Question: Additional information for the unresolved financial reporting issues in Exhibit 3 Advance information - Issue 1 Revaluation of Land Included in the balance for PPE

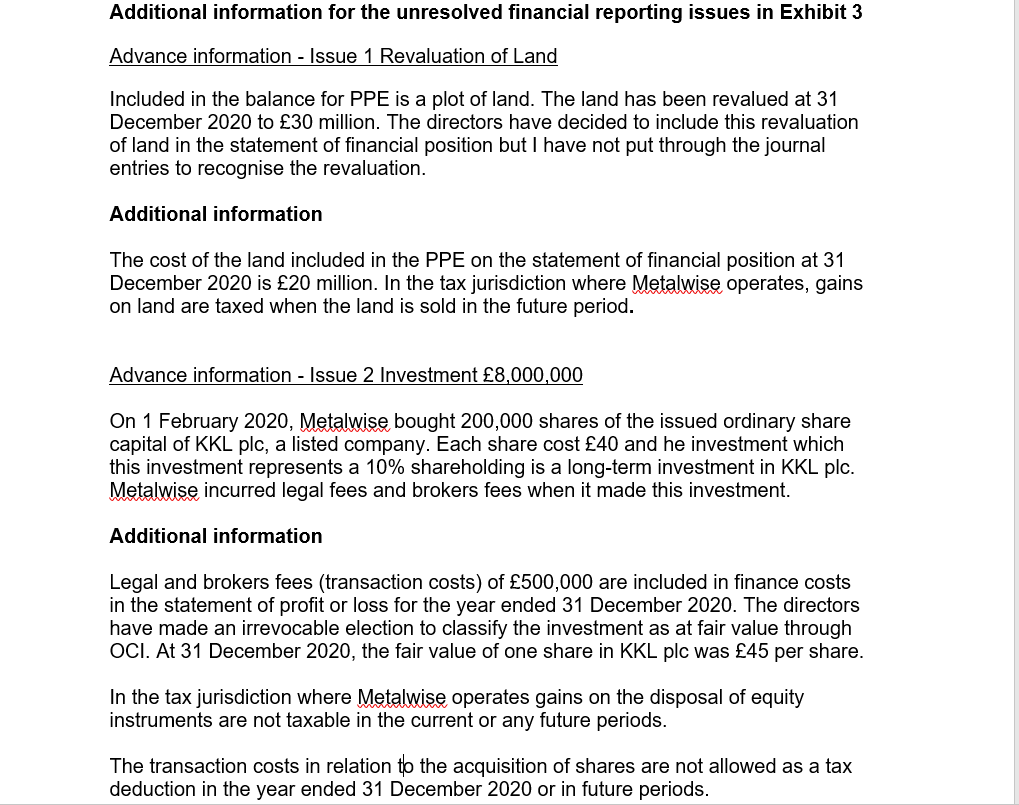

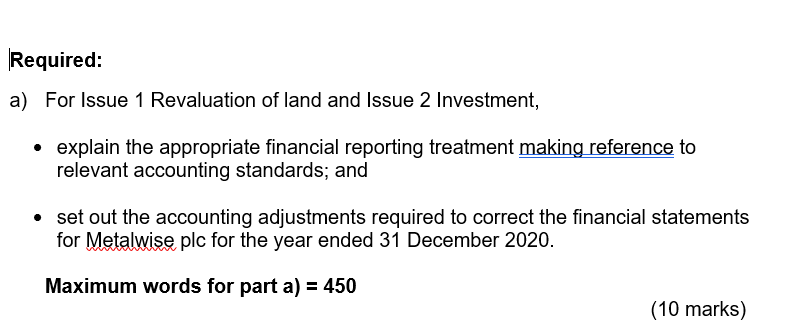

Additional information for the unresolved financial reporting issues in Exhibit 3 Advance information - Issue 1 Revaluation of Land Included in the balance for PPE is a plot of land. The land has been revalued at 31 December 2020 to 30 million. The directors have decided to include this revaluation of land in the statement of financial position but I have not put through the journal entries to recognise the revaluation. Additional information The cost of the land included in the PPE on the statement of financial position at 31 December 2020 is 20 million. In the tax jurisdiction where Metalwise operates, gains on land are taxed when the land is sold in the future period. Advance information - Issue 2 Investment 8,000,000 On 1 February 2020, Metalwise bought 200,000 shares of the issued ordinary share capital of KKL plc, a listed company. Each share cost 40 and he investment which this investment represents a 10% shareholding is a long-term investment in KKL plc. Metalwise incurred legal fees and brokers fees when it made this investment. Additional information Legal and brokers fees (transaction costs) of 500,000 are included in finance costs in the statement of profit or loss for the year ended 31 December 2020. The directors have made an irrevocable election to classify the investment as at fair value through OCI. At 31 December 2020, the fair value of one share in KKL plc was 45 per share. In the tax jurisdiction where Metalwise operates gains on the disposal of equity instruments are not taxable in the current or any future periods. The transaction costs in relation to the acquisition of shares are not allowed as a tax deduction in the year ended 31 December 2020 or in future periods. Required: a) For Issue 1 Revaluation of land and Issue 2 Investment, explain the appropriate financial reporting treatment making reference to relevant accounting standards; and set out the accounting adjustments required to correct the financial statements for Metalwise plc for the year ended 31 December 2020. Maximum words for part a) = 450 (10 marks) Additional information for the unresolved financial reporting issues in Exhibit 3 Advance information - Issue 1 Revaluation of Land Included in the balance for PPE is a plot of land. The land has been revalued at 31 December 2020 to 30 million. The directors have decided to include this revaluation of land in the statement of financial position but I have not put through the journal entries to recognise the revaluation. Additional information The cost of the land included in the PPE on the statement of financial position at 31 December 2020 is 20 million. In the tax jurisdiction where Metalwise operates, gains on land are taxed when the land is sold in the future period. Advance information - Issue 2 Investment 8,000,000 On 1 February 2020, Metalwise bought 200,000 shares of the issued ordinary share capital of KKL plc, a listed company. Each share cost 40 and he investment which this investment represents a 10% shareholding is a long-term investment in KKL plc. Metalwise incurred legal fees and brokers fees when it made this investment. Additional information Legal and brokers fees (transaction costs) of 500,000 are included in finance costs in the statement of profit or loss for the year ended 31 December 2020. The directors have made an irrevocable election to classify the investment as at fair value through OCI. At 31 December 2020, the fair value of one share in KKL plc was 45 per share. In the tax jurisdiction where Metalwise operates gains on the disposal of equity instruments are not taxable in the current or any future periods. The transaction costs in relation to the acquisition of shares are not allowed as a tax deduction in the year ended 31 December 2020 or in future periods. Required: a) For Issue 1 Revaluation of land and Issue 2 Investment, explain the appropriate financial reporting treatment making reference to relevant accounting standards; and set out the accounting adjustments required to correct the financial statements for Metalwise plc for the year ended 31 December 2020. Maximum words for part a) = 450 (10 marks)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts