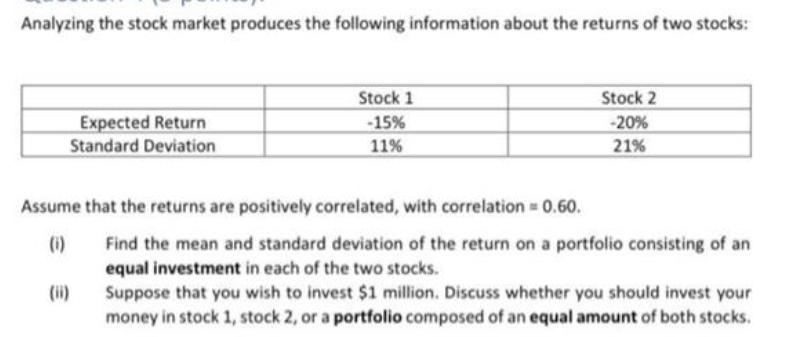

Analyzing the stock market produces the following information about the returns of two stocks: Expected Return...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

i Mean and Standard Deviation of the Portfolio Mean The mean return of the portfolio is calculated b... View the full answer

Related Book For

Fundamentals of Financial Management

ISBN: 978-1305635937

Concise 9th Edition

Authors: Eugene F. Brigham

Posted Date: