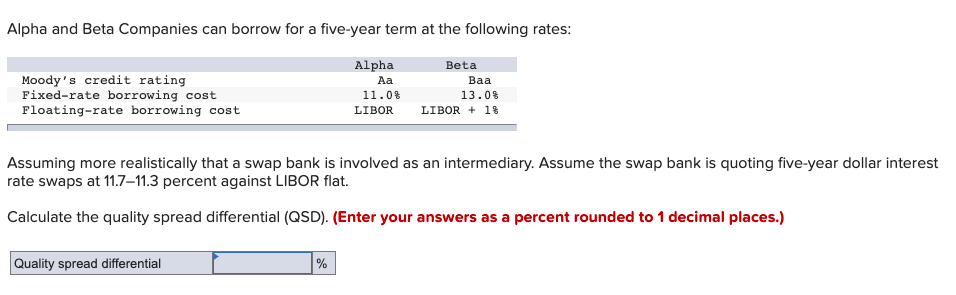

Question: Alpha and Beta Companies can borrow for a five-year term at the following rates: Moody's credit rating Fixed-rate borrowing cost Floating-rate borrowing cost Alpha 11.0%

Alpha and Beta Companies can borrow for a five-year term at the following rates: Moody's credit rating Fixed-rate borrowing cost Floating-rate borrowing cost Alpha 11.0% LIBOR Beta Baa 13.03 LIBOR + 13 Assuming more realistically that a swap bank is involved as an intermediary. Assume the swap bank is quoting five-year dollar interest rate swaps at 11.711.3 percent against LIBOR flat. Calculate the quality spread differential (QSD). (Enter your answers as a percent rounded to 1 decimal places.) Quality spread differential %

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock