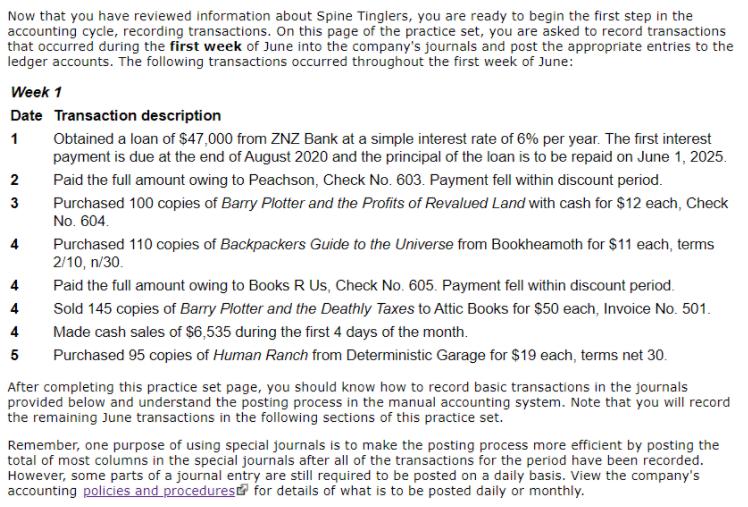

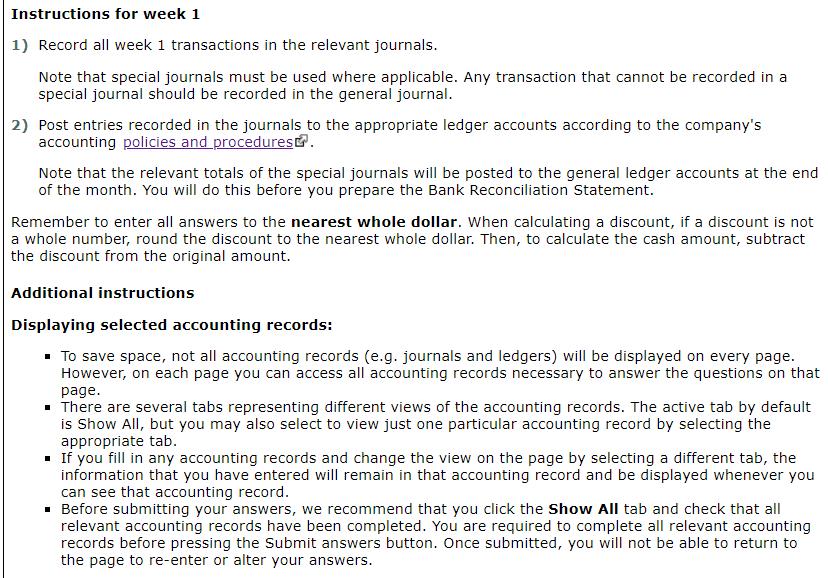

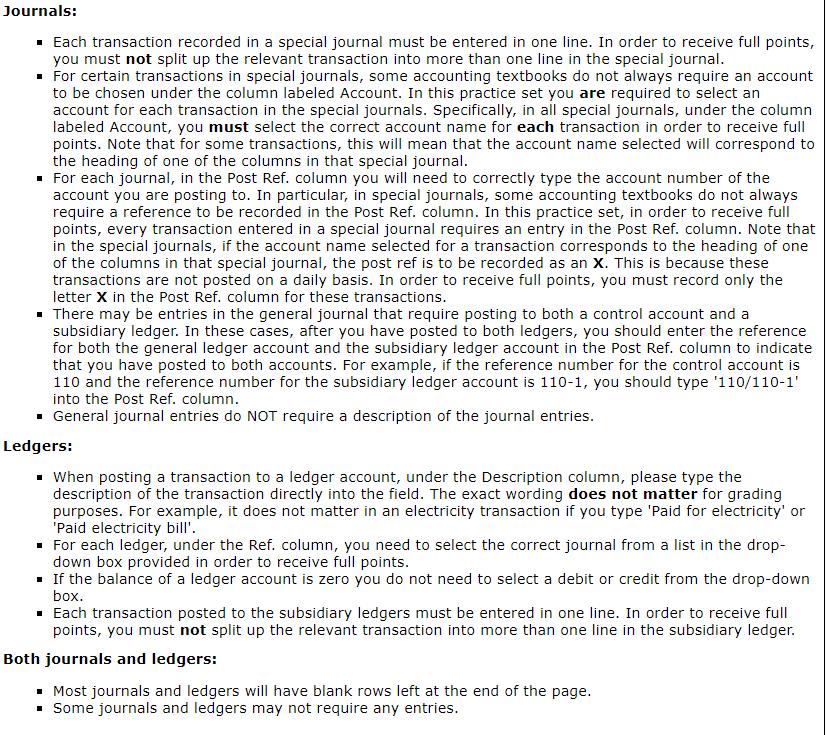

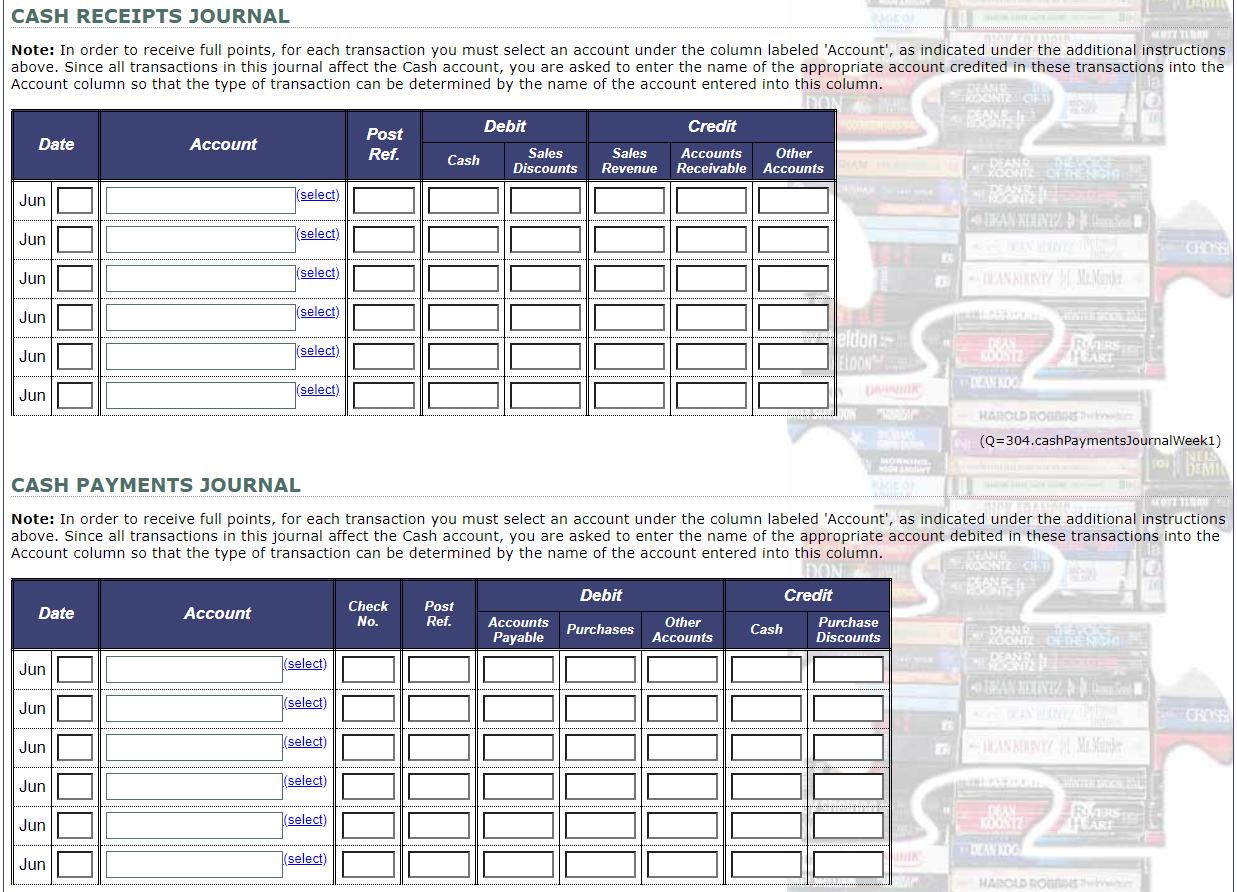

Now that you have reviewed information about Spine Tinglers, you are ready to begin the first...

