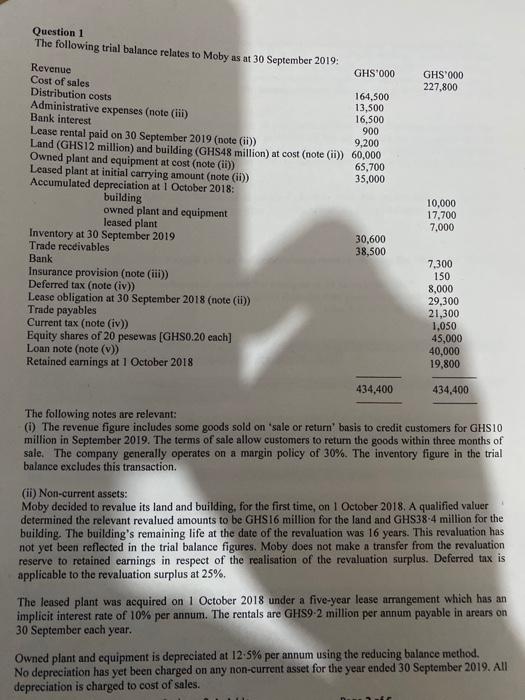

Question 1 The following trial balance relates to Moby as at 30 September 2019: Revenue Cost...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

