Question: The following data is observed from the bond market. All coupon-paying bonds pay coupons semi-annually, and other bonds in the market use the semi-annual convention.

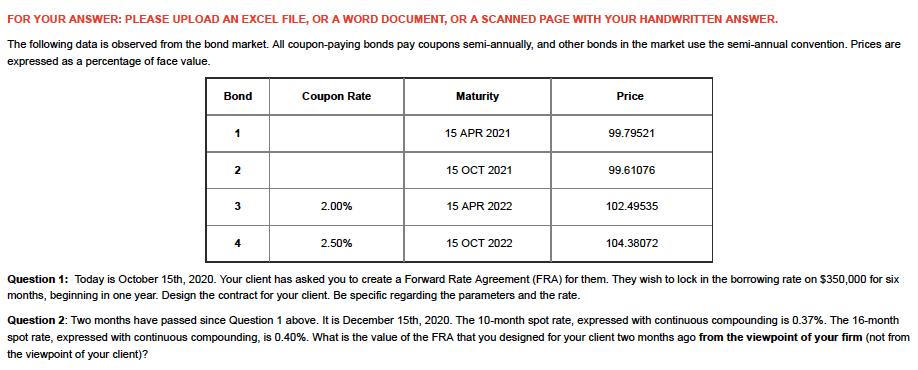

The following data is observed from the bond market. All coupon-paying bonds pay coupons semi-annually, and other bonds in the market use the semi-annual convention. Prices are expressed as a percentage of face value.

Question 1: Today is October 15th, 2020. Your client has asked you to create a Forward Rate Agreement (FRA) for them. They wish to lock in the borrowing rate on $350,000 for six months, beginning in one year. Design the contract for your client. Be specific regarding the parameters and the rate.

Question 2: Two months have passed since Question 1 above. It is December 15th, 2020. The 10-month spot rate, expressed with continuous compounding is 0.37%. The 16-month spot rate, expressed with continuous compounding, is 0.40%. What is the value of the FRA that you designed for your client two months ago from the viewpoint of your firm (not from the viewpoint of your client)?

FOR YOUR ANSWER: PLEASE UPLOAD AN EXCEL FILE, OR A WORD DOCUMENT, OR A SCANNED PAGE WITH YOUR HANDWRITTEN ANSWER. The following data is observed from the bond market. All coupon-paying bonds pay coupons semi-annually, and other bonds in the market use the semi-annual convention. Prices are expressed as a percentage of face value. Bond 1 2 3 Coupon Rate 2.00% 2.50% Maturity 15 APR 2021 15 OCT 2021 15 APR 2022 15 OCT 2022 Price 99.79521 99.61076 102.49535 104.38072 Question 1: Today is October 15th, 2020. Your client has asked you to create a Forward Rate Agreement (FRA) for them. They wish to lock in the borrowing rate on $350,000 for six months, beginning in one year. Design the contract for your client. Be specific regarding the parameters and the rate. Question 2: Two months have passed since Question 1 above. It is December 15th, 2020. The 10-month spot rate, expressed with continuous compounding is 0.37%. The 16-month spot rate, expressed with continuous compounding, is 0.40%. What is the value of the FRA that you designed for your client two months ago from the viewpoint of your firm (not from the viewpoint of your client)?

Step by Step Solution

3.32 Rating (161 Votes )

There are 3 Steps involved in it

Question 1 Today is October 15th 2020 Your client has asked you to create a Forward Rate Agreement FRA for them They wish to lock in the borrowing rate on 350000 for six months beginning in one year D... View full answer

Get step-by-step solutions from verified subject matter experts