Question: American call option K=100 SO=200 T=5 year O=0.3 continously compounded rate = 5% 8 = 3% Create a binomial model to calculate price using 500

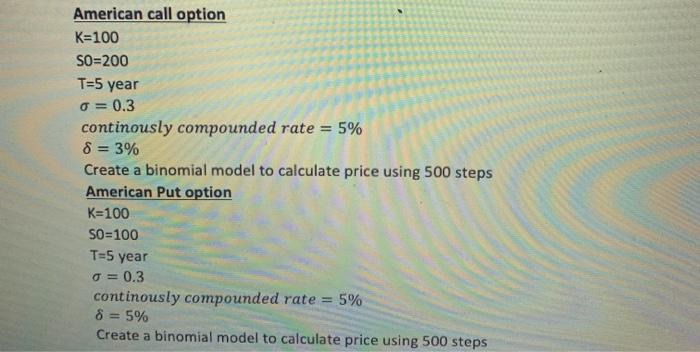

American call option K=100 SO=200 T=5 year O=0.3 continously compounded rate = 5% 8 = 3% Create a binomial model to calculate price using 500 steps American Put option K=100 SO=100 T=5 year O=0.3 continously compounded rate = 5% 8 = 5% Create a binomial model to calculate price using 500 steps American call option K=100 SO=200 T=5 year O=0.3 continously compounded rate = 5% 8 = 3% Create a binomial model to calculate price using 500 steps American Put option K=100 SO=100 T=5 year O=0.3 continously compounded rate = 5% 8 = 5% Create a binomial model to calculate price using 500 steps

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock