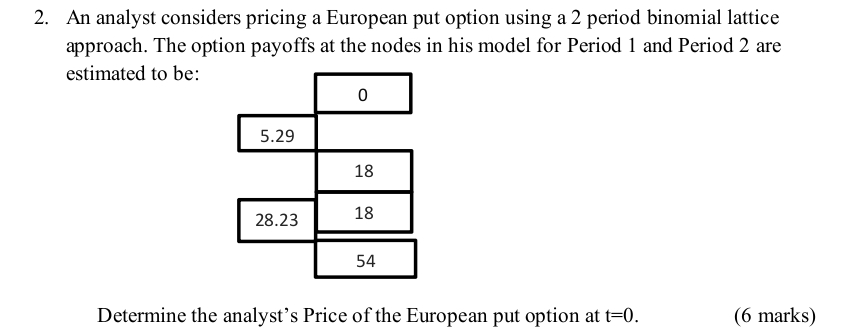

Question: An analyst considers pricing a European put option using a 2 period binomial lattice approach. The option payoffs at the nodes in his model for

An analyst considers pricing a European put option using a period binomial lattice approach. The option payoffs at the nodes in his model for Period and Period are estimated to be:

table

Determine the analyst's Price of the European put option at

marks

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock