Question: Already have A & B so everything else please! In R Studio please! 4. Statistical Inference. = = Consider matrix M = [1, x, z,

Already have A & B so everything else please! In R Studio please!

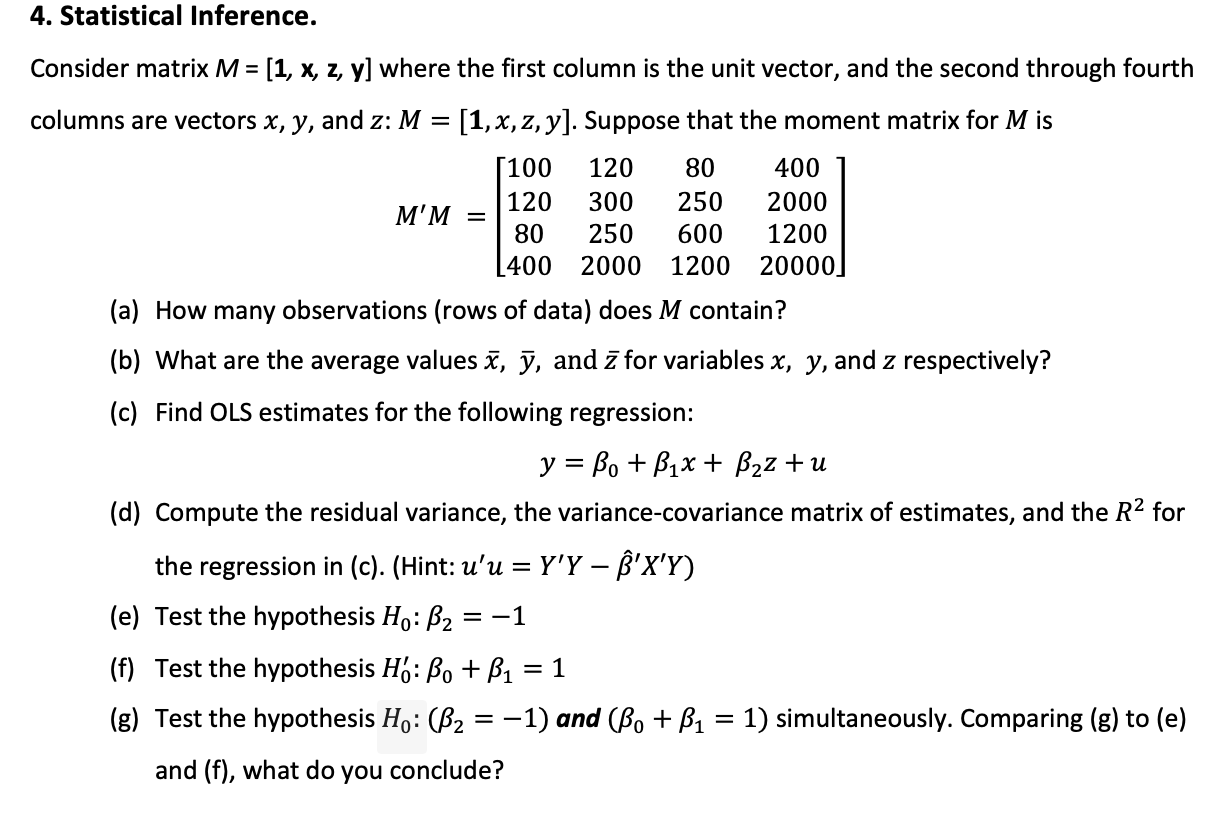

4. Statistical Inference. = = Consider matrix M = [1, x, z, y] where the first column is the unit vector, and the second through fourth columns are vectors x, y, and z: M = [1,x,z,y). Suppose that the moment matrix for M is [100 120 80 400 120 300 250 2000 M'M = 80 250 600 1200 L400 2000 1200 20000] (a) How many observations (rows of data) does M contain? (b) What are the average values , , and z for variables x, y, and z respectively? (c) Find OLS estimates for the following regression: y = Bo + B1x + Bzz +u (d) Compute the residual variance, the variance-covariance matrix of estimates, and the R2 for the regression in (c). (Hint: u'u = Y'Y B'X'Y) (e) Test the hypothesis Ho: B2 = -1 = = (f) Test the hypothesis H: Bo + B1 = 1 (g) Test the hypothesis Ho: (B2 = -1) and (Be + B1 = 1) simultaneously. Comparing (g) to (e) and (f), what do you conclude? = = 4. Statistical Inference. = = Consider matrix M = [1, x, z, y] where the first column is the unit vector, and the second through fourth columns are vectors x, y, and z: M = [1,x,z,y). Suppose that the moment matrix for M is [100 120 80 400 120 300 250 2000 M'M = 80 250 600 1200 L400 2000 1200 20000] (a) How many observations (rows of data) does M contain? (b) What are the average values , , and z for variables x, y, and z respectively? (c) Find OLS estimates for the following regression: y = Bo + B1x + Bzz +u (d) Compute the residual variance, the variance-covariance matrix of estimates, and the R2 for the regression in (c). (Hint: u'u = Y'Y B'X'Y) (e) Test the hypothesis Ho: B2 = -1 = = (f) Test the hypothesis H: Bo + B1 = 1 (g) Test the hypothesis Ho: (B2 = -1) and (Be + B1 = 1) simultaneously. Comparing (g) to (e) and (f), what do you conclude? = =

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts