Question: Almost all option pricing models are based on the concept of a riskless hedge. Investors can create a riskless hedge by purchasing shares of stock

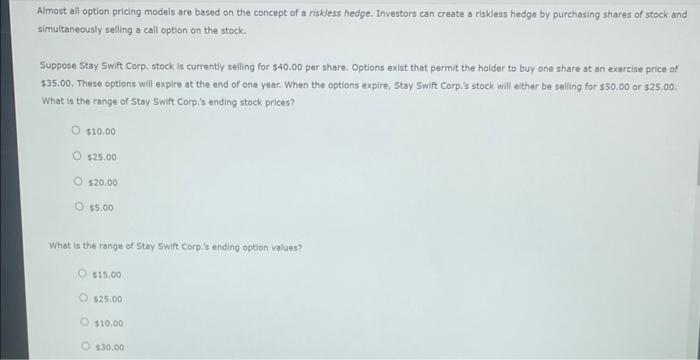

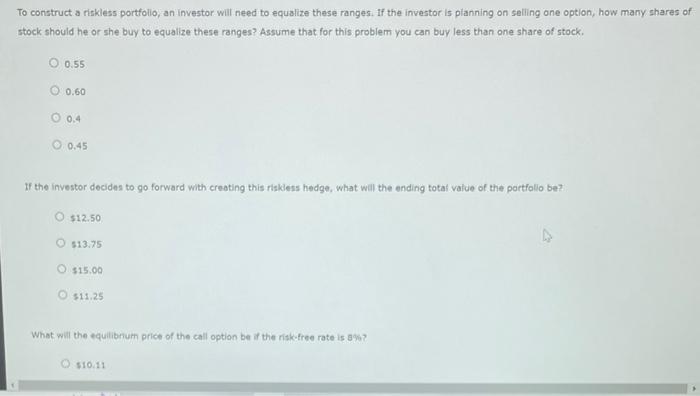

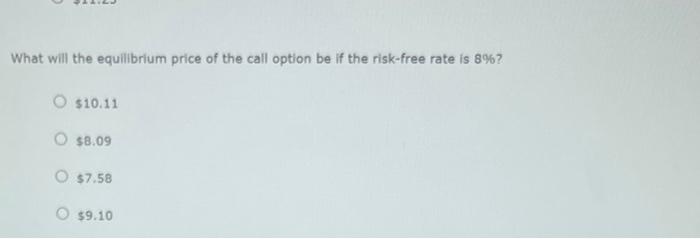

Almost all option pricing models are based on the concept of a riskless hedge. Investors can create a riskless hedge by purchasing shares of stock and simultaneously selling a call option on the stock. Suppose Stay 5 wift Corp, stock is currently selling for $40.00 per share. Options exist that permit the holder to buy one share at an exercise price of $35.00. These options will expire at the end of one year. When the options expire, 5 toy 5 wift Corp.'s stock will either be seling for $50.00 or 525.00. What is the range of 5 tay 5wift Corpi's ending stock prices? $10.00 525.00 520,00 55.00 What is the range of Stay Swift Corp.'s ending option values? $15.00 325.00 $10.00 530,00 To construct a riskless portfollo, an investor will need to equalize these ranges. if the investor is pianning on seling one option, how many shares of stock should he or she buy to equalize these ranges? Assume that for this problem you can buy less than one share of stock. 0.55 0.60 0.4 0.45 If the investor decides to go forward with creating this riskiess hedge, what will the ending total value of the portfollo be? 512.50 513.75 315,00 $11,25 What will the equilibrium price of the call option be if the risk-free rate is 8% ? $10.11 What will the equilibrium price of the call option be if the risk-free rate is 8% ? 510.11 38.09 57.58 $9.10

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts