An amortized loan is a loan that is to be repaid in equal amounts on a...

Fantastic news! We've Found the answer you've been seeking!

Question:

![]()

Transcribed Image Text:

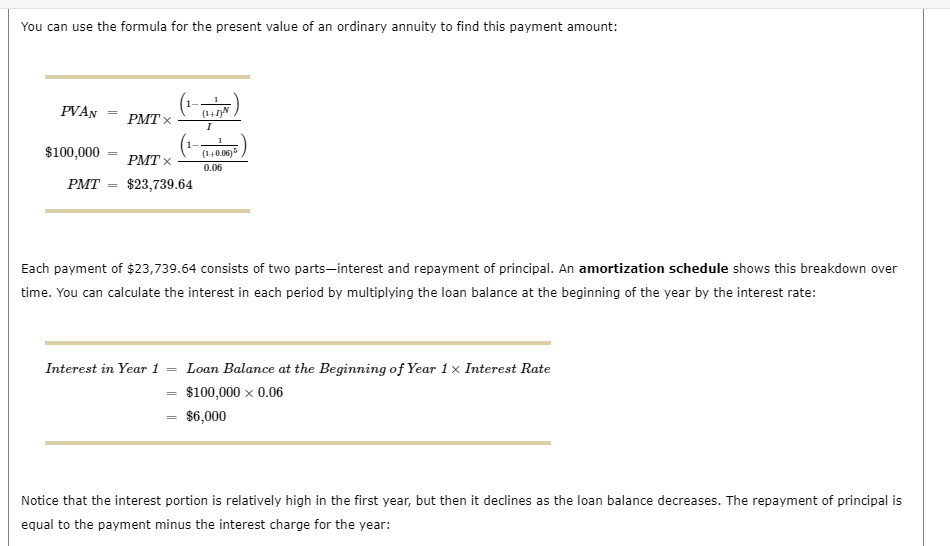

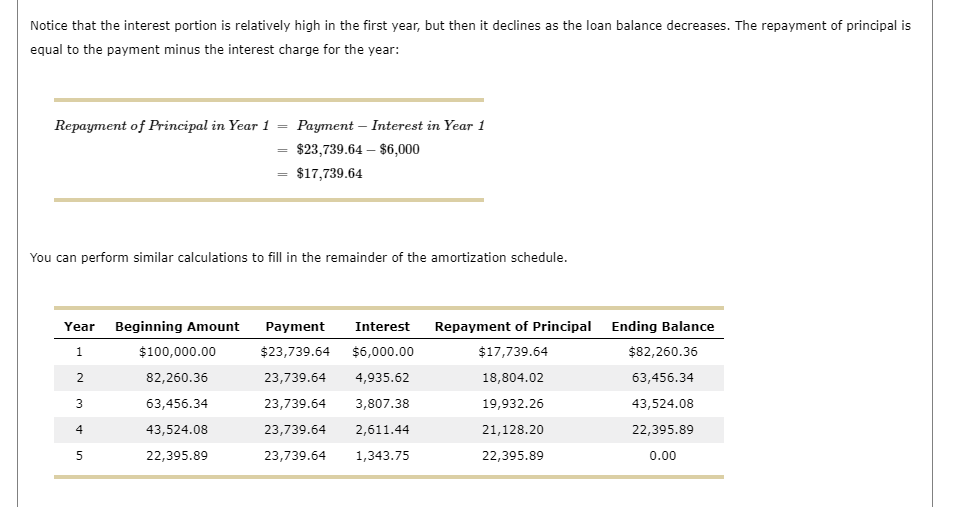

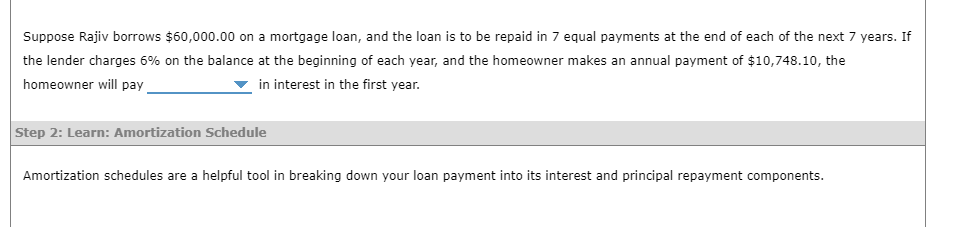

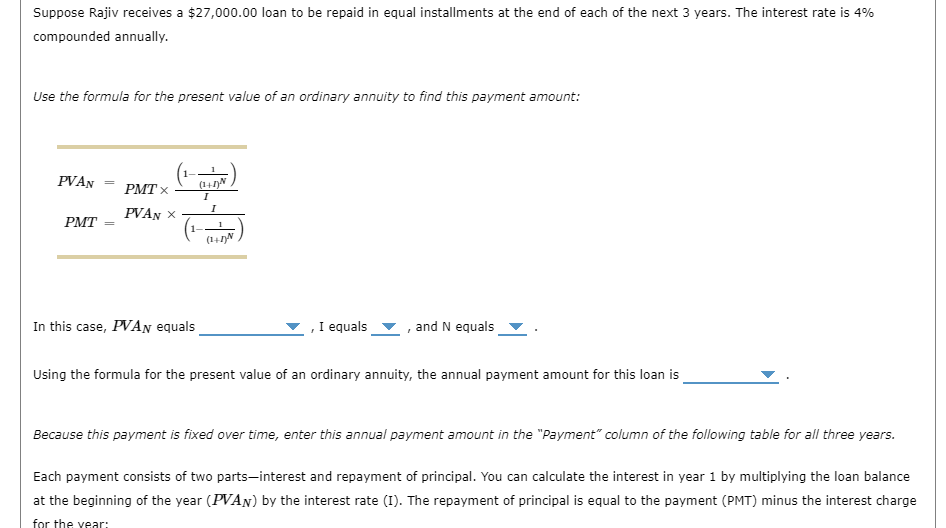

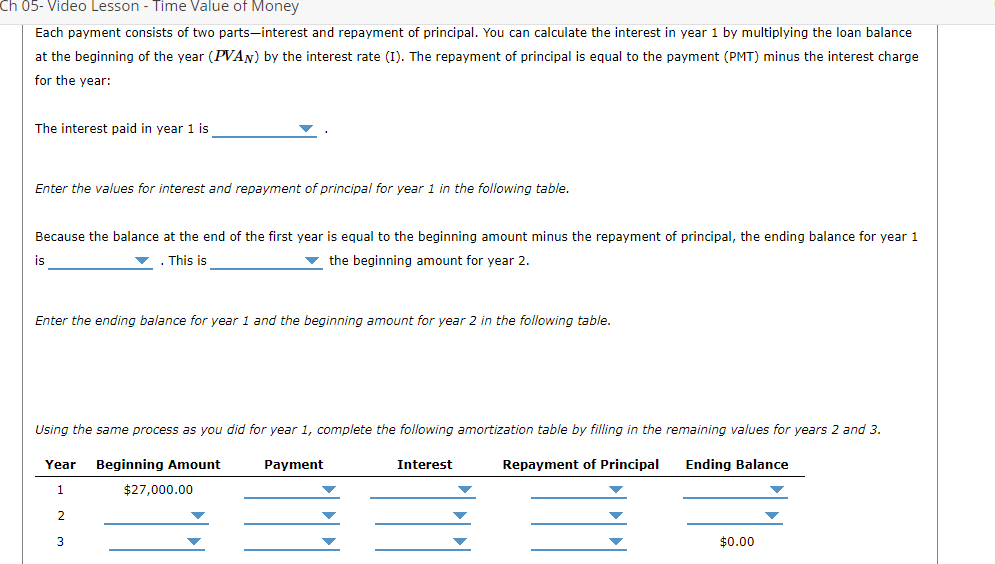

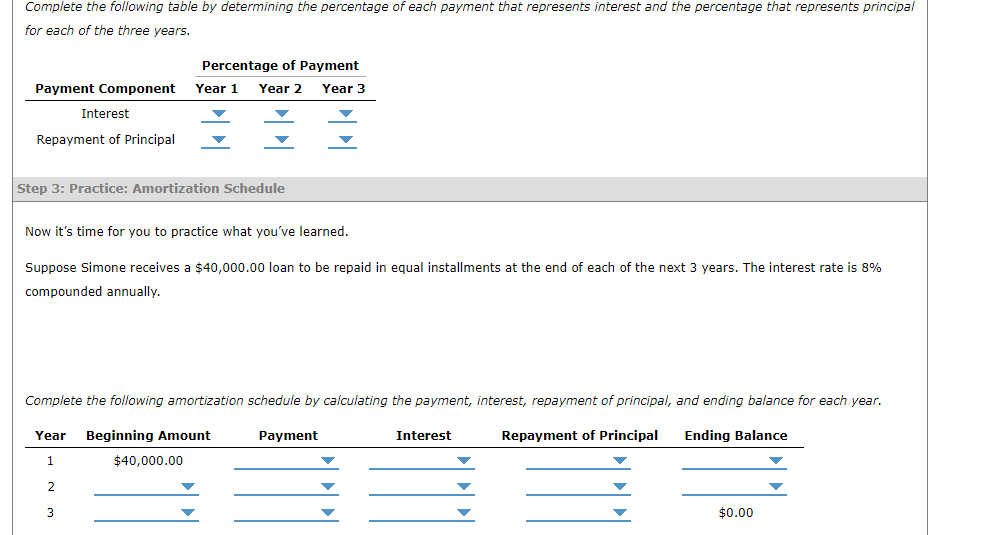

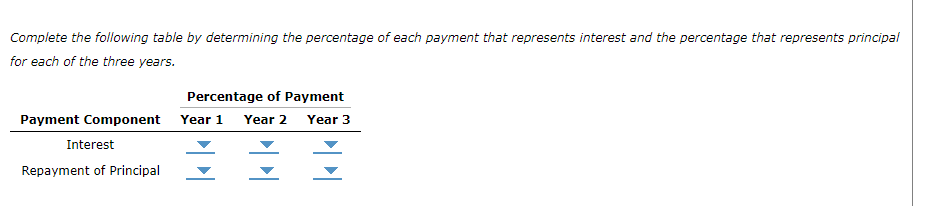

An amortized loan is a loan that is to be repaid in equal amounts on a monthly, quarterly, or annual basis. Many loans such as car loans, home mortgage loans, and student loans are paid off over time in regular, fixed installments; these loans are a great real-world application of compound interest. For example, suppose a homeowner borrows $100,000 on a mortgage loan, and the loan is to be repaid in 5 equal payments at the end of each of the next 5 years. If the lender charges 6% on the balance at the beginning of each year, what is the payment the homeowner must make each year? Given what you know about present value (PV) and future value (FV), you can deduce that the sum of the PV of each payment the homeowner makes must add up to $100,000: $100,000 = 1.06¹ PMT PMT PMT + + 1.062 1.063 5 PMT Σ 1.06² t=1 + PMT 1.064 + PMT 1.06 What is an amortization schedule? You can use the formula for the present value of an ordinary annuity to find this payment amount: PVAN $100,000 PMT PMT X PMT X $23,739.64 Interest in Year 1 Each payment of $23,739.64 consists of two parts-interest and repayment of principal. An amortization schedule shows this breakdown over time. You can calculate the interest in each period by multiplying the loan balance at the beginning of the year by the interest rate: = (1+1)N I = (1+0.06) 0.06 Loan Balance at the Beginning of Year 1 x Interest Rate $100,000 x 0.06 $6,000 Notice that the interest portion is relatively high in the first year, but then it declines as the loan balance decreases. The repayment of principal is equal to the payment minus the interest charge for the year: Notice that the interest portion is relatively high in the first year, but then it declines as the loan balance decreases. The repayment of principal is equal to the payment minus the interest charge for the year: Repayment of Principal in Year 1 = Payment Interest in Year 1 = $23,739.64 - $6,000 = $17,739.64 You can perform similar calculations to fill in the remainder of the amortization schedule. Year 1 2 3 4 5 Beginning Amount Payment Interest $23,739.64 $6,000.00 23,739.64 4,935.62 23,739.64 3,807.38 23,739.64 2,611.44 23,739.64 1,343.75 $100,000.00 82,260.36 63,456.34 43,524.08 22,395.89 Repayment of Principal $17,739.64 18,804.02 19,932.26 21,128.20 22,395.89 Ending Balance $82,260.36 63,456.34 43,524.08 22,395.89 0.00 Suppose Rajiv borrows $60,000.00 on a mortgage loan, and the loan is to be repaid in 7 equal payments at the end of each of the next 7 years. If the lender charges 6% on the balance at the beginning of each year, and the homeowner makes an annual payment of $10,748.10, the homeowner will pay in interest in the first year. Step 2: Learn: Amortization Schedule Amortization schedules are a helpful tool in breaking down your loan payment into its interest and principal repayment components. Suppose Rajiv receives a $27,000.00 loan to be repaid in equal installments at the end of each of the next 3 years. The interest rate is 4% compounded annually. Use the formula for the present value of an ordinary annuity to find this payment amount: PVAN PMT = PMT x PVAN X (1+1)N I I 1. In this case, PVAN equals (1+1)N , I equals and N equals Using the formula for the present value of an ordinary annuity, the annual payment amount for this loan is Because this payment is fixed over time, enter this annual payment amount in the "Payment" column of the following table for all three years. Each payment consists of two parts-interest and repayment of principal. You can calculate the interest in year 1 by multiplying the loan balance at the beginning of the year (PVAN) by the interest rate (I). The repayment of principal is equal to the payment (PMT) minus the interest charge for the year: Ch 05- Video Lesson - Time Value of Money Each payment consists of two parts-interest and repayment of principal. You can calculate the interest in year 1 by multiplying the loan balance at the beginning of the year (PVAN) by the interest rate (I). The repayment of principal is equal to the payment (PMT) minus the interest charge for the year: The interest paid in year 1 is Enter the values for interest and repayment of principal for year 1 in the following table. Because the balance at the end of the first year is equal to the beginning amount minus the repayment of principal, the ending balance for year 1 . This is ▼ the beginning amount for year 2. is Enter the ending balance for year 1 and the beginning amount for year 2 in the following table. Using the same process as you did for year 1, complete the following amortization table by filling in the remaining values for years 2 and 3. Repayment of Principal Year Beginning Amount 1 2 3 $27,000.00 Payment Interest Ending Balance $0.00 Complete the following table by determining the percentage of each payment that represents interest and the percentage that represents principal for each of the three years. Payment Component Interest Repayment of Principal Percentage of Payment Year 1 Year 2 Year 3 Step 3: Practice: Amortization Schedule Now it's time for you to practice what you've learned. Suppose Simone receives a $40,000.00 loan to be repaid in equal installments at the end of each of the next 3 years. The interest rate is 8% compounded annually. Complete the following amortization schedule by calculating the payment, interest, repayment of principal, and ending balance for each year. Year Beginning Amount Repayment of Principal Ending Balance 1 2 3 $40,000.00 Payment Interest $0.00 Complete the following table by determining the percentage of each payment that represents interest and the percentage that represents principal for each of the three years. Payment Component Interest Repayment of Principal Percentage of Payment Year 1 Year 2 Year 3 Ž = An amortized loan is a loan that is to be repaid in equal amounts on a monthly, quarterly, or annual basis. Many loans such as car loans, home mortgage loans, and student loans are paid off over time in regular, fixed installments; these loans are a great real-world application of compound interest. For example, suppose a homeowner borrows $100,000 on a mortgage loan, and the loan is to be repaid in 5 equal payments at the end of each of the next 5 years. If the lender charges 6% on the balance at the beginning of each year, what is the payment the homeowner must make each year? Given what you know about present value (PV) and future value (FV), you can deduce that the sum of the PV of each payment the homeowner makes must add up to $100,000: $100,000 = 1.06¹ PMT PMT PMT + + 1.062 1.063 5 PMT Σ 1.06² t=1 + PMT 1.064 + PMT 1.06 What is an amortization schedule? You can use the formula for the present value of an ordinary annuity to find this payment amount: PVAN $100,000 PMT PMT X PMT X $23,739.64 Interest in Year 1 Each payment of $23,739.64 consists of two parts-interest and repayment of principal. An amortization schedule shows this breakdown over time. You can calculate the interest in each period by multiplying the loan balance at the beginning of the year by the interest rate: = (1+1)N I = (1+0.06) 0.06 Loan Balance at the Beginning of Year 1 x Interest Rate $100,000 x 0.06 $6,000 Notice that the interest portion is relatively high in the first year, but then it declines as the loan balance decreases. The repayment of principal is equal to the payment minus the interest charge for the year: Notice that the interest portion is relatively high in the first year, but then it declines as the loan balance decreases. The repayment of principal is equal to the payment minus the interest charge for the year: Repayment of Principal in Year 1 = Payment Interest in Year 1 = $23,739.64 - $6,000 = $17,739.64 You can perform similar calculations to fill in the remainder of the amortization schedule. Year 1 2 3 4 5 Beginning Amount Payment Interest $23,739.64 $6,000.00 23,739.64 4,935.62 23,739.64 3,807.38 23,739.64 2,611.44 23,739.64 1,343.75 $100,000.00 82,260.36 63,456.34 43,524.08 22,395.89 Repayment of Principal $17,739.64 18,804.02 19,932.26 21,128.20 22,395.89 Ending Balance $82,260.36 63,456.34 43,524.08 22,395.89 0.00 Suppose Rajiv borrows $60,000.00 on a mortgage loan, and the loan is to be repaid in 7 equal payments at the end of each of the next 7 years. If the lender charges 6% on the balance at the beginning of each year, and the homeowner makes an annual payment of $10,748.10, the homeowner will pay in interest in the first year. Step 2: Learn: Amortization Schedule Amortization schedules are a helpful tool in breaking down your loan payment into its interest and principal repayment components. Suppose Rajiv receives a $27,000.00 loan to be repaid in equal installments at the end of each of the next 3 years. The interest rate is 4% compounded annually. Use the formula for the present value of an ordinary annuity to find this payment amount: PVAN PMT = PMT x PVAN X (1+1)N I I 1. In this case, PVAN equals (1+1)N , I equals and N equals Using the formula for the present value of an ordinary annuity, the annual payment amount for this loan is Because this payment is fixed over time, enter this annual payment amount in the "Payment" column of the following table for all three years. Each payment consists of two parts-interest and repayment of principal. You can calculate the interest in year 1 by multiplying the loan balance at the beginning of the year (PVAN) by the interest rate (I). The repayment of principal is equal to the payment (PMT) minus the interest charge for the year: Ch 05- Video Lesson - Time Value of Money Each payment consists of two parts-interest and repayment of principal. You can calculate the interest in year 1 by multiplying the loan balance at the beginning of the year (PVAN) by the interest rate (I). The repayment of principal is equal to the payment (PMT) minus the interest charge for the year: The interest paid in year 1 is Enter the values for interest and repayment of principal for year 1 in the following table. Because the balance at the end of the first year is equal to the beginning amount minus the repayment of principal, the ending balance for year 1 . This is ▼ the beginning amount for year 2. is Enter the ending balance for year 1 and the beginning amount for year 2 in the following table. Using the same process as you did for year 1, complete the following amortization table by filling in the remaining values for years 2 and 3. Repayment of Principal Year Beginning Amount 1 2 3 $27,000.00 Payment Interest Ending Balance $0.00 Complete the following table by determining the percentage of each payment that represents interest and the percentage that represents principal for each of the three years. Payment Component Interest Repayment of Principal Percentage of Payment Year 1 Year 2 Year 3 Step 3: Practice: Amortization Schedule Now it's time for you to practice what you've learned. Suppose Simone receives a $40,000.00 loan to be repaid in equal installments at the end of each of the next 3 years. The interest rate is 8% compounded annually. Complete the following amortization schedule by calculating the payment, interest, repayment of principal, and ending balance for each year. Year Beginning Amount Repayment of Principal Ending Balance 1 2 3 $40,000.00 Payment Interest $0.00 Complete the following table by determining the percentage of each payment that represents interest and the percentage that represents principal for each of the three years. Payment Component Interest Repayment of Principal Percentage of Payment Year 1 Year 2 Year 3 Ž =

Expert Answer:

Answer rating: 100% (QA)

An amortization schedule is a table that shows how a loan will be repaid over time including the amount of each payment the amount of interest paid an... View the full answer

Related Book For

Income Tax Fundamentals 2013

ISBN: 9781285586618

31st Edition

Authors: Gerald E. Whittenburg, Martha Altus Buller, Steven L Gill

Posted Date:

Students also viewed these accounting questions

-

A claim is a contested change where the buyer and the seller cannot reach an agreement on compensation for the change or cannot agree that a change has occurred. Explain

-

A small rubber ball is launched by a compressed - air cannon from ground level with an initial speed of 1 2 . 4 1 2 . 4 m / / s directly upward. Choose upward as the positive direction in your...

-

Genevieve Shannara has always wanted to open her own kennel and grooming services; she had been grooming pets for friends and family from her apartment for extra cash since high school. When the...

-

In Problems 1316, find each sum. 10 (-2)* k=1

-

Refer to Table 13-1. a. On June 4, 2012, you purchased a British pound-denominated CD by converting $1 million to pounds at a rate of 0.6435 pounds for U.S. dollars. It is now July 4, 2012. Has the...

-

Recall the Project Management Simulation, how to set up priority in guiding the implementation efforts? What is the proper way to implement innovation project at both incremental and radical levels?...

-

The details of cost per unit at an activity level of 10,000 units of a product are as follows: Rs Raw materials 10 Direct expenses 8 Labour charges 2 Variable overheads 4 Fixed overheads 6 Total cost...

-

What is the largest percentage fee that a client who currently is lending (y < 1) will be willing to pay to invest in your fund? What about a client who is borrowing (y > 1)? For Challenge Problems...

-

Santos Golf Products is considering whether to upgrade its equipment. Managers are considering two options. Equipment manufactured by Stenback Inc. costs $950,000 and will last six years and have no...

-

Fawcett Institute provides one-on-one training to individuals who pay tuition directly to the business and also offers extension training to groups in off-site locations. Fawcett prepares adjusting...

-

Transcribed image text: Natalie's Nail Salon has 2 locations: Natalie's Downtown, and Natalie's By-the-Beach. The two salons combined performed 314 pedicures in the first quarter of 2011, and 395...

-

I have attached a case study, primarily based on your textbook chapter reading assignments. The background material for the case also references chapters 3 and 15, not assigned for this course....

-

On December 1 , 2 0 2 5 , Sandhill Distributing Company had the following account balances.DebitCash$ 7 , 1 0 0 Accounts Receivable 4 , 5 0 0 Inventory 1 1 , 9 0 0 Supplies 1 , 2 0 0 Equipment 2 2 ,...

-

Cindy Greene works at Georgia Mountain Hospital. The hospital experiences a lot of business closer to summer when the temperature is warmer. Cindy is meeting with her supervisor to go over the budget...

-

Use z scores to compare the given values. Based on sample data, newborn males have weights with a mean of 3247.4 g and a standard deviation of 575.4 g. Newborn females have weights with a mean of...

-

Gignment FULL SCAL Exercise 4- The following ndependent situations require professional judgment for determining when to recognize revenue from the transactions. Identify when revenue should be...

-

Explain how financial institutions price risk. Explain the dilemma they face in pricing risk. Explain the role that pricing risk plays in institutions' strategic decisions. In your explanation, cite...

-

Big Jim Company sponsored a picnic for employees and purchased a propane grill equipped with a standard-sized propane tank for the picnic. To make sure there was enough propane for all the cooking...

-

For each of the following situations, indicate whether the taxpayer(s) is (are) required to file a tax return for 2012. Explain your answer. a. Helen is a single taxpayer with interest income in 2012...

-

a. Wilson filed his individual tax return on the original due date, but failed to pay $700 in taxes that were due with the return. If Wilson pays the taxes exactly 2 months late, calculate the amount...

-

The following additional information is available for the Dr. Ivan and Irene Incisor family from Chapters 1-6. On December 12, Irene purchased the building where her store is located. She paid...

-

The International Licensing Industry Merchandisers Association (LIMA; www.licensing.org) is an organization with offices worldwide. It supports merchandise licensing through education, networking,...

-

Suppose you are an international entrepreneur and want to open your own franchise somewhere in Europe. You decide to conduct research to identify the most promising franchise and learn how to become...

-

What are the advantages and disadvantages of licensing? LO.1

Study smarter with the SolutionInn App