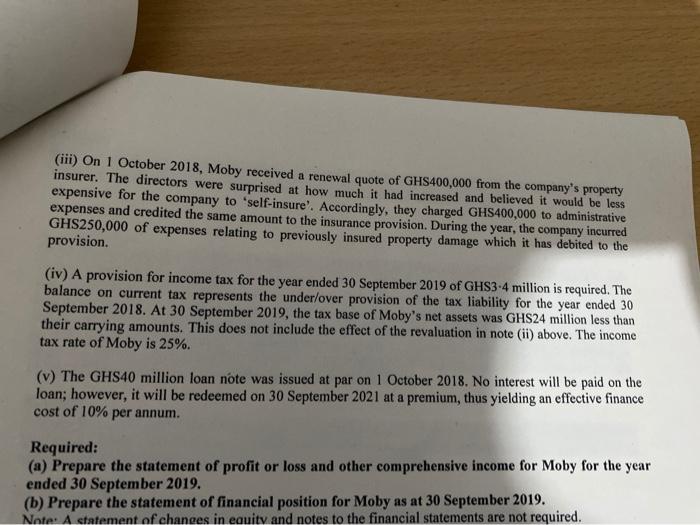

Question 1 The following trial balance relates to Moby as at 30 September 2019: Revenue Cost of sales Distribution costs GHS'000 GHS'000 227,800 Administrative expenses (note (ii) Bank interest Lease rental paid on 30 September 2019 (note (ii)) Land (GHS12 million) and building (GHS48 million) at cost (note (ii)) 60,000 Owned plant and equipment at cost (note (ii)) Leased plant at initial carrying amount (note (ii) Accumulated depreciation at I October 2018: 164,500 13,500 16,500 900 9,200 65,700 35,000 building owned plant and equipment leased plant 10,000 17,700 7,000 Inventory at 30 September 2019 Trade receivables Bank 30,600 38,500 7,300 150 Insurance provision (note (iii) Deferred tax (note (iv)) Lease obligation at 30 September 2018 (note (i) Trade payables Current tax (note (iv)) Equity shares of 20 pesewas [GHS0.20 each) Loan note (note (v)) Retained earnings at 1 October 2018 8,000 29,300 21,300 1,050 45,000 40,000 19,800 434,400 434,400 The following notes are relevant: (i) The revenue figure includes some goods sold on 'sale or return' basis to credit customers for GHS10 million in September 2019. The terms of sale allow customers to retum the goods within three months of sale. The company generally operates on a margin policy of 30%. The inventory figure in the trial balance excludes this transaction. (ii) Non-current assets: Moby decided to revalue its land and building, for the first time, on 1 October 2018. A qualified valuer determined the relevant revalued amounts to be GHS16 million for the land and GHS38-4 million for the building. The building's remaining life at the date of the revaluation was 16 years. This revaluation has not yet been reflected in the trial balance figures, Moby does not make a transfer from the revaluation reserve to retained earnings in respect of the realisation of the revaluation surplus. Deferred tax is applicable to the revaluation surplus at 25%. The leased plant was acquired on 1 October 2018 under a five-year lease arrangement which has an implicit interest rate of 10% per annum. The rentals are GHS9-2 million per annum payable in arears on 30 September each year. Owned plant and equipment is depreciated at 12-5% per annum using the reducing balance method. No depreciation has yet been charged on any non-current asset for the year ended 30 September 2019. All depreciation is charged to cost of sales. (iii) On 1 October 2018, Moby received a renewal quote of GHS400,000 from the company's property insurer. The directors were surprised at how much it had increased and believed it would be less expensive for the company to "self-insure'. Accordingly, they charged GHS400,000 to administrative expenses and credited the same amount to the insurance provision. During the year, the company incurred GHS250,000 of expenses relating to previously insured property damage which it has debited to the provision. (iv) A provision for income tax for the year ended 30 September 2019 of GHS3-4 million is required. The balance on current tax represents the under/over provision of the tax liability for the year ended 30 September 2018. At 30 September 2019, the tax base of Moby's net assets was GHS24 million less than their carrying amounts. This does not include the effect of the revaluation in note (ii) above. The income tax rate of Moby is 25%. (v) The GHS40 million loan note was issued at par on 1 October 2018. No interest will be paid on the loan; however, it will be redeemed on 30 September 2021 at a premium, thus yielding an effective finance cost of 10% per annum. Required: (a) Prepare the statement of profit or loss and other comprehensive income for Moby for the year ended 30 September 2019. (b) Prepare the statement of financial position for Moby as at 30 September 2019. Note: A statement of changes in eauity and notes to the financial statements are not required. Question 1 The following trial balance relates to Moby as at 30 September 2019: Revenue Cost of sales Distribution costs GHS'000 GHS'000 227,800 Administrative expenses (note (ii) Bank interest Lease rental paid on 30 September 2019 (note (ii)) Land (GHS12 million) and building (GHS48 million) at cost (note (ii)) 60,000 Owned plant and equipment at cost (note (ii)) Leased plant at initial carrying amount (note (ii) Accumulated depreciation at I October 2018: 164,500 13,500 16,500 900 9,200 65,700 35,000 building owned plant and equipment leased plant 10,000 17,700 7,000 Inventory at 30 September 2019 Trade receivables Bank 30,600 38,500 7,300 150 Insurance provision (note (iii) Deferred tax (note (iv)) Lease obligation at 30 September 2018 (note (i) Trade payables Current tax (note (iv)) Equity shares of 20 pesewas [GHS0.20 each) Loan note (note (v)) Retained earnings at 1 October 2018 8,000 29,300 21,300 1,050 45,000 40,000 19,800 434,400 434,400 The following notes are relevant: (i) The revenue figure includes some goods sold on 'sale or return' basis to credit customers for GHS10 million in September 2019. The terms of sale allow customers to retum the goods within three months of sale. The company generally operates on a margin policy of 30%. The inventory figure in the trial balance excludes this transaction. (ii) Non-current assets: Moby decided to revalue its land and building, for the first time, on 1 October 2018. A qualified valuer determined the relevant revalued amounts to be GHS16 million for the land and GHS38-4 million for the building. The building's remaining life at the date of the revaluation was 16 years. This revaluation has not yet been reflected in the trial balance figures, Moby does not make a transfer from the revaluation reserve to retained earnings in respect of the realisation of the revaluation surplus. Deferred tax is applicable to the revaluation surplus at 25%. The leased plant was acquired on 1 October 2018 under a five-year lease arrangement which has an implicit interest rate of 10% per annum. The rentals are GHS9-2 million per annum payable in arears on 30 September each year. Owned plant and equipment is depreciated at 12-5% per annum using the reducing balance method. No depreciation has yet been charged on any non-current asset for the year ended 30 September 2019. All depreciation is charged to cost of sales. (iii) On 1 October 2018, Moby received a renewal quote of GHS400,000 from the company's property insurer. The directors were surprised at how much it had increased and believed it would be less expensive for the company to "self-insure'. Accordingly, they charged GHS400,000 to administrative expenses and credited the same amount to the insurance provision. During the year, the company incurred GHS250,000 of expenses relating to previously insured property damage which it has debited to the provision. (iv) A provision for income tax for the year ended 30 September 2019 of GHS3-4 million is required. The balance on current tax represents the under/over provision of the tax liability for the year ended 30 September 2018. At 30 September 2019, the tax base of Moby's net assets was GHS24 million less than their carrying amounts. This does not include the effect of the revaluation in note (ii) above. The income tax rate of Moby is 25%. (v) The GHS40 million loan note was issued at par on 1 October 2018. No interest will be paid on the loan; however, it will be redeemed on 30 September 2021 at a premium, thus yielding an effective finance cost of 10% per annum. Required: (a) Prepare the statement of profit or loss and other comprehensive income for Moby for the year ended 30 September 2019. (b) Prepare the statement of financial position for Moby as at 30 September 2019. Note: A statement of changes in eauity and notes to the financial statements are not required.

Expert Answer:

Answer rating: 100% (QA)

G 1 2 a 3 Moby Statement of profit or loss for the year ended 30 September 2019 4 GHS000 6 Revenue 7 ... View the full answer

Related Book For

Financial Accounting and Reporting

ISBN: 978-1292162409

18th edition

Authors: Barry Elliott, Jamie Elliott

Posted Date:

Students also viewed these accounting questions

-

An ice block of mass 5.0 kg slides down a rough surface of a ramp with at an angle = 48 while an ice worker pulls on the block by a rope with a force F = 45 N and is directed up the ramp. The...

-

The following trial balance relates to Faith at 30 September 2008: GHS000 GHS000 Leasehold property at valuation 1 October 2007 (note (i)) 50,000 Plant and equipment at cost (note (i)) 76,600 Plant...

-

The following trial balance relates to Amethyst as at 31 March 2015: The following information is relevant: 1. After the year end stock take it was discovered that goods worth $4 million, which were...

-

Use Gordon formula to calculate the price of the stock. ITC company expected to pay dividend of $4 and growth rate of 3% per year is constant forever. Required return is 8%.

-

The theoretical limit for extracting solute S from phase 1 (volume V 1 ) into phase 2 (volume V 2 ) is attained by dividing V 2 into an infinite number of infinitesimally small portions and...

-

The alarm at a fire station rings and an 86-kg fireman, starting from rest, slides down a pole to the floor below (a distance of 4.0 m). Just before landing, his speed is 1.4 m/s. What is the...

-

If the probability is 0.90 that a new machine will produce 40 or more chairs, find the probabilities that among 16 such machines (a) 12 will produce 40 or more chairs; (b) at least 10 will produce 40...

-

A radioactive material produces 1280 decays per minute at one time, and 4.6h later produces 320 decays per minute. What is its half-life?

-

Let's suppose you (USA dealer) imported 10 BMW (7 series) from a German dealer on March 1, 2018 at 60,000 each, payable in 30 days. The exchange rate on March 1, 2018 was 1.15 US$/. Then you sold...

-

Rio Ferinand, the owner of Ferdinand Gold Mining, is evaluating a new gold mine in Fort McMurray. Paul Pogba, the company's geologist, has just finished his analysis of the mine site. He has...

-

C++ program to simulate a game of Blackjack between two to four players. Your program must incorporate a two-dimensional array to represent the suit and the value of each card dealt to a player, keep...

-

Radom Manufacturing produces various products. The company operates a landfill, which it uses to dispose of nonhazardous trash. The trash is hauled from the two nearby manufacturing facilities in...

-

The Greenville Cruisers, a professional roller derby team, prepares financial statements on a monthly basis. The roller derby season begins in February, but in January, the team engaged in the...

-

3-42. CVP, SENSITIVITY ANALYSIS. Jan's Ornaments sells handmade ornaments for $35.00 per ornament. Operating information for 2020 is as follows: Sales revenue ($35 per ornament) Variable cost ($20...

-

Cullumber Company self-insures its property for fire and storm damage. If the company were to obtain insurance on the property, it would cost them $1920000 per year. The company estimates that, on...

-

For profitable companies, accountants provide two versions of Earning per Share (EPS) 'Basic' and 'Diluted'. Why is 'Diluted EPS only computed for profitable companies? Briefly, how is 'Basic' EPS...

-

Using FIRAC then consider this problem: You have taken a few of Instructors classes and have learned about jurisdiction. You work part-time for a lawyer in Costa Mesa, CA. The lawyer tells you that a...

-

1. Use these cost, revenue, and probability estimates along with the decision tree to identify the best decision strategy for Trendy's Pies. 2. Suppose that Trendy is concerned about her probability...

-

James Bright has just taken up the position of managing director following the unsatisfactory achievements of the previous incumbent. James arrives as the accounts for the previous year are being...

-

Geoworld Enterprises plc has the following information extracted from its statement of income and payroll systems:...

-

FRS 105 requires that a complete set of financial statements of a micro-entity should include the following: (a) A statement of financial position as at the reporting date with notes included at the...

-

Trans Clothing Alterations began operations on 1 August 2024 and completed the following transactions during the first month. 1. Tran deposited \($18\) 000 of her personal funds in a current account...

-

Finesse Fitness was established on 1 April 2024 with an initial investment of $60000 by the owner, Daniel Hewitt. During the first few months of business, the owner employed a student studying...

-

Jason Vu offers tutoring services to first-year university students. He has set up a sole proprietorship business named JV Tutoring. Jason has collected the following information relating to his...

Study smarter with the SolutionInn App