An enduring controversy within financial theory concerns the effect of financial leverage on the value and stock

Question:

An enduring controversy within financial theory concerns the effect of financial leverage on the value and stock price of a company. Can a company affect its overall value by selecting an optimal financing mix (debt and equity)? The firm's mix of debt and equity financing is called its capital structure. The essentials of the capital structure and the effect of financial policies on the value of the firm were pioneering work of Noble recipients Modigliani and Miller in 1958 and 1963.1

The essential question is: Does debt financing create value?If so, how? If not, then why do so many financial mangers try to find the combination of securities that has greatest overall effect on the market value of the firm?

This short case presents a simple model of Modigliani-Miller theorem to highlight the advantage of debt financing and whether there is an optimal capital structure that maximizes the value of the firm. However, it ignores other market imperfections such as bankruptcy and agency problems among security holders that would affect the value of the firm.

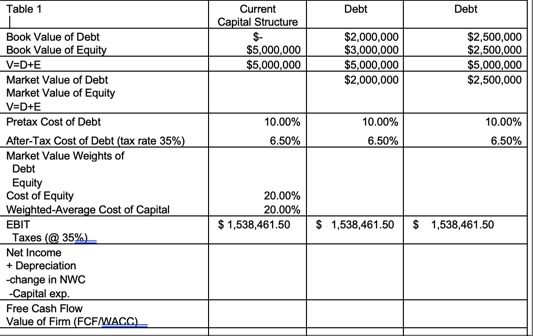

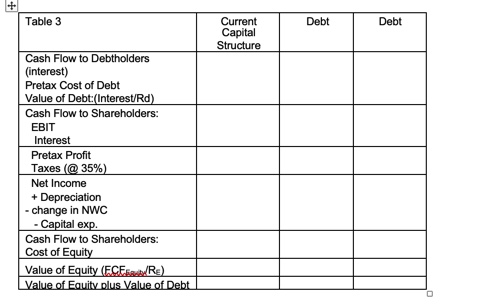

Radstone, Inc., a prominent stone fabrication firm was formed 5 years ago to exploit a new continuous fabrication process. Radstone's founders, Jim Rad and Mick Rad, had been employed in the research department of a major integrated-stone fabrication company, but when that company decided against using the new process, they decided to strike out on their own.One advantage of the new process was that it required relatively little capital in comparison with the typical fabrication company, so they have been able to avoid issuing debt financing, and thus they own all of the shares.However, the company has now reached the stage where outside capital is necessary if the firm is to achieve its growth targets. Therefore, they have decided to leverage the company with swapping some of their shares with new debt.

Currently the company has value of $5 million with outstanding shares of 100,000. The company generates $1,538,461.5 in earnings before interest and taxes (EBIT[EJHN1]) in perpetuity. The corporate tax rate is 35 percent and all earnings are paid as dividends. The company is considering the effect of $2 million and $2.5 million debt -equity swap on its cost of capital and its value. The cost of debt is 10 percent and the cost of capital is currently 20 percent. Any investment in net working capital and capital expenditure is equal to its depreciation allowances. The corporate tax rate is 35 percent.

[EJHN1]an amount of moneybefore tax isthe amount that you earn or receivebeforeyou have paidtaxon it.

Expert Answer:

The ModiglianiMiller theorem suggests that under certain assumptions the capital structure mix of de... View the full answer

Statistics For Business And Economics

ISBN: 9780132745659

8th Edition

Authors: Paul Newbold, William Carlson, Betty Thorne