Question: Accounting Problem (Simple) Instructions Refer to Background to Complete Question 5 Part 1.png and Question 5 Part 2.png, use the list of Accounts Below. List

Accounting Problem (Simple)

Instructions

Refer to Background to Complete Question 5 Part 1.png and Question 5 Part 2.png, use the list of Accounts Below.

List of Accounts

- Accumulated Depletion

- Accumulated Depreciation - Vehicles

- Accumulated Depreciation - Buildings

- Accumulated Depreciation - Equipment

- Accumulated Depreciation - Furniture

- Accumulated Depreciation - Machinery

- Accumulated Depreciation - Vehicles

- Accumulated Impairment Losses - Building

- Accumulated Impairment Losses - Equipment

- Accumulated Impairment Losses - Land

- Accumulated Impairment Losses - Machinery

- Accumulated Impairment Losses - Mine

- Accumulated Impairment Losses - Patents

- Accumulated Impairment Losses - Vehicles

- Asset Retirement Obligation

- Buildings

- Cash

- Common Shares

- Contribution Expense

- Cost of Goods Sold

- Deferred Revenue - Government Grants

- Depreciation Expense

- Equipment

- Exploration Expense

- Furniture

- Gain on Disposal of Vehicles

- Gain on Disposal of Building

- Gain on Disposal of Equipment

- Gain on Disposal of Furniture

- Gain on Disposal of Machinery

- Gain on Disposal of Vehicle

- Gain on Disposal of Land

- Interest Expense

- Interest Payable

- Inventory

- Investment Property

- Land

- Loss on Disposal of Vehicles

- Loss on Disposal of Building

- Loss on Disposal of Equipment

- Loss on Disposal of Machinery

- Loss on Disposal of Land

- Loss on Disposal of Vehicles

- Loss on Expropriation

- Loss on Impairment

- Machinery

- Mineral Resources

- No Entry

- Notes Payable

- Oil Property

- Recovery of Loss from Impairment

- Repairs and Maintenance Expense

- Retained Earnings

- Revaluation Surplus (OCI)

- Revenue - Government Grants

- Royalty Expense

- Vehicles

Background

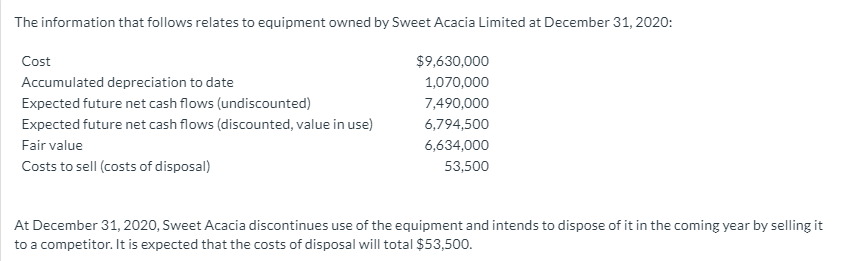

The information that follows relates to equipment owned by Sweet Acacia Limited at December 31, 2020: Cost $9,630,000 Accumulated depreciation to date 1,070,000 Expected future net cash flows (undiscounted) 7,490,000 Expected future net cash flows (discounted, value in use) 6,794,500 Fair value 6,634,000 Costs to sell (costs of disposal) 53,500 At December 31, 2020, Sweet Acacia discontinues use of the equipment and intends to dispose of it in the coming year by selling it to a competitor. It is expected that the costs of disposal will total $53,500.Assume that Sweet Acacia is a private company that follows ASPE. (Credit account titles are automatically indented when the amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account titles and enter 0 for the amounts.) 1. Prepare the journal entry at December 31, 2020, to record asset impairment, if any. 2. Prepare the journal entry to record depreciation expense for 2021. 3. Assume that the asset was not sold by December 31, 2021. The equipment's fair value (and recoverable amount) on this date is $6.96 million. Prepare the journal entry, if any, to record the increase in fair value. It is expected that the costs of disposal will total $53,500. No. Account Titles and Explanation Debit Credit (1) (2) (3)Repeat the requirements in (a) above assuming that Sweet Acacia is a public company that follows IFRS, and that the asset meets all criteria for classification as an asset held for sale. (Credit account titles are automatically indented when the amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account titles and enter 0 for the amounts.) Account Titles and Explanation Debit Credit (1) (2) (3)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts