ADJUSTING ENTRIES

PROBLEM: IN A TABLE, give the necessary adjusting entries WITH THEIR CORRESPONDING AMOUNTS as of December 31, 2003, for the following independent data and events. If an adjusting entry is not required, state the reason.

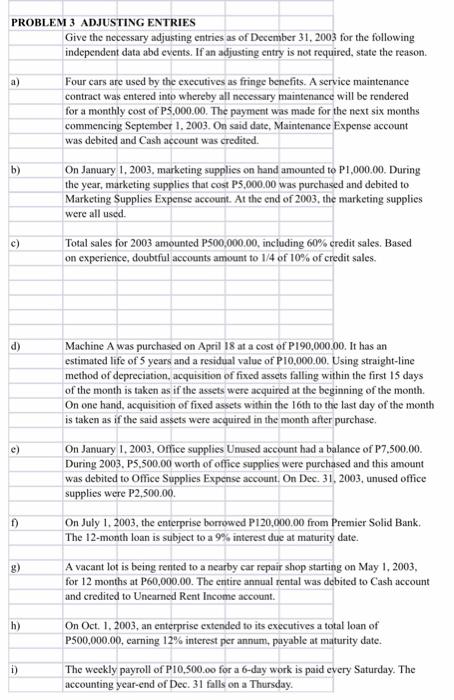

a) Four cars are used by the executives as fringe benefits. A service maintenance contract was entered into whereby all necessary maintenance will be rendered for a monthly cost of P5,000.00. The payment was made for the next six months commencing September 1, 2003. On said date, the Maintenance Expense account was debited and the Cash account was credited.

b) On January 1, 2003, marketing supplies on hand amounted to P1,000.00. During the year, marketing supplies that cost P5,000.00 was purchased and debited to Marketing Supplies Expense account. At the end of 2003, the marketing supplies were all used.

c) Total sales for 2003 amounted to P500,000.00, including 60% credit sales. Based on experience, doubtful accounts amount to 1/4 of 10% of credit sales.

d) Machine A was purchased on April 18 at a cost of P190,000.00. It has an estimated life of 5 years and a residual value of P10,000.00. Using the straight-line method of depreciation, the acquisition of fixed assets falling within the first 15 days of the month is taken as if the assets were acquired at the beginning of the month. On one hand, the acquisition of fixed assets between the 16th to the last day of the month is taken as if the said assets were acquired in the month after purchase.

e) On January 1, 2003, Office Supplies Unused account had a balance of P7,500.00. In 2003, P5,500.00 worth of office supplies were purchased and this amount was debited to the Office Supplies Expense account. On Dec. 31, 2003, Unused Office Supplies were P2,500.00.

f) On July 1, 2003, the enterprise borrowed P120,000.00 from Premier Solid Bank. The 12-month loan is subject to a 9% interest due at maturity date.

g) A vacant lot is being rented to a nearby car repair shop starting on May 1, 2003, for 12 months at P60,000.00. The entire annual rental was debited to Cash account and credited to Unearned Rent Income account.

h) On Oct. 1, 2003, an enterprise extended to its executives a total loan of P500,000.00, earning 12% interest per annum, payable at maturity date.

i) The weekly payroll of P10,500.oo for a 6-day work is paid every Saturday. The accounting year-end of Dec. 31 falls on a Thursday.

Give the necessary adjusting entries as of December 31, 2003 for the following independent data abd events. If an adjusting entry is not required, state the reason. a) Four cars are used by the executives as fringe benefits. A service maintenance contract was entered into whereby all necessary maintenance will be rendered for a monthly cost of P5,000.00. The payment was made for the next six months commencing September 1, 2003. On said date, Maintenance Expense account was debited and Cash account was credited. b) On January 1, 2003, marketing supplies on hand amounted to P1,000.00. During the year, marketing supplies that cost P5,000,00 was purchased and debited to Marketing Supplies Expense account. At the end of 2003, the marketing supplies were all used. \begin{tabular}{|l|l|} \hline c) Total sales for 2003 amounted P500,000.00, including 60% credit sales. Based \\ \hline on experience, doubtful accounts amount to 1/4 of 10% of credit sales. \\ \hline & \\ \hline d) & \\ \hline Machine A was purchased on April 18 at a cost of PI90,000.00. It has an \end{tabular} method of depreciation, acquisition of fixed assets falling within the first 15 days of the month is taken as if the assets were acquired at the beginning of the month. On one hand, acquisition of fixed assets within the 16th to the last day of the month is taken as if the said assets were acquired in the month after purchase