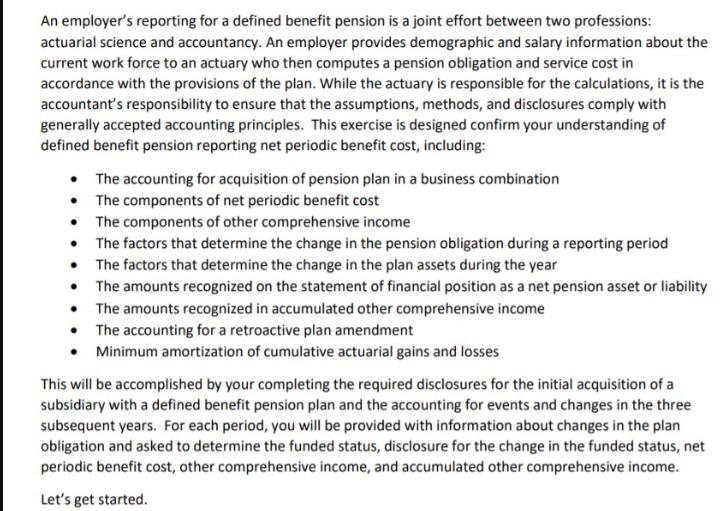

An employer's reporting for a defined benefit pension is a joint effort between two professions: actuarial...

Fantastic news! We've Found the answer you've been seeking!

Question:

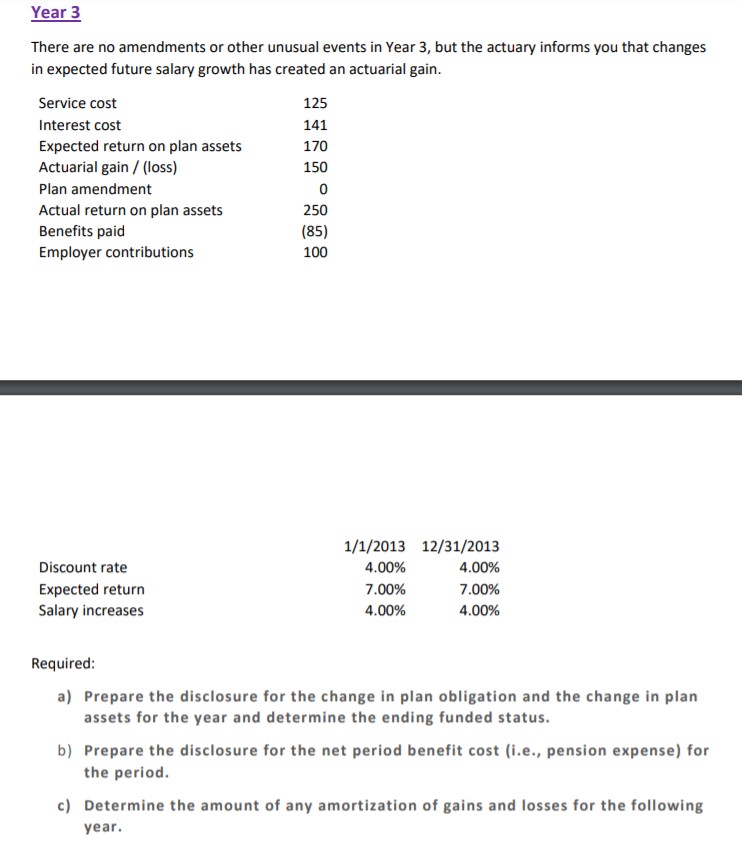

Transcribed Image Text:

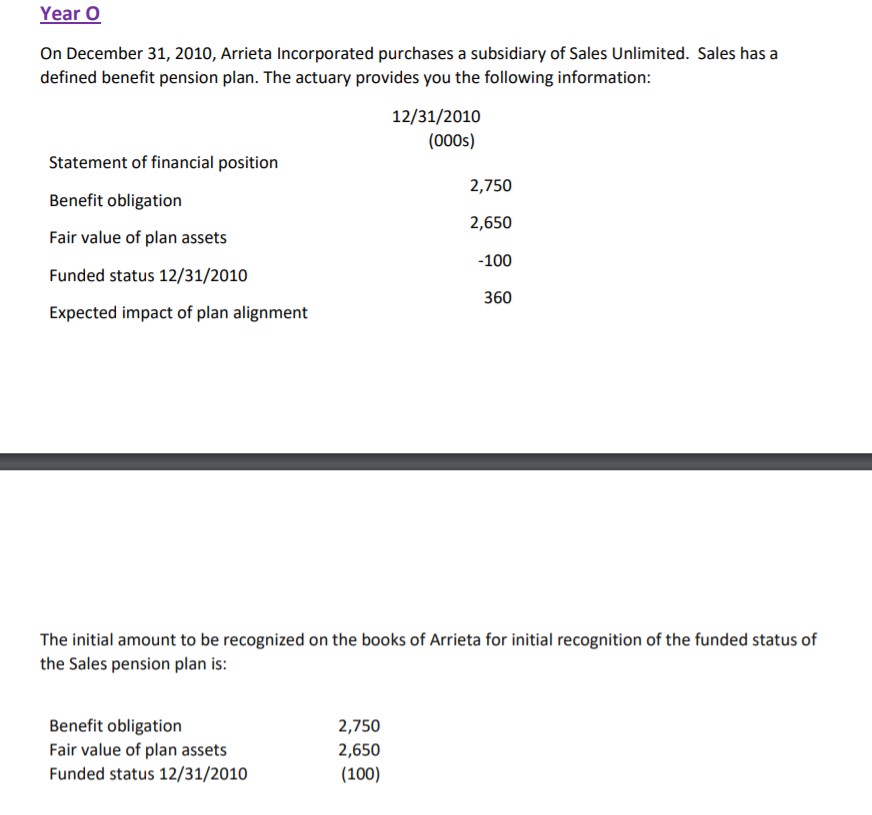

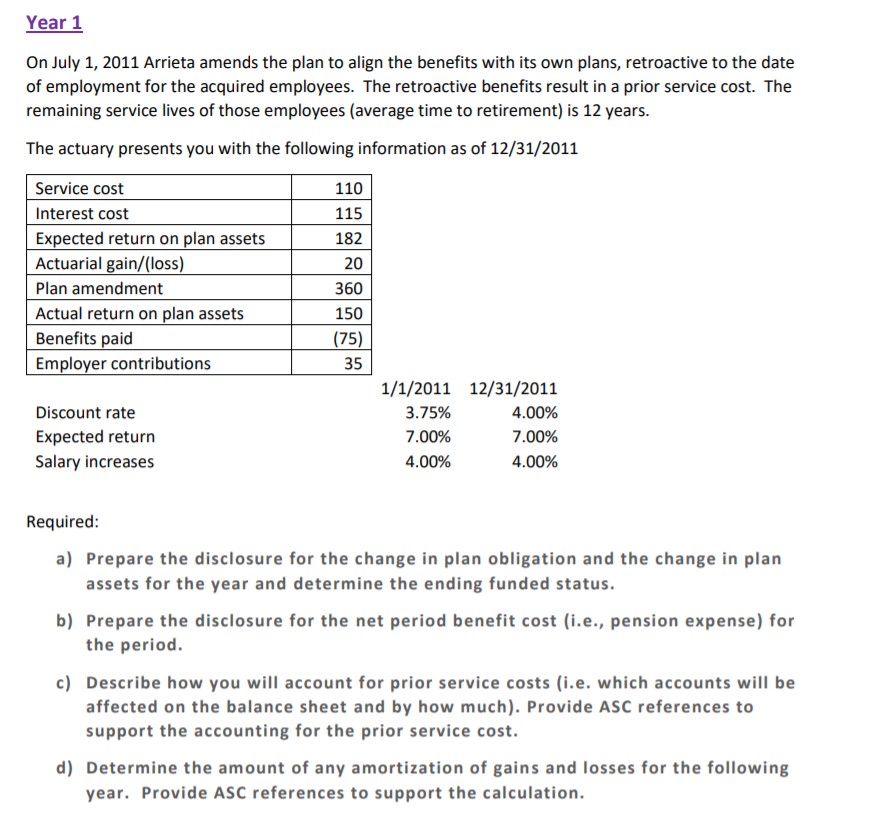

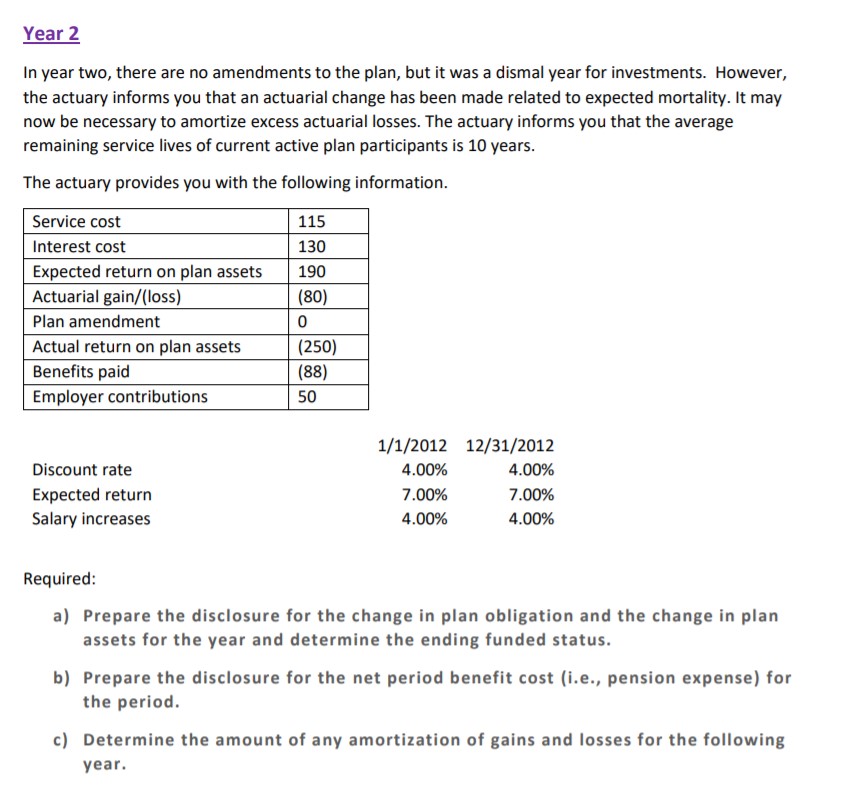

An employer's reporting for a defined benefit pension is a joint effort between two professions: actuarial science and accountancy. An employer provides demographic and salary information about the current work force to an actuary who then computes a pension obligation and service cost in accordance with the provisions of the plan. While the actuary is responsible for the calculations, it is the accountant's responsibility to ensure that the assumptions, methods, and disclosures comply with generally accepted accounting principles. This exercise is designed confirm your understanding of defined benefit pension reporting net periodic benefit cost, including: The accounting for acquisition of pension plan in a business combination The components of net periodic benefit cost The components of other comprehensive income The factors that determine the change in the pension obligation during a reporting period The factors that determine the change in the plan assets during the year The amounts recognized on the statement of financial position as a net pension asset or liability The amounts recognized in accumulated other comprehensive income The accounting for a retroactive plan amendment Minimum amortization of cumulative actuarial gains and losses This will be accomplished by your completing the required disclosures for the initial acquisition of a subsidiary with a defined benefit pension plan and the accounting for events and changes in the three subsequent years. For each period, you will be provided with information about changes in the plan obligation and asked to determine the funded status, disclosure for the change in the funded status, net periodic benefit cost, other comprehensive income, and accumulated other comprehensive income. Let's get started. Year O On December 31, 2010, Arrieta Incorporated purchases a subsidiary of Sales Unlimited. Sales has a defined benefit pension plan. The actuary provides you the following information: Statement of financial position Benefit obligation Fair value of plan assets Funded status 12/31/2010 Expected impact of plan alignment 12/31/2010 (000s) 2,750 2,650 -100 360 The initial amount to be recognized on the books of Arrieta for initial recognition of the funded status of the Sales pension plan is: Benefit obligation 2,750 Fair value of plan assets 2,650 Funded status 12/31/2010 (100) Year 1 On July 1, 2011 Arrieta amends the plan to align the benefits with its own plans, retroactive to the date of employment for the acquired employees. The retroactive benefits result in a prior service cost. The remaining service lives of those employees (average time to retirement) is 12 years. The actuary presents you with the following information as of 12/31/2011 Service cost 110 Interest cost 115 Expected return on plan assets 182 Actuarial gain/(loss) 20 Plan amendment 360 Actual return on plan assets 150 Benefits paid (75) Employer contributions 35 1/1/2011 12/31/2011 Discount rate 3.75% 4.00% Expected return 7.00% 7.00% Salary increases 4.00% 4.00% Required: a) Prepare the disclosure for the change in plan obligation and the change in plan assets for the year and determine the ending funded status. b) Prepare the disclosure for the net period benefit cost (i.e., pension expense) for the period. c) Describe how you will account for prior service costs (i.e. which accounts will be affected on the balance sheet and by how much). Provide ASC references to support the accounting for the prior service cost. d) Determine the amount of any amortization of gains and losses for the following year. Provide ASC references to support the calculation. Year 2 In year two, there are no amendments to the plan, but it was a dismal year for investments. However, the actuary informs you that an actuarial change has been made related to expected mortality. It may now be necessary to amortize excess actuarial losses. The actuary informs you that the average remaining service lives of current active plan participants is 10 years. The actuary provides you with the following information. Service cost 115 Interest cost 130 Expected return on plan assets 190 Actuarial gain/(loss) (80) Plan amendment 0 Actual return on plan assets (250) Benefits paid Employer contributions (88) 50 Discount rate Expected return 1/1/2012 12/31/2012 4.00% 4.00% 7.00% 7.00% 4.00% 4.00% Salary increases Required: a) Prepare the disclosure for the change in plan obligation and the change in plan assets for the year and determine the ending funded status. b) Prepare the disclosure for the net period benefit cost (i.e., pension expense) for the period. c) Determine the amount of any amortization of gains and losses for the following year. Year 3 There are no amendments or other unusual events in Year 3, but the actuary informs you that changes in expected future salary growth has created an actuarial gain. Service cost 125 Interest cost 141 Expected return on plan assets 170 Actuarial gain/(loss) 150 Plan amendment 0 Actual return on plan assets 250 Benefits paid Employer contributions (85) 100 1/1/2013 12/31/2013 Discount rate Expected return 4.00% 4.00% 7.00% 7.00% Salary increases 4.00% 4.00% Required: a) Prepare the disclosure for the change in plan obligation and the change in plan assets for the year and determine the ending funded status. b) Prepare the disclosure for the net period benefit cost (i.e., pension expense) for the period. c) Determine the amount of any amortization of gains and losses for the following year. An employer's reporting for a defined benefit pension is a joint effort between two professions: actuarial science and accountancy. An employer provides demographic and salary information about the current work force to an actuary who then computes a pension obligation and service cost in accordance with the provisions of the plan. While the actuary is responsible for the calculations, it is the accountant's responsibility to ensure that the assumptions, methods, and disclosures comply with generally accepted accounting principles. This exercise is designed confirm your understanding of defined benefit pension reporting net periodic benefit cost, including: The accounting for acquisition of pension plan in a business combination The components of net periodic benefit cost The components of other comprehensive income The factors that determine the change in the pension obligation during a reporting period The factors that determine the change in the plan assets during the year The amounts recognized on the statement of financial position as a net pension asset or liability The amounts recognized in accumulated other comprehensive income The accounting for a retroactive plan amendment Minimum amortization of cumulative actuarial gains and losses This will be accomplished by your completing the required disclosures for the initial acquisition of a subsidiary with a defined benefit pension plan and the accounting for events and changes in the three subsequent years. For each period, you will be provided with information about changes in the plan obligation and asked to determine the funded status, disclosure for the change in the funded status, net periodic benefit cost, other comprehensive income, and accumulated other comprehensive income. Let's get started. Year O On December 31, 2010, Arrieta Incorporated purchases a subsidiary of Sales Unlimited. Sales has a defined benefit pension plan. The actuary provides you the following information: Statement of financial position Benefit obligation Fair value of plan assets Funded status 12/31/2010 Expected impact of plan alignment 12/31/2010 (000s) 2,750 2,650 -100 360 The initial amount to be recognized on the books of Arrieta for initial recognition of the funded status of the Sales pension plan is: Benefit obligation 2,750 Fair value of plan assets 2,650 Funded status 12/31/2010 (100) Year 1 On July 1, 2011 Arrieta amends the plan to align the benefits with its own plans, retroactive to the date of employment for the acquired employees. The retroactive benefits result in a prior service cost. The remaining service lives of those employees (average time to retirement) is 12 years. The actuary presents you with the following information as of 12/31/2011 Service cost 110 Interest cost 115 Expected return on plan assets 182 Actuarial gain/(loss) 20 Plan amendment 360 Actual return on plan assets 150 Benefits paid (75) Employer contributions 35 1/1/2011 12/31/2011 Discount rate 3.75% 4.00% Expected return 7.00% 7.00% Salary increases 4.00% 4.00% Required: a) Prepare the disclosure for the change in plan obligation and the change in plan assets for the year and determine the ending funded status. b) Prepare the disclosure for the net period benefit cost (i.e., pension expense) for the period. c) Describe how you will account for prior service costs (i.e. which accounts will be affected on the balance sheet and by how much). Provide ASC references to support the accounting for the prior service cost. d) Determine the amount of any amortization of gains and losses for the following year. Provide ASC references to support the calculation. Year 2 In year two, there are no amendments to the plan, but it was a dismal year for investments. However, the actuary informs you that an actuarial change has been made related to expected mortality. It may now be necessary to amortize excess actuarial losses. The actuary informs you that the average remaining service lives of current active plan participants is 10 years. The actuary provides you with the following information. Service cost 115 Interest cost 130 Expected return on plan assets 190 Actuarial gain/(loss) (80) Plan amendment 0 Actual return on plan assets (250) Benefits paid Employer contributions (88) 50 Discount rate Expected return 1/1/2012 12/31/2012 4.00% 4.00% 7.00% 7.00% 4.00% 4.00% Salary increases Required: a) Prepare the disclosure for the change in plan obligation and the change in plan assets for the year and determine the ending funded status. b) Prepare the disclosure for the net period benefit cost (i.e., pension expense) for the period. c) Determine the amount of any amortization of gains and losses for the following year. Year 3 There are no amendments or other unusual events in Year 3, but the actuary informs you that changes in expected future salary growth has created an actuarial gain. Service cost 125 Interest cost 141 Expected return on plan assets 170 Actuarial gain/(loss) 150 Plan amendment 0 Actual return on plan assets 250 Benefits paid Employer contributions (85) 100 1/1/2013 12/31/2013 Discount rate Expected return 4.00% 4.00% 7.00% 7.00% Salary increases 4.00% 4.00% Required: a) Prepare the disclosure for the change in plan obligation and the change in plan assets for the year and determine the ending funded status. b) Prepare the disclosure for the net period benefit cost (i.e., pension expense) for the period. c) Determine the amount of any amortization of gains and losses for the following year.

Expert Answer:

Related Book For

Intermediate Accounting

ISBN: 978-0077400163

6th edition

Authors: J. David Spiceland, James Sepe, Mark Nelson

Posted Date:

Students also viewed these accounting questions

-

An employer s reporting for a defined benefit pension is a joint effort between two professions: actuarial science and accountancy. An employer provides demographic and salary information about the...

-

Video and Image data With the ubiquity of video and image capture devices, visual data are more prevalent than ever. The use of these data to augment accounting records is quickly becoming a reality...

-

A company has the following results for the three years to 31 October 2020: Assuming that all possible claims are made to relieve the trading loss against total profits, calculate the company's...

-

This problem utilizes information from Problem 10- 9 and requires that the LBO valuation model be constructed. Randy was happy with the anticipated results from the acquisition of Flanders Inc., but...

-

Lessor Leasing Company agrees to provide Lessee Company with equipment under a non-cancelable lease for five years. The equipment has a five-year life, cost Lessor Company $30,000, and will have no...

-

An F-test with 5 degrees of freedom in the numerator and 7 degrees of freedom in the denominator produced a test statistic whose value was 5.31. The null and alternate hypotheses were H0: 1 = 2...

-

On January 1, the company issued 10-year bonds with a face value of $200,000. The bonds carry a coupon rate of 10%, and interest is paid semiannually. On the issue date, the market interest rate for...

-

A 55kg bicyclist (including the bicycle), initially at rest, pedals to the right, causing her speed to increase steadily for 6.9s. During this time she travels 34m while experiences a 60N drag and...

-

How does the theory of intersectionality, as proposed by Kimberl Crenshaw, challenge traditional sociological perspectives on race, gender, and class, and what implications does this have for...

-

Given a Stream, which method would you use to obtain an equivalent parallel Stream? A. getParallelStream() B. parallelStream() C. parallel() D. getParallel() E. parallels() F. None of the above

-

The following diagrams represent the order of read/write operations of two threads sharing a common variable. Each thread first reads the value of the variable from memory and then writes a new value...

-

Fill in the blank with the functional interface from java.util.function that allows the code to compile and print 3 at runtime. _____________ transformer = x -> x; A. Function B. UnaryOperator C....

-

What is the expected result of calling deleteTree() on a directory? Assume the directory exists and is able to be modified. A. It will delete the directory itself only. B. It will delete the...

-

Fill in the blanks: ______________ is a special case of ______________, in which two or more active threads try to acquire the same set of locks and are repeatedly unsuccessful. A. Deadlock, livelock...

-

Choose one of the topics below, do some additional outside reading, and write a paper on the barriers that exist when accessing oral health care for the population you choose. Focus on what issues...

Study smarter with the SolutionInn App