. Adhnan should decide on the accounting information that should be presented in its financial statement. For example, should AAB provide information on how much it costs to acquire its assets, or how much the assets are currently worth? Should AAB combine all the activities and show as one segment, or should it report all the activities as a separate segment? Mr Adhnan also in a state of agitation on the requested by one of the executive directors. He asked Mr Adhnan to suppress the information about the lawsuit that has been filed towards the company. His argument was captured as below. "For a newly listed company, this kind of disclosure is damaging to the company and should be hidden. Besides, the chances for AAB to win the case was relatively high". Director X AAB also acquired a new subsidiary, Antanah Bhd (AB). This new subsidiary just operated for one year, and since then, AB outsourced the company's account. Thus, for consolidation purpose, the great challenges for AAB after taking over AB are to scrutinize the accounting method used and to adjust the subsidiary company's year-end to make it similar to AAB's accounting year-end which is on 31 December. However, the account of AB has to be closed first as the company's year-end is approaching, which is on 31 October. Below is the unadjusted trial balance of AB for the 12-month fiscal year ended 31 October 2020: Debit (RM) 12,000 3,600 Credit (RM) Cash Accounts receivable Prepaid insurance Supplies Land 2,500 15,000 60,000 Building Furniture Equipment Accumulated depreciation – building Accumulated depreciation - equipment Accumulated depreciation- furniture Accounts payable Salaries payable Interest payable Unearned commissions revenue Unearned subscriptions revenue Bank loan – long term Share capital Retained earnings Income summary Commissions revenue 3,000 20,000 4,400 1,200 800 47,600 52,100 37,900 32,700 Subscriptions revenue Advertising expense 4,300 Depreciation expense - building Depreciation expense -equipment Depreciation expense - Insurance expense Interest expense Salaries expense Supplies expense Utilities expense Total - furniture 1,800 2,365 33,475 15,800 2,860 176,700 176,700 Additional information: (i) The company's insurance coverage is provided by a single comprehensive 12-month policy that began on 1 May 2020. Supplies on hand on 31 October 2020 total RM2,850. (ii) (iii) The estimated useful life for building, furniture and equipment were 50 years, 10 years and 20 years, respectively. (iv) Interest of RM208 on the bank loan of October were paid on 1 November 2020, when the regular RM350 payment was made. A review of the unadjusted balance in the unearned commissions revenue account indicates the unearned balance should be RM450. (v) (vi) A review of the unadjusted balance in the subscription revenue account revealed that RM2,000 has not been earned. (vii) Salaries that have been eared by employees in October but are not due to be paid to them until the next pay day in November amounted to RM325. QUESTIONS: 1. In the first paragraph, identify the issue that is facing by the accountant of AAB? (СТPS) 2. Based on the issue identified, how does the accountant of AAB could resolve it? (CTPS) 3. For the law suit case facing by AAB, identify which fundamental quality and ingredient of a fundamental quality that was violated if Mr Adhnan follows the director's request? 4. "The lawsuit against the company should be disclosed". Do you agree or disagree? Discuss. (CTPS) 5. How will the prudence concept help to explain the lawsuit issue? 6. Why the accounting year-end of parent and subsidiary companies should be matched? Explain based on any appropriate concept of the qualitative characteristic of accounting information. 7. As a resut of the took over AB by AAB, the responsibility of preparing the accounting information was also taken over by Mr Adhnan department. Thus, he instructed his staff to complete the following task for AB: a. Prepare all necessary adjusting journal entries on 31 October 2020. b. Prepare a statement of profit or loss and other comprehensive income for the year ended 31 October 2020. c. Prepare a statement of financial position as at 31 October 2020. -END OF QUESTIONS-

Expert Answer:

Answer rating: 100% (QA)

1 In the first paragraph identify the issue that is facing by the accountant of AAB The accountant i... View the full answer

Related Book For

Fundamental Accounting Principles

ISBN: 978-0078110870

20th Edition

Authors: John J. Wild, Ken W. Shaw, Barbara Chiappetta

Posted Date:

Students also viewed these accounting questions

-

Galaxy Productions fiscal year ended 31 December 2019. Their net profit was $2,796, the firms equity (new capital) was reduced from $50,000 to $32,796. The was also selling merchandises as part of...

-

Sky High Building Services has seen a growth in business in recent months and, based on the advice of the Accountant, has created a small proprietary company in order to run the building services...

-

Insurance coverage expires on October 31 2017 2 Depreciation expense for the month was 3750 3 Gift cards with remaining balances of 2300 expired on August 31 2017 4 A physical count showed 23000 on...

-

Kellogg Company is expected to pay $2.00 in annual dividends to its common shareholders in the future. Our best estimate of the expected cost of equity capital is 5.0% and the expected growth rate in...

-

What is validity?

-

(a) Is there a choice of rotation axes for a bowling ball and a baseball, each rotating on its own axis, such that the baseball has a greater rotational inertia? If so, describe the axes. If not,...

-

With reference to the previous exercise, construct a 98% confidence interval for the true population mean number of unremovable defects per display. Data From Previous Exercise 7.5 The manufacture of...

-

The following variances existed at year-end 2010 for Muckstadt Production Company: Material price variance ............$23,400 U Material quantity variance .......... 24,900 F Labor rate variance...

-

Discuss the principles of process intensification (PI) and its role in achieving sustainable and efficient chemical processing, focusing on the reduction of equipment size, energy consumption, and...

-

you are a corporate trainer for XYZ organization. You have just been tasked with developing and deploying a training program for new customer service representatives discussing how to reply to...

-

You have recently been appointed as management accountant to Beacon Ltd. The company manufactures three types of laptops. The company currently absorbs overheads on the basis of machine hours. The...

-

A professional is obligated to a. keep abreast of changes in their field. b. follow up on a clients condition or status. c. make referrals when appropriate. d. all of the above.

-

To whom do medical records belong? When do defendants have a right to these records?

-

True Or False Legal assistants are often responsible for helping to make sure that filing dates are met.

-

True Or False Comparative negligence can be used to reduce a plaintiffs recovery if the defendant is reckless or willful and wanton.

-

What is the difference between contributory negligence, comparative negligence, and assumption of risk?

-

Write the pre-order, post-order, and in-order travel sequence for the binary tree given below: (No explanation needed). M F C G R J P X I N FIG. 1

-

The first law of thermodynamics is sometimes whimsically stated as, You cant get something for nothing, and the second law as, You cant even break even. Explain how these statements could be...

-

The Carrefour Group reports the following description of its trading securities (titled financial assets reported at fair value in the income statement). These are financial assets held by the Group...

-

Does the balance in the Accumulated DepreciationMachinery account represent funds to replace the machinery when it wears out? If not, what does it represent?

-

Key information from Nokia (www.Nokia.com), which is a leading global manufacturer of mobile devices and services, follows. 1. Compute the accounts receivable turnover for the current year. 2. How...

-

What is the pressure drop associated with water at \(27^{\circ} \mathrm{C}\) flowing with a mean velocity of \(0.1 \mathrm{~m} / \mathrm{s}\) through an \(800-\mathrm{m}-\) long cast iron pipe of...

-

Fully developed conditions are known to exist for water flowing through a \(50-\mathrm{mm}\)-diameter tube at \(0.02 \mathrm{~kg} / \mathrm{s}\) and \(27^{\circ} \mathrm{C}\). What is the maximum...

-

Water at \(35^{\circ} \mathrm{C}\) is pumped through a horizontal, \(200-\mathrm{m}\)-long, \(30-\mathrm{mm}\)-diameter tube at \(0.25 \mathrm{~kg} / \mathrm{s}\). Over time, a 2-mm-thick layer of...

Study smarter with the SolutionInn App