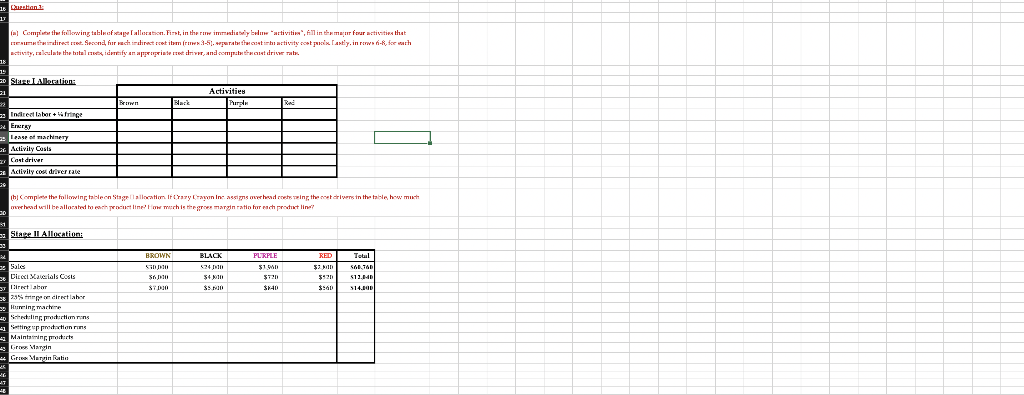

Question: Additional info 1 Castan Completa fallowing tables are allocation. First, in the row immediately below artiviti, All in the main fear activities that BEdictreet. Second,

Additional info

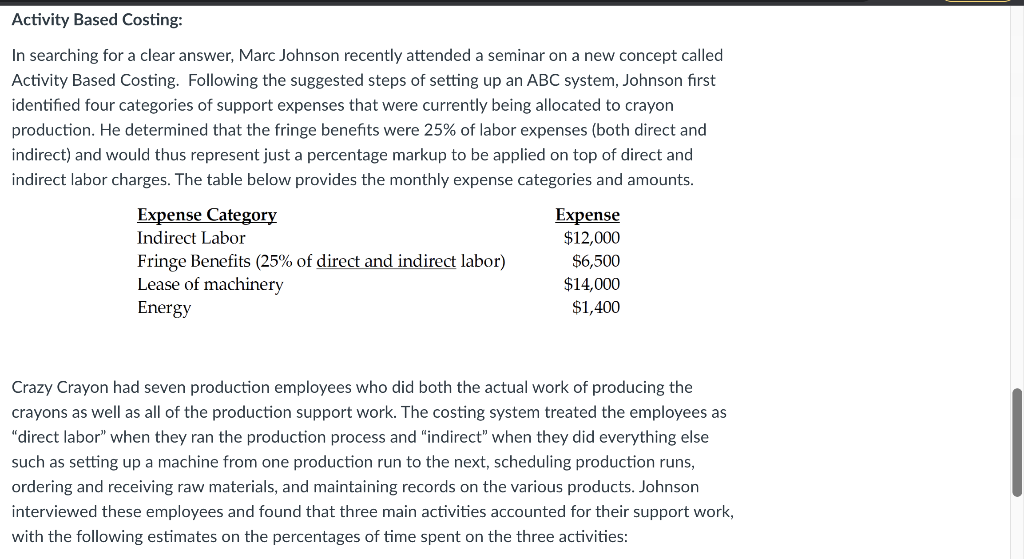

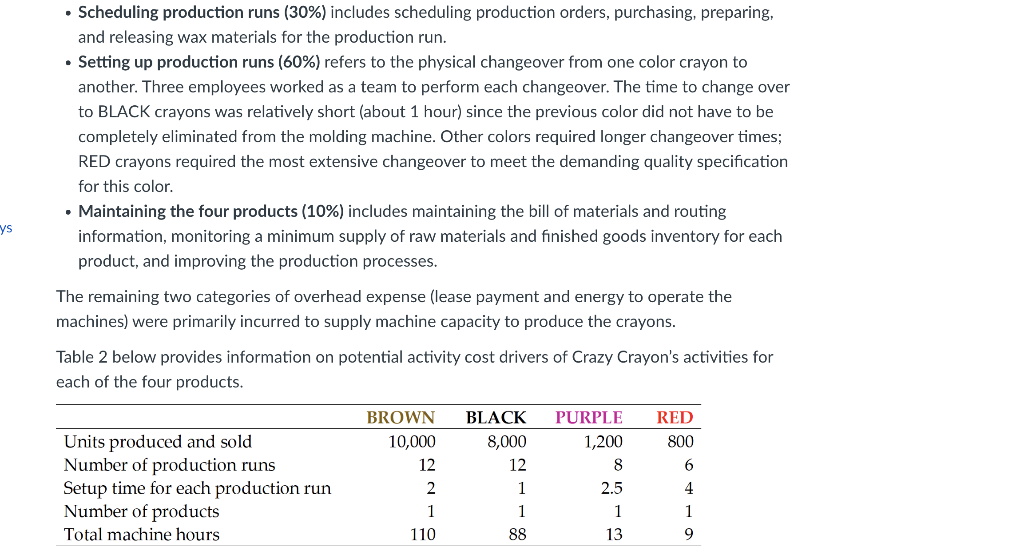

1 Castan Completa fallowing tables are allocation. First, in the row immediately below artiviti", All in the main fear activities that BEdictreet. Second, forvach direct rretim (2.3-5.rabeceractivity coix Castly, in two-R, feath activity, a clate the belles identify an appropriate red driver and completo drive at 18 50 SL Allocation Activities Purple Brown Back Red 3 Indirect labore Errey Lased machinery Activity Costa Cost driver - Activity Codrera thi Complete following tableon Stage allocation. If Chary ragyon Incassins hardrobe eing, the set drivers in the table, how much hd will be allocated to chewch is the gro margination for each product line? 30 33 Stage II Allocation BROWN BLACK Total Sales PLIRPLE 31 3721 $140 RED $3 MIN $42 $540 Diccc Macials Cosis 311111 SALTAR $12.HR 514.000 34 11 $ rector STA 28 direct lahor 3 Hurrin warme 40 Sect:ling practition in 1 Settings pretion Maintain points * Le Margin .. Gre Marin Ratin Activity Based Costing: In searching for a clear answer, Marc Johnson recently attended a seminar on a new concept called Activity Based Costing. Following the suggested steps of setting up an ABC system, Johnson first identified four categories of support expenses that were currently being allocated to crayon production. He determined that the fringe benefits were 25% of labor expenses (both direct and indirect) and would thus represent just a percentage markup to be applied on top of direct and indirect labor charges. The table below provides the monthly expense categories and amounts. Expense Category Expense Indirect Labor $12,000 Fringe Benefits (25% of direct and indirect labor) $6,500 Lease of machinery $14,000 Energy $1,400 Crazy Crayon had seven production employees who did both the actual work of producing the crayons as well as all of the production support work. The costing system treated the employees as "direct labor" when they ran the production process and indirect" when they did everything else such as setting up a machine from one production run to the next, scheduling production runs, ordering and receiving raw materials, and maintaining records on the various products. Johnson interviewed these employees and found that three main activities accounted for their support work, with the following estimates on the percentages of time spent on the three activities: Scheduling production runs (30%) includes scheduling production orders, purchasing, preparing, and releasing wax materials for the production run. Setting up production runs (60%) refers to the physical changeover from one color crayon to another. Three employees worked as a team to perform each changeover. The time to change over to BLACK crayons was relatively short (about 1 hour) since the previous color did not have to be completely eliminated from the molding machine. Other colors required longer changeover times; RED crayons required the most extensive changeover to meet the demanding quality specification for this color Maintaining the four products (10%) includes maintaining the bill of materials and routing information, monitoring a minimum supply of raw materials and finished goods inventory for each product, and improving the production processes. The remaining two categories of overhead expense (lease payment and energy to operate the machines) were primarily incurred to supply machine capacity to produce the crayons. ys Table 2 below provides information on potential activity cost drivers of Crazy Crayon's activities for each of the four products. BLACK 8,000 12 RED 800 Units produced and sold Number of production runs Setup time for each production run Number of products Total machine hours 6 BROWN 10,000 12 2 1 110 PURPLE 1,200 8 2.5 4 1 1 88 1 13 1 9 1 Castan Completa fallowing tables are allocation. First, in the row immediately below artiviti", All in the main fear activities that BEdictreet. Second, forvach direct rretim (2.3-5.rabeceractivity coix Castly, in two-R, feath activity, a clate the belles identify an appropriate red driver and completo drive at 18 50 SL Allocation Activities Purple Brown Back Red 3 Indirect labore Errey Lased machinery Activity Costa Cost driver - Activity Codrera thi Complete following tableon Stage allocation. If Chary ragyon Incassins hardrobe eing, the set drivers in the table, how much hd will be allocated to chewch is the gro margination for each product line? 30 33 Stage II Allocation BROWN BLACK Total Sales PLIRPLE 31 3721 $140 RED $3 MIN $42 $540 Diccc Macials Cosis 311111 SALTAR $12.HR 514.000 34 11 $ rector STA 28 direct lahor 3 Hurrin warme 40 Sect:ling practition in 1 Settings pretion Maintain points * Le Margin .. Gre Marin Ratin Activity Based Costing: In searching for a clear answer, Marc Johnson recently attended a seminar on a new concept called Activity Based Costing. Following the suggested steps of setting up an ABC system, Johnson first identified four categories of support expenses that were currently being allocated to crayon production. He determined that the fringe benefits were 25% of labor expenses (both direct and indirect) and would thus represent just a percentage markup to be applied on top of direct and indirect labor charges. The table below provides the monthly expense categories and amounts. Expense Category Expense Indirect Labor $12,000 Fringe Benefits (25% of direct and indirect labor) $6,500 Lease of machinery $14,000 Energy $1,400 Crazy Crayon had seven production employees who did both the actual work of producing the crayons as well as all of the production support work. The costing system treated the employees as "direct labor" when they ran the production process and indirect" when they did everything else such as setting up a machine from one production run to the next, scheduling production runs, ordering and receiving raw materials, and maintaining records on the various products. Johnson interviewed these employees and found that three main activities accounted for their support work, with the following estimates on the percentages of time spent on the three activities: Scheduling production runs (30%) includes scheduling production orders, purchasing, preparing, and releasing wax materials for the production run. Setting up production runs (60%) refers to the physical changeover from one color crayon to another. Three employees worked as a team to perform each changeover. The time to change over to BLACK crayons was relatively short (about 1 hour) since the previous color did not have to be completely eliminated from the molding machine. Other colors required longer changeover times; RED crayons required the most extensive changeover to meet the demanding quality specification for this color Maintaining the four products (10%) includes maintaining the bill of materials and routing information, monitoring a minimum supply of raw materials and finished goods inventory for each product, and improving the production processes. The remaining two categories of overhead expense (lease payment and energy to operate the machines) were primarily incurred to supply machine capacity to produce the crayons. ys Table 2 below provides information on potential activity cost drivers of Crazy Crayon's activities for each of the four products. BLACK 8,000 12 RED 800 Units produced and sold Number of production runs Setup time for each production run Number of products Total machine hours 6 BROWN 10,000 12 2 1 110 PURPLE 1,200 8 2.5 4 1 1 88 1 13 1 9

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts