Question: Advanced Financial Planning - Comprehensive Financial Plan Practice Case Overview and Family Situation Maddie and Ryan Findlay have been married for 6 years. Maddie is

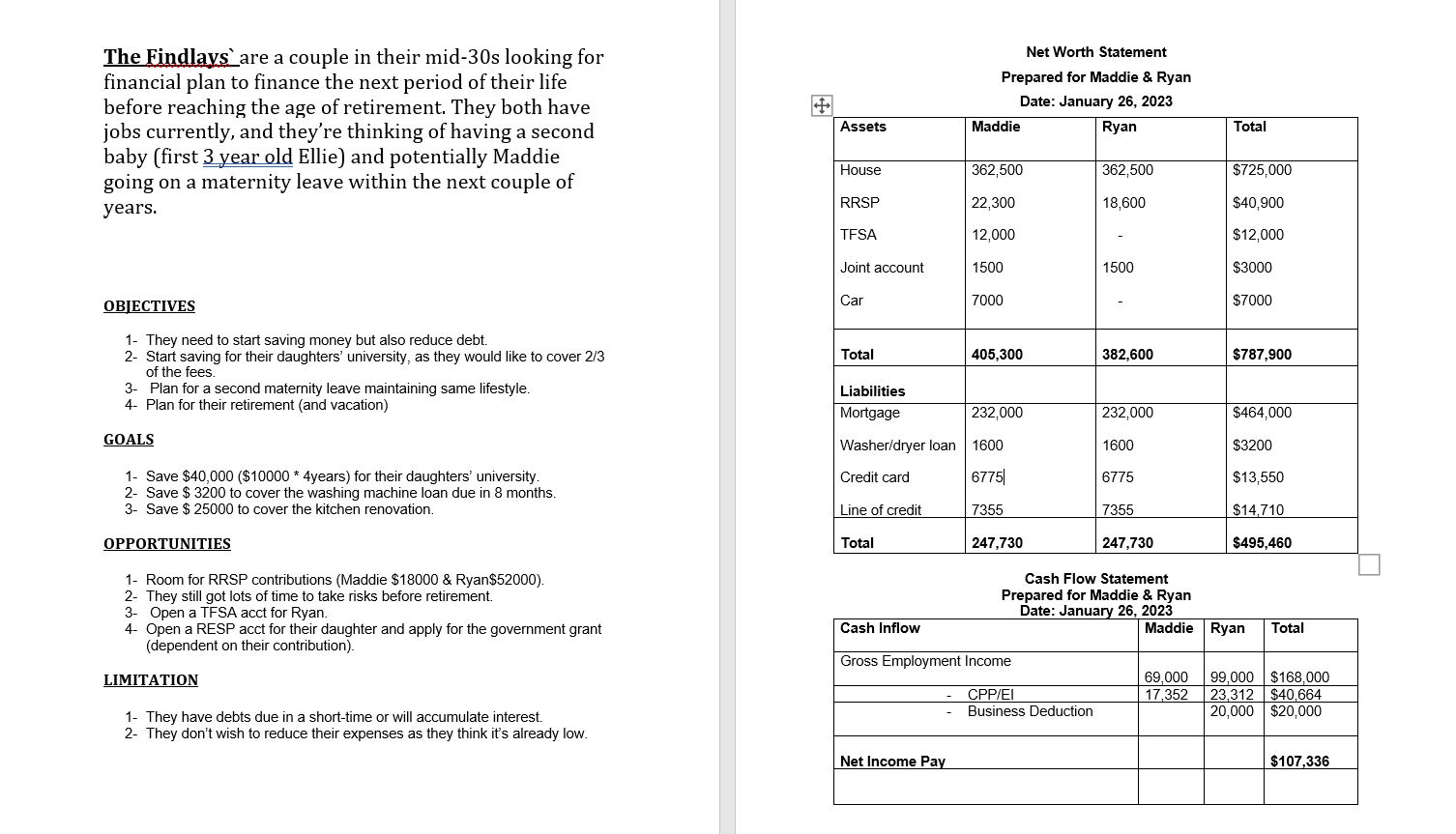

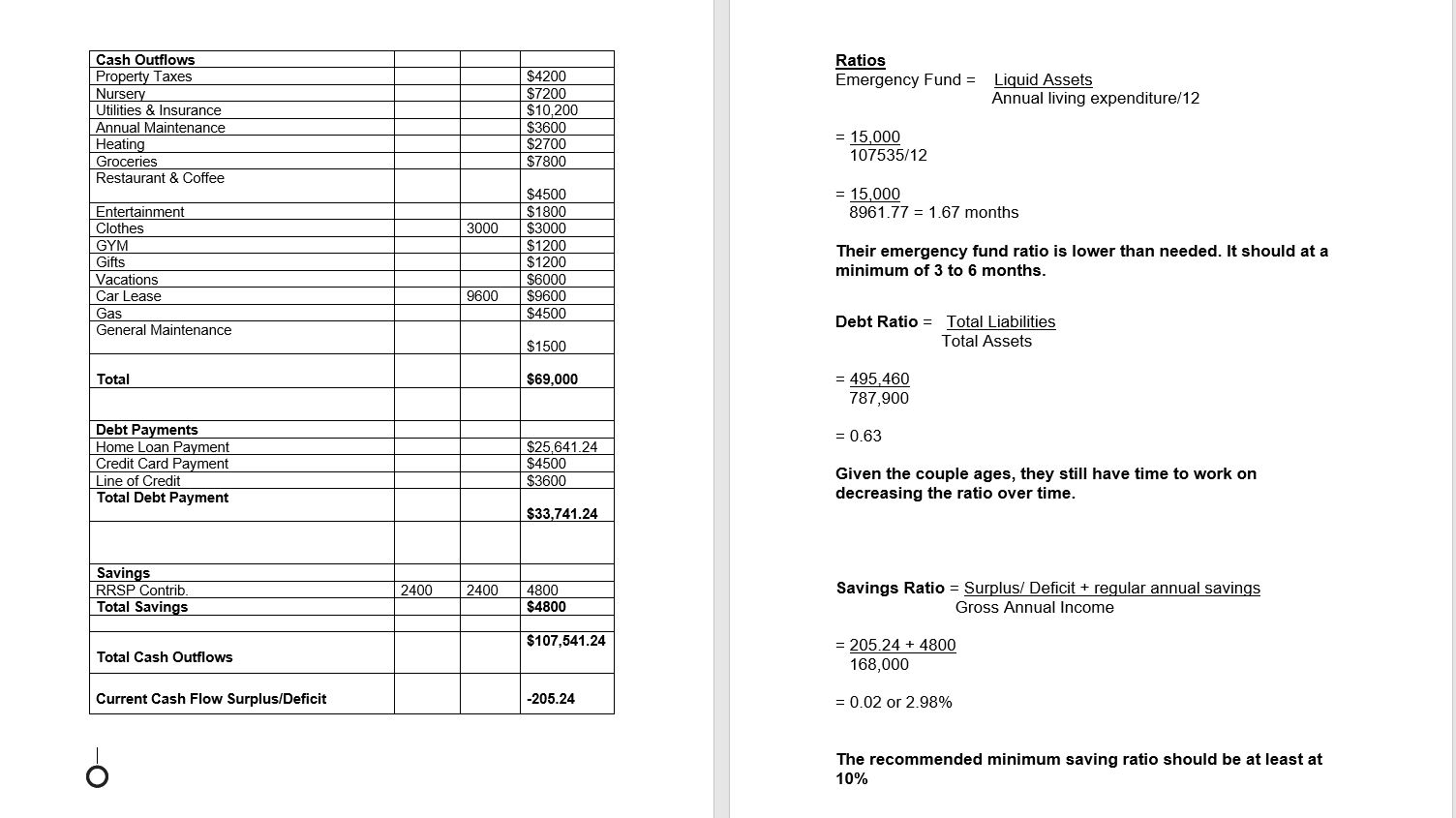

Advanced Financial Planning - Comprehensive Financial Plan Practice Case Overview and Family Situation Maddie and Ryan Findlay have been married for 6 years. Maddie is 34 years and Ryan is 36 years old. This couple lives in Pickering. Ontario. The Findlay's have agueLold daughter named Ellie and they are hoping to have a second child in the next year or two. Employment/Self Employment and Benefits Maddie Findlay Maddie is an emergency room trauma nurse at their local hospital. This is an extremely demanding job that requires her to work long shifts and she never knows what kind ot'patients she will see. Even though her work is challenging she loves her job. She earns $69,000 per year and the hospital provides her and her family with health and dental benets. They also provide disability insurance and life insurance. She pays for her disability insurance each month and it covers her for 60% of her salary based on her 'Own Occupation\" for the rst two years and 'Any Dccupation' after that. Her life insurance through her employer covers her for two times her salary. In addition she is a member of her hospitals dened benet pension plan known as Health Care of Ontario Pension Plan [HODPPL Maddie contributes 6.9% on pensionable earnings up to the YMPE and 9.2% on pensionable earnings for any amount above the YMPE. Maddie joined the pension plan 9-years ago when she started at the hospital. Ryan Findlay Ryan is a real estate agent and alter a rough star'the has built a good book of clients over the last 10 years. He earned gross real estate commissions of$99.000 on average over the last 3 years. Although sales have declined in the rst quarter of this year relative to last year, Ryan is still condent the real estate market and his commissions will pick up later this year. Ryan takes advantage ofthe deductions and business expenses to educe his taxable income. He spends $20,000 a year in marketing costs and other'lnrsinsated expenses. Eeing self-employed. Ryan does not have health benets, disability insurance) life insurance or a pension plan through work. Ellie Findlay Ellie is an adorable and active toddler and is keeping her parents very busy. Maddie and Ryan have been able to work their own schedules so that they have not had to rely on daycare. Being selfeemployed. Ryan has been able to work around Maddie's schedule or ask family members for help when it is necessary forhim to meet clients. She will be starting a nursery school program three days a week next month and it will cost them $608 per month. This will help free up time for Ryan to focus more on his business. Personal Assets Family Home Maddie and Ryan bought their rst home in Pickering dieyeeus ago. They bought an older townhouse for $530,00U with a down payment of 151 161000. They were very fortunate that Maddie was left $66,000 from her grandmother when she passed away and they each used the maximum Home Buyers Plan to come up with the rest They borrowed the remaining amount of $464,000 from their bank and have been making monthly payments of$2.136.77 based on a ZSryear amortization. At the time of 1mm\" signed for a Seyear closed mortgage paying 2.? 5%. There mortgage comes due in a g and they are wondering what the best solution would be for them at that time. Ryan gures that their home is currently worth $725,000. They would like to do a kitchen renovation in the next year as the townhouse is about 20-years old and it is showing its age. They have spoke with some contractors and estimate that it will cost them about $25,080 to do. Automobiles Maddie inherited her gi'andmothersngLold Honda Civic when she passed away. She is planning on driving this car as long as she can because she uses it to commute to work and that is it. They value this car to be worth $7,800. The rest of the time they use Ryan's new Audi Q7 SUV that he bought last year. He leases this vehicle because he uses part ofit for his business. Financial Management Attitudes Towards Spending, Savings and Debt Maddie and Ryan enjoyed life as newlyweds. They would spend time going out with friends to parties, 9113.1); and vacations. When they gotggot they realized that life was goingto change and they were excited about that. However, they were le with some debt and then with Maddie artwork for a year for her maternity leave they incun'ed more debt They realize now that something is going to have to change as they would like to have a second child and do not want to take on more debt to do so. They do not want to sacrice too much of their current standard of living as they feel that they have already given up much of their old lifestyle. Thelast two years they have saved small amounts in their RRSPs because of the need to repay the money they borrowed through the Home Buyers Plan. They have not been able to save any other money. They each put $200 per month into their own RRSP's. Expenses They looked at their credit card and bank smtements to try and understand where they are spending their money. In addition to their monthly mortgage payment. they pay property taxes of $4.200 per year, ijjt'jes and insurance of $350 per month. heating of$225 per month and annual maintenance costs of$3.600. Patti and Ryan spend $650 per month on groceries and $375 per month on restaurants and coffee. They also still enjoy going outwith friends and they spend $150 per month on entertainment Ryan has to dress well for w and they spend $250 per month on clothes. Each of them has a gym membership that cost them a total of$100 per month. They spend about $1,200 per year on gitts and they still enjoy one vacation a year at a cost of $6.000. Ryanis monthly lease payments are $800 per month. The lease rate at the time of purchase was 1.9% for AIS-months. The buyout on the vehicle is $26,000 at the end of the four years. They pay $325 per month in gas for their personal travels and they have general maintenance costs of$1.500 per year. Maddie has deductions from her paycheck for income taxes. CPP and El, totaling $1,446 per month. Ryan pays quarterly instalments for his taxes and CPPtotaling $23,312 annually. Debts The Findlay's have a Scotiabank Mastercard with a balance owing of $13,550. Most of this spending was done in the past but they haven't been able pay the balance down. The available credit on this card is $15,000 and the interest rate is 19%. They make the minimum monthly payments of' $375 per month. They a]so have an unsecured line ot'credit with an available limit of$151000. They have an outstanding balance of$14.710. Most ofthe spending on this account occurred when Maddie was off on maternity leave and her income was signicantly reduced. The interest rate is prime plus 5%. which means they are paying a total of 8%. They make the minimum monthly payment of $300. Finally, they have a buy now pay later loan as their washing machine broke and they had to replace it. They decided to replace both the washer and dryer at the same HE and they used dris type of loan because they did not have the cash. They are required to pay the balance in full in 8-months time. lftheyw they will owe interest on4% starting then they bought them 16 months ago on a balance of $3.200. Asset Management Registered Assets Maddie and Ryan both have a small individual RRSP that they have been contributing to each month to repay the money they used through the Home Buyers Plan. Maddie invests this money in a balanced portfolio of ETF's that is rebalanced on a W. She has a moderate risk prole and she earns an annual rate of return of 5%. The balance in her RRSP account is $22,300 and has unused RRSP contribution room of$18,000. Maddie has named Ryan as the beneciary of her account. Ryan has chosen to open a self-directed RRSPJ where he has been buying penny stocks. He has an interest in investing and he gures that this is a good way to learn. The balance in this account is $13,600 and he has unused RRSF contribution room of $52,000. Ryan has a growth prole and has earned an annual rate ofreturn of?% on average in this account Ryan has not lled out the paperwork to name a beneciary to this account. Maddie has aIaLEme Savings Account [TFSA] where she invested $12,000 from her grandmothers esmte. Shelias set this money aside for herself. She is not sure what she wants to use this money fir but it will be something special that she will remember her grandmother by. ltis currently invested in a cashable GIC earning a rate of return of 1.1% per annum. Maddie has named Ellie as the beneciary to this account. Maddie's Dened Benet Pension Plan benet is based on her best veryears average w and it will be indexed to in ation. The pension benet is calculated based on years of service and 1.5% of pensionable earnings up to the YMPE and 2% of pensionable earnings beyond the YMPE. The pension also provides a bridge benet if she retires before age 65. If she decides to retire she will receive an unreduced pension benet it'she meets the BS factor. Ryan is named as the beneciary to her pension plan. living and take at least three trips a year. They estimate that this would be an addltional$101000 per year above what they are already spending on vacations. Non-Registered Assets They have a joint cllequing account where their pay goes in and where they pay their bills. The balance in that account is $3,000. Risk Management Assumptions Beyond Maddie's benets From work and their home and auto policies. they do not have any individual insurance policies. The couple is worried that if Ryan were unable to work given a M they would not be able to make ends meet. They also have the same concerns if either one ofthern were to die. They believe that if either of them % to die they would need $50,000 per year until retirement to supplement the surviving spouses income. Maddie and Ryan have a combined marginal tax rate of 30% Ination 2% Life expectancy age 95 Current Mortgage Rates: 0 1-year xed rate of2.99% Zryear xed rate of 2.99% 3ryear xed rate of 2.84% 47year xed rate of3.14% Sryear xed rate of 2.79% o Sryear variable rate of 2.70% I Fixedrrate Loan Rates: C) 3ryear xed rate of 7% o Sryear xed rate of 8% Estate Planning and Legal Documents Maddie and Ryan believe they are too young to be thinking about estate planning. They have not drafted wills or powers of attorney. 0000 Short-term and tong-term Objectives Short-term Objectives Maddie and Ryan have not clearly dened their nancial objectives for the short? terln. They know that they would like to have a second child Within the next two w and they don't want to have to borrow money while Maddie is offon maternity leave again. They would also like to get their debt under control as they are nding a good portion of their pay is going to service their debt. The couple is also not sure how they will pay for their buy now pay later loan when it comes due. Maddie and Ryan would like to W for Ellie's education. They have not started yet and are unsure ofwhere to begin. They would like to contribute two thirds of her education costs and they estimate that would be about $10,000 per year [in today/s dollars] for four years. Long-term Objectives Maddie and Ryan haven't talked too much about retirement, as it seems like it is so far away. Maddie knows that she likely won't be able to keep up with the pace of the emergency room past the age off-0. She is thinking that she would like to retire then. Ryan is thinking that he will retire with Maddie, but he is considering working partitime past retirement, as he really enjoys Working with his clients to help them nd their dream homes. They would also like to maintain their current standard of \fCash Outflows Ratios Property Taxes $4200 Emergency Fund = Liguid Assets NUKSPW $7200 Annual living expenditure/12 Utilities & Insurance $10 200 Annual Maintenance $3600 7 Heating $2700 ' 15 000 Groceries $7800 107535112 Restaurant & Coffee $4500 : 15 000 Entertainment $1800 8961]? 2 1 67 months Clothes 3000 $3000 gar: $1388 Their emergency fund ratio is lower than needed. It should at a Vacations $8000 minimum of 3 to 6 months. Car Lease 9600 $9800 Gas $4500 General Maintenance Debt Ratio : Total Liabilities $1500 Total Assets Total $59,000 = 495.460 787,900 Debt Payments = 053 Home Loan Payment $25 641,24 0 (it C) d P t 4500 _ . . Urn: 13f grrEdmaymen $3800 Given the couple ages, they still have time to work on Total Debt payment decreasing the ratio over time. $30,741.24 Savings RRSP Contrib, 2400 2400 4800 Savings Ratio : Sur lusf Deficit + re ular annual savin 5 Total Savings $4800 Gross Annual income 1- m h o m 510154124 : 205 24 + 4300 ota as u 0W5 168,000 Current Cash Flow Surpluleeficit 405.24 : 0 02 0; 2 98% ' The recommended minimum saving ratio should be at least at O 10%

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Accounting Questions!