Question: After reading this auditing ESG, what do you consider will be the effects of Auditing in the future based on Section 5 Practicalities of reporting?

After reading this auditing ESG, what do you consider will be the effects of Auditing in the future based on Section 5 Practicalities of reporting?

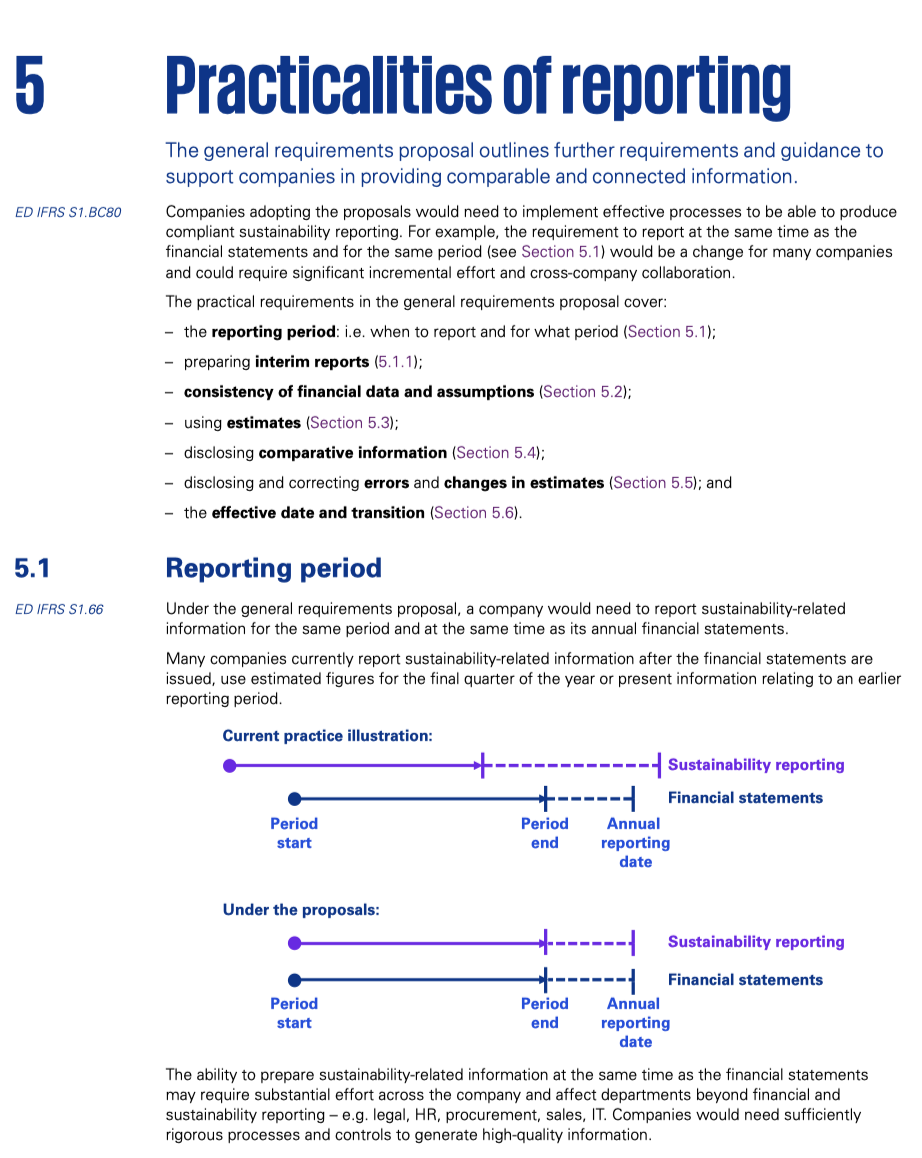

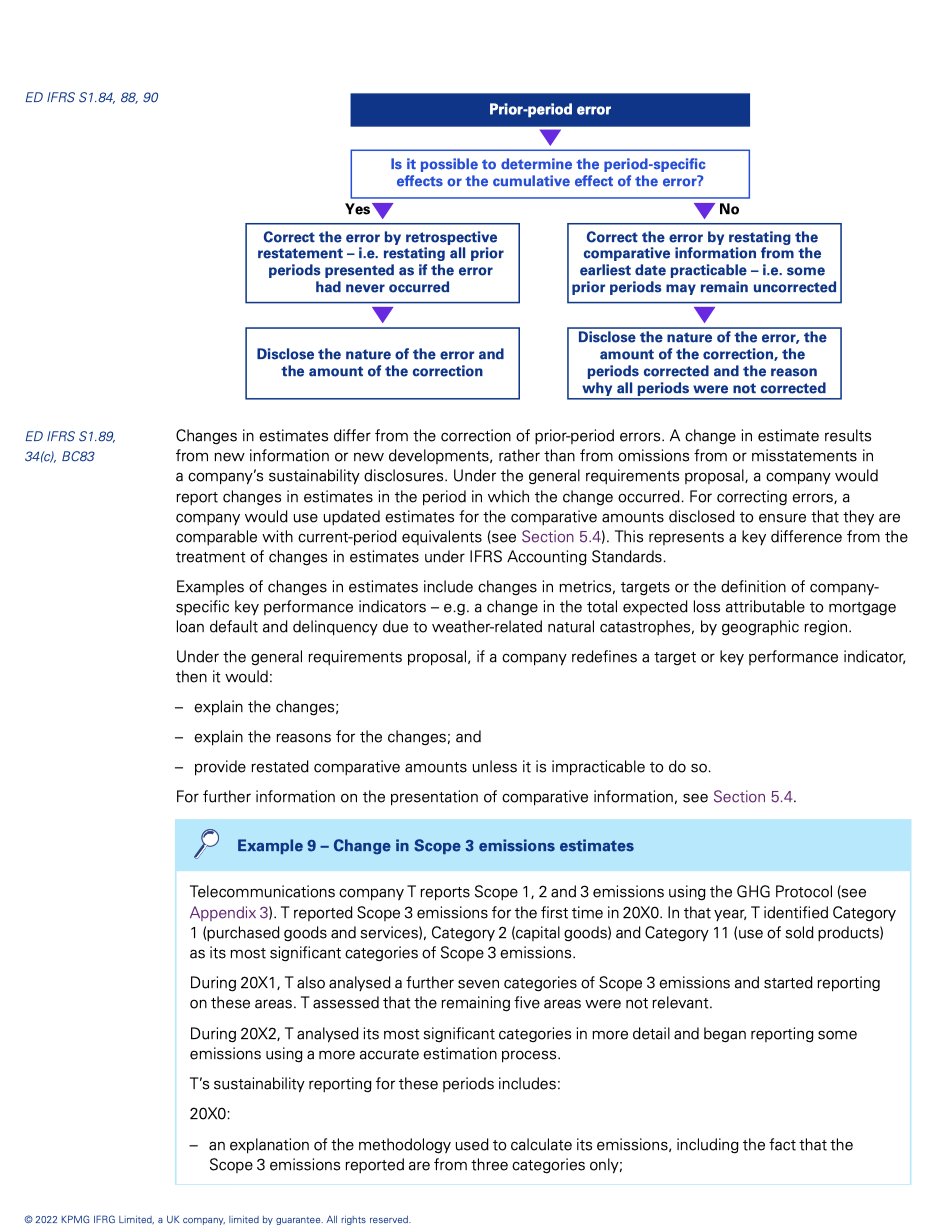

5 Practicalities of reporting The general requirements proposal outlines further requirements and guidance to support companies in providing comparable and connected information. ED IFRS S1.BC80 Companies adopting the proposals would need to implement effective processes to be able to produce compliant sustainability reporting. For example, the requirement to report at the same time as the financial statements and for the same period (see Section 5.1) would be a change for many companies and could require significant incremental effort and cross-company collaboration. The practical requirements in the general requirements proposal cover: the reporting period: i.e. when to report and for what period (Section 5. 1); - preparing interim reports (5.1.1); - consistency of financial data and assumptions (Section 5.2); using estimates (Section 5.3); disclosing comparative information (Section 5.4); disclosing and correcting errors and changes in estimates (Section 5.5); and the effective date and transition (Section 5.6). 5.1 Reporting period ED IFRS S1.66 Under the general requirements proposal, a company would need to report sustainability-related information for the same period and at the same time as its annual financial statements. Many companies currently report sustainability-related information after the financial statements are issued, use estimated figures for the final quarter of the year or present information relating to an earlier reporting period Current practice illustration: -------------- Sustainability reporting -- Financial statements Period Period Annual start end reporting date Under the proposals: Sustainability reporting --- Financial statements Period Period Annual start end reporting date The ability to prepare sustainability-related information at the same time as the financial statements may require substantial effort across the company and affect departments beyond financial and sustainability reporting - e.g. legal, HR, procurement, sales, IT. Companies would need sufficiently rigorous processes and controls to generate high-quality information.ED inf-"HS 31.?! 5.1.1 so was 51.5970 5.2 ED iFFiS $1.80 Under the general requirements proposal. a company would also disclose information about transactio ns. other events and conditions that occur or arise after the reporting date but before the date on which the sustainability-related financial disclosures are authorised for issue. The company would disclose information if its exclusion would be expected to inuence investors' decisions. This concept appears similar to the guidance on reporting events after the reporting date in IFHS Accounting Standards. Interim reporting The Standards would not require companies to provide interim sustainability-related information. However, local laws and regulations could require interim reports to be prepared or a company could choose to prepare interim reporting on a voluntary basis. Unless local requirements state otherwise. companies would be permitted to prepare any interim sustainability-related information in accordance with the Standards. Do the proposals define the sustainability-related financial disclosures to be included -._';-. in interim reporting? No. The proposals do not contain prescriptive disclosure requirements for interim reporting. The extent of information that a company would provide would depend on local laws and regulations. If a company presents an interim report. then it would prepare either a complete set of sustainability disclosures {see Section 2.3] or more condensed interim sustainability disclosures. Although there is no prescriptive guidance on interim disclosures, the ISSB Board's intention is for interim disclosures to provide an update on the company's latest complete set of annual disclosures. Therefore. companies would be expected to focus on the disclosure of new information. events and circumstances in their interim reporting. For example, they might focus on metrics and targets disclosures in the interim reporting rather than governance and risk management information, which is often subject to less change. Similarly. the disclosure of strategy-related information would depend on the occurrence of new events during the interim period. Consistency of financial data and assumptions Achieving connectivity between sustainability reporting and financial reporting is important. Management's views on each significant sustainabilityerelated risk or opportunity would need to inform both the sustainability reporting and financial statements. This means that although sustainability-related information may differ in nature from the financial statements. it should be consistent to the extent possible. For example. if a company has made and disclosed climate- related commitments in the front part of the annual report. then the assumptions used in the financial statements would be consistent. where appropriate. but would consider the recognition and measurement requirements of the applicable financial reporting framework. Commitments are one of the most common areas where sustainability reporting and lFFlS Accounting Standards differ. This is because only those commitments that meet the IAS 3710 recognition requirements are recognised in the financial statements. The assumptions used in sustainability reporting and financial reporting may also differ because of requirements in lFFIS Accounting Standards. In these instances, disclosing the differences in assumptions and the reasons for those differences would help users to understand and to reconcile the information in the sustainability disclosures with the financial statements. For example, a company may consider discussing why key assumptions used in estimates in the financial statements differ from net-zero commitmentsfscenarios and the impacts disclosed in the front part of the annual report e.g. it might discuss the differences between the key assumptions used in impairment testing and 'Paris- aligned' assumptions used in scenario analysis disclosures. ED lFHS $1.22 5.3 ED lFFlS Si. 19, 33 See our web article Have you disclosed the impacts of climate-related matters cleanly? for further information. Consistency of financial data and assumptions would also be required for the following: financial data used to normalise metrics {e.g. metrics may be linked to a financial statement caption, such as greenhouse gas emissions per unit of revenue]: - activity metrics that rely on similar data sources to financial metrics leg. the same sales data may be used for an activity metric relating to number of products sold and for revenue disclosures]: disclosures on concentration of risk in the value chain that may be connected to risk concentration disclosures in the financial statements; and the same currency used as the unit of measure for sustainability disclosures and as the presentation currency in the company's nancial statements. Would the proposals require better connectivity with the financial statements _- compared to current sustainability reporting? Yes. For example. the proposals include disclosure requirements on the impact of sustainability- reIated risks and opportunities on a company's current financial position. performance and cash flows {see 3.3.4}. The 2021 TCFD status report11 identified that of the TCFD adopters consulted, only 20% disclosed impacts on financial performance and 14% disclosed impacts on financial position. This included both qualitative, directional information and quantitative plans, budgets and actual financial impacts. Although disclosing the impact on financial position and performance is just one example of financial statement connectivity, this survey demonstrated that even among TCFD adopters {who may be some of the most advanced in this regard}, there would need to be significant improvements in connectivity to com ply with the proposals. Use of estimates Preparing disclosures for sustainability reporting will inevitably involve the use of estimates. This could be because information is forward looking, or because of a lack of relevant historical data or accurate measurement techniques. Estimates often require management to make difficult, subjective or complex judgements. The number of variables and assumptions affecting those judgements means that there is uncertainty underlying many estimates. Estimation uncertainty could arise either when presenting historical information or in management's predictions of future outcomes. When companies use estimates. they would need to disclose information including: which metrics or other disclosures have significant estimation uncertainty: the sources and nature of the estimation uncertainties and the factors affecting those uncertainties; and - the methods used to calculate targets and inputs into calculations, along with the significant assumptions made and the limitations of those methods. The focus on judgements and estimates in the proposals is similar to that in financial reporting, specifically IAS 1'3. Information about possible future events is also likely to be important. This could be where events have not affected financial performance or financial position, or are not reported in the financial statements. 'I 1. Task Force on Climate-Related Financial Disclosures. W. 12. IAS 1 Presentation of Financial Statements. ED $915518? ED iFRS 51.82 5.4 ED iFRSSi'.63 ED iFHS 51.64. 8532-56153 ED JFRS 51.65.82 ED iFHSSi'.85 Companies would need to consider the following when making materiality judgements about possible future events: - the potential effects of the events on the value. timing and certainty of the company's future cash flows. including in the long term {the possible outcome}: and - the range of possible outcomes and the likelihood of the possible outcomes within that range. A company would consider all relevant facts and circumstances when investigating possible outcomes. as well as information about low-probability and high-impact outcomes that could become material when they are aggregated. For example. a company's supply chain could be disrupted if it is exposed to a wide variety of sustainability-related risks. Information about the aggregate risk affecting the supply chain could be material even if the risks are not considered individually to be significant. Internal processes would need to be sufficient to capture this granular risk information to ensure that information that is material in aggregate can be reported. Comparative information Under the general requirements proposal. a company would disclose comparative information for the previous period for all metrics disclosed in the current period. Companies would also include comparative information for narrative and descriptive disclosures when the information would be relevant to the users' understanding of the current period's disclosures. Unlike in IFFIS Accounting Standards. comparative information presented would reflect updated estimates. When a company reports comparative information that differs from the information it reported in the previous period. it would disclose: - the difference between the amount reported in the previous period and the revised comparative amount: and - the reason why the amounts have been revised. There would be exceptions to these requirements: - in the first year of adoption isee 5.6.1}: or - when a company cannot collate the required information. For example. following a change in methodology or estimate. a company identifies that it did not collate the information that it needed in prior periods to restate the comparatives and is unable to recreate it in the current period. In this case. the company would explain the reason why it was not able to restate its comparatives. Errors and changes in estimates The general requirements proposal defines prior-period errors as omissions from. and misstatements in. a company's sustainability disclosures for one or more periods. These errors would arise from a failure to use or the misuse of reliable information that: - was available when the general purpose financial reporting for those periods was authorised for issue; and - the company could reasonably have obtained and considered in preparing those sustainability disclosures. This diagram depicts the process that would be followed after identifying a prior period error: ED IFRS S1.84, 88, 90 Prior-period error Is it possible to determine the period-specific effects or the cumulative effect of the error? Yes No Correct the error by retrospective Correct the error by restating the restatement - i.e. restating all prior comparative information from the periods presented as if the error earliest date practicable - i.e. some had never occurred prior periods may remain uncorrected Disclose the nature of the error, the Disclose the nature of the error and amount of the correction, the the amount of the correction periods corrected and the reason why all periods were not corrected ED IFRS S1.89, Changes in estimates differ from the correction of prior-period errors. A change in estimate results 34(c), BC83 from new information or new developments, rather than from omissions from or misstatements in a company's sustainability disclosures. Under the general requirements proposal, a company would report changes in estimates in the period in which the change occurred. For correcting errors, a company would use updated estimates for the comparative amounts disclosed to ensure that they are comparable with current-period equivalents (see Section 5.4). This represents a key difference from the treatment of changes in estimates under IFRS Accounting Standards. Examples of changes in estimates include changes in metrics, targets or the definition of company- specific key performance indicators - e.g. a change in the total expected loss attributable to mortgage loan default and delinquency due to weather-related natural catastrophes, by geographic region. Under the general requirements proposal, if a company redefines a target or key performance indicator, then it would: - explain the changes; - explain the reasons for the changes; and provide restated comparative amounts unless it is impracticably to do so. For further information on the presentation of comparative information, see Section 5.4. Example 9 - Change in Scope 3 emissions estimates Telecommunications company T reports Scope 1, 2 and 3 emissions using the GHG Protocol (see Appendix 3). T reported Scope 3 emissions for the first time in 20X0. In that year, Tidentified Category 1 (purchased goods and services), Category 2 (capital goods) and Category 11 (use of sold products) as its most significant categories of Scope 3 emissions. During 20X1, T also analysed a further seven categories of Scope 3 emissions and started reporting on these areas. T assessed that the remaining five areas were not relevant. During 20X2, T analysed its most significant categories in more detail and began reporting some emissions using a more accurate estimation process. T's sustainability reporting for these periods includes: 20XO: an explanation of the methodology used to calculate its emissions, including the fact that the Scope 3 emissions reported are from three categories only;5.6 ED ill-"85513? ED iFS $7.9i92 5.6.1 E0 was 57.32 ED iFHSSi.9i' 20X1 '. an explanation that the number of categories of Scope 3 emissions reporting has increased, because the company has analysed these categories forthe first time: a breakdown by category of the types of emissions reported and excluded. including explanations; and an explanation that T restated its comparatives to include additional categories; zoxz: an explanation of where and how the methodology used to calculate certain categories of Scope 3 emissions has changed, with an explanation of why management expects the new methodology to be more accurate: and an explanation that the company has not restated comparatives. because it did not collate the relevant data in prior years. Effective date and transition Although the proposals do not specify an effective date! the ISSB Board has stated that it aims to issue the final standards before the end of 2022. Companies would be allowed to apply the standards before the effective date. provided that they disclose that fact. Irrespective of the effective date chosen by the ISSB Board! it will be for local jurisdictions to determine when to mandate adoption of the Standards. Companies complying with all of the relevant requirements would include a statement of compliance with the Standards. This statement could still be included if disclosures were complete except for information that was prohibited by local laws or regulations. Transition provisions Disclosures would not be required for any period before the date of initial application. This means that comparative information would not be required in the first period of adoption. However. some companies may have reported similar information previously under other frameworks. It may therefore be useful to align comparatives to the proposals, when the data is available to do this. -. Could companies adopt some of the requirements but not all? '- Yes. A company would be able to adopt certain requirements from the proposals but not all. provided that it did not include a statement claiming compliance with the Standards and this was permitted by its local jurisdiction. For example! a company could provide all disclosures required under the climate proposal. but limited information on other significant sustainability-related risks and opportunities. Because the general requirements proposal requires companies to include all material informatio n. in this situation the company would not include a statement of compliance with the Standards

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Accounting Questions!