Fantastic news! We've Found the answer you've been seeking!

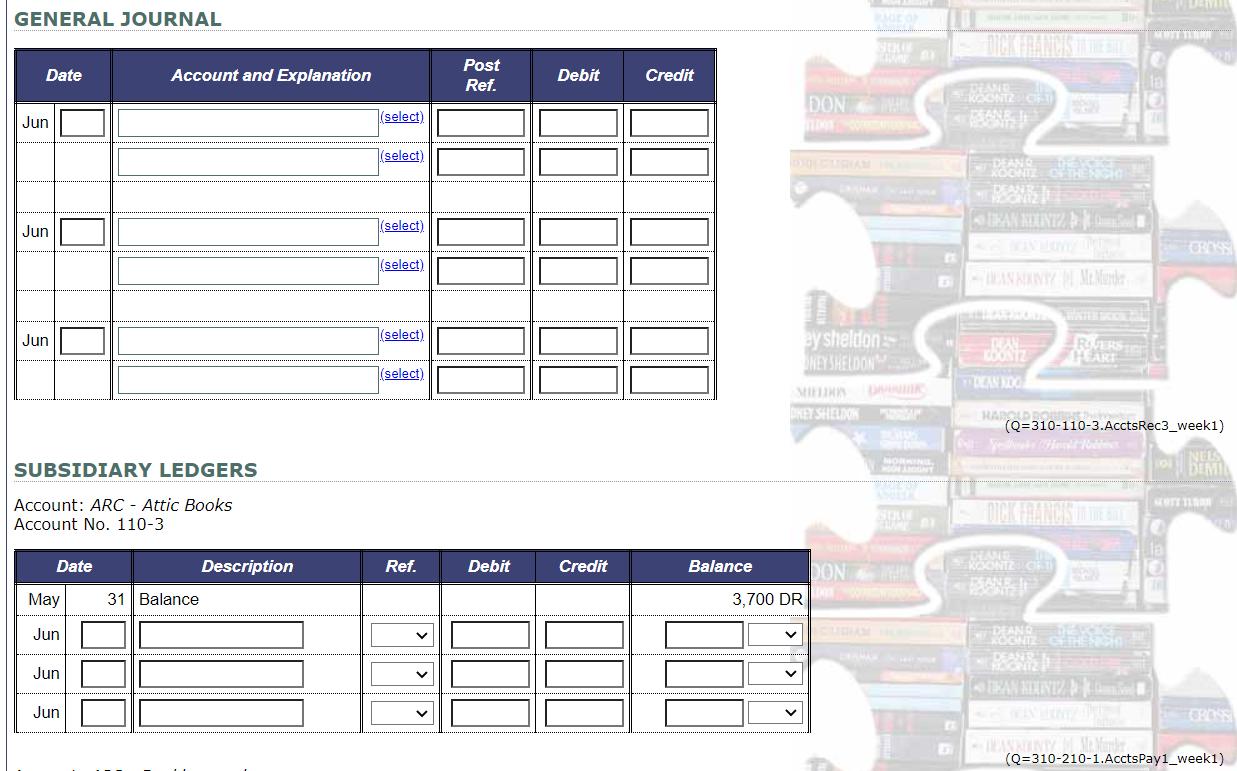

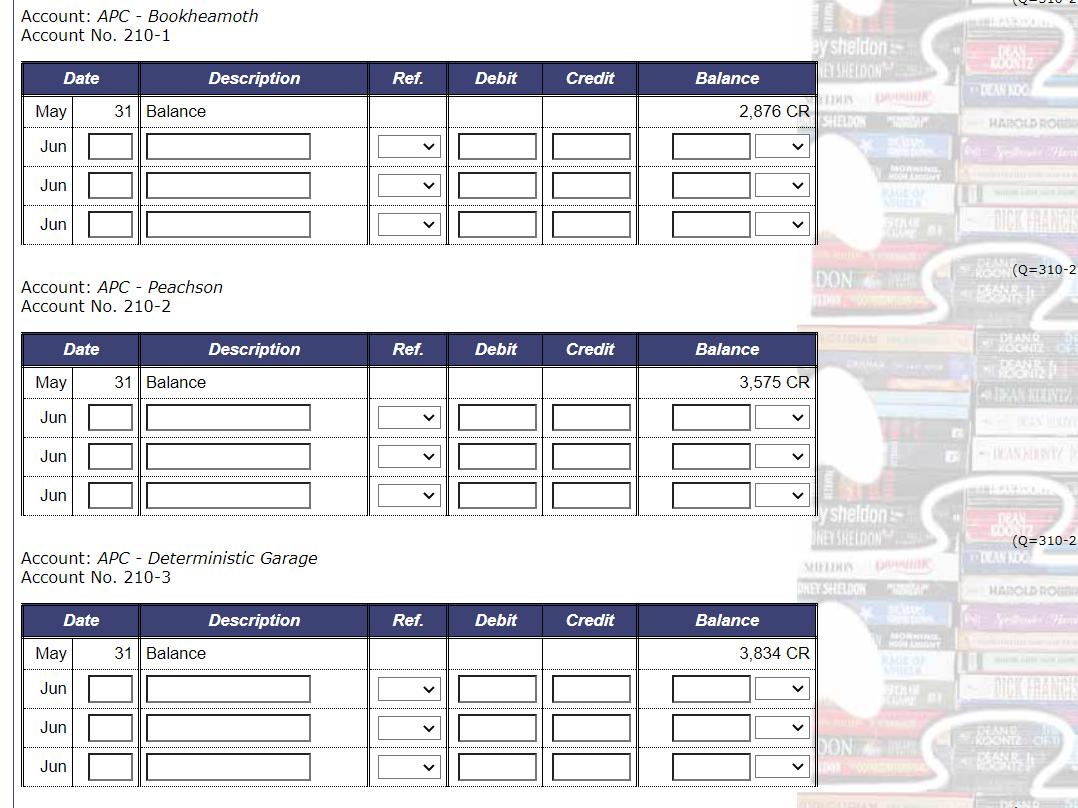

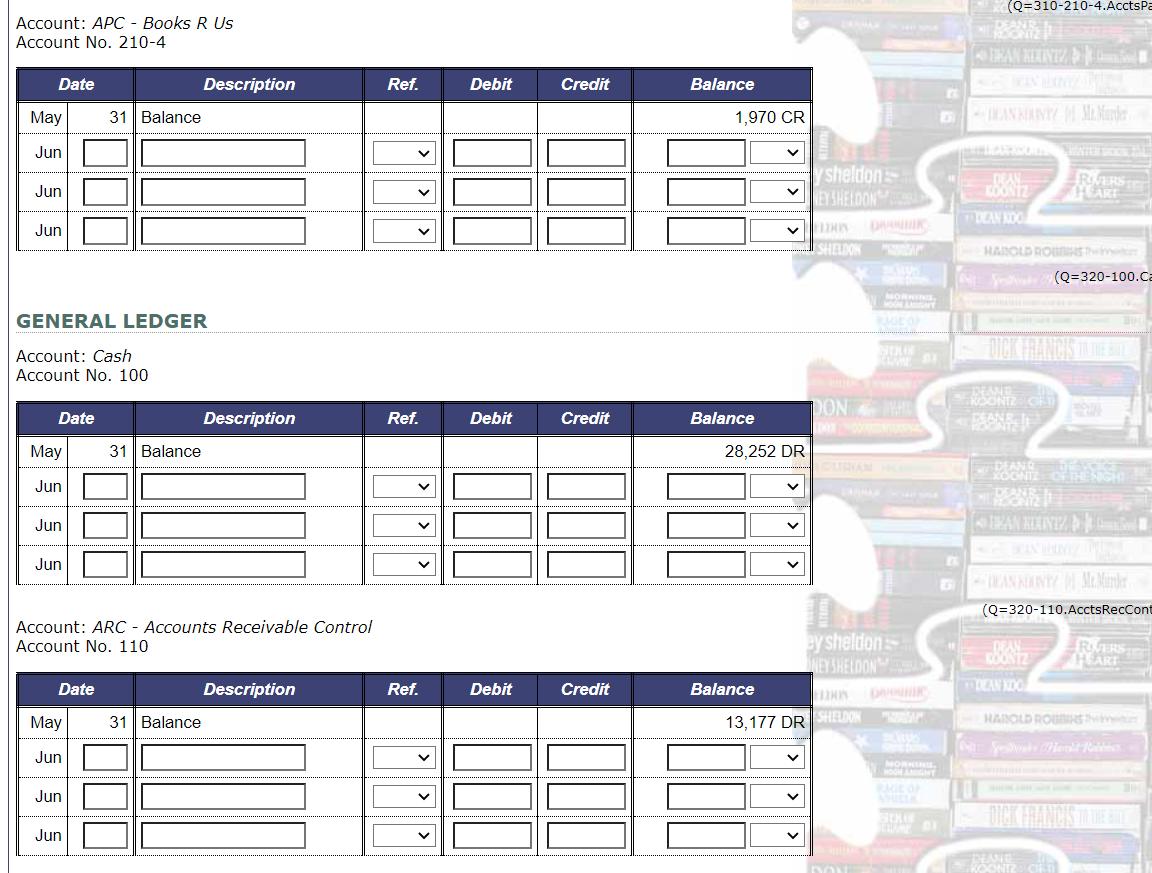

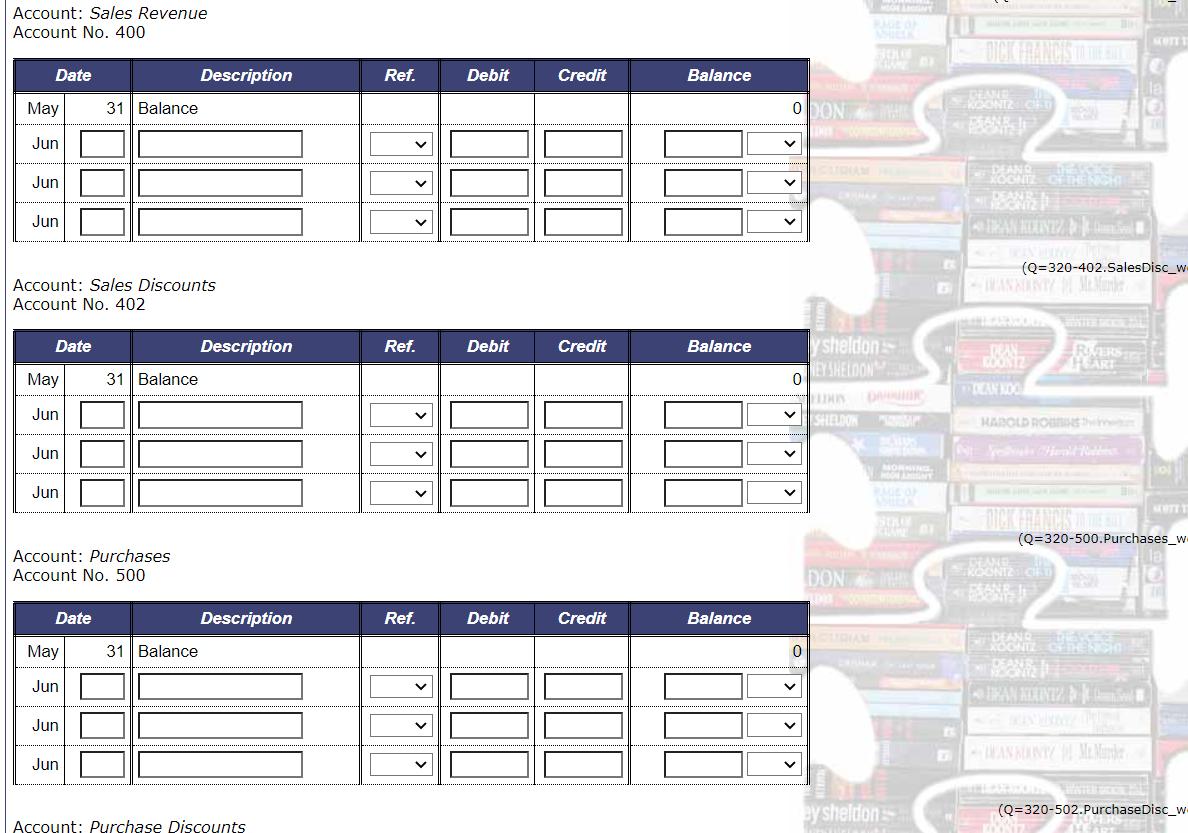

Question:

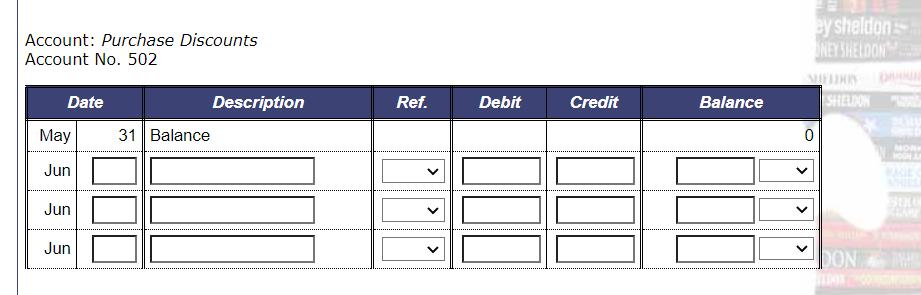

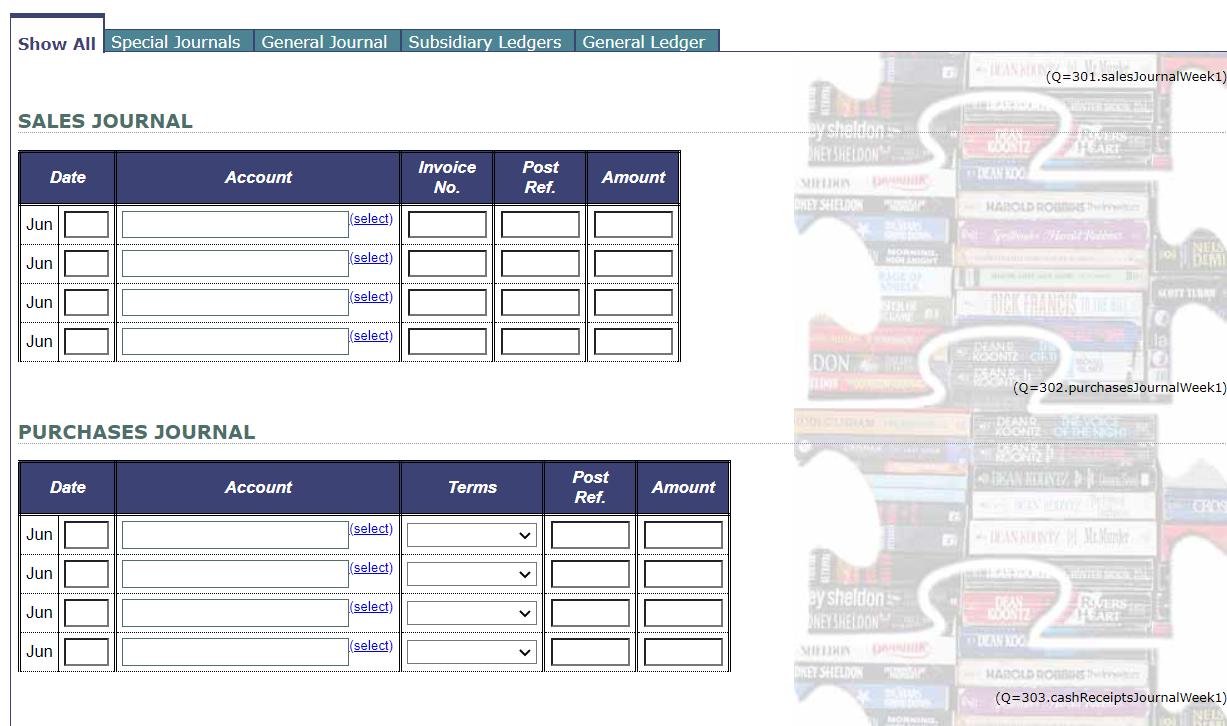

Transcribed Image Text: