Question: Andrew is considering dividing his portfolio between two assets, a risky asset that has an expected return of 35% and a standard deviation of 0.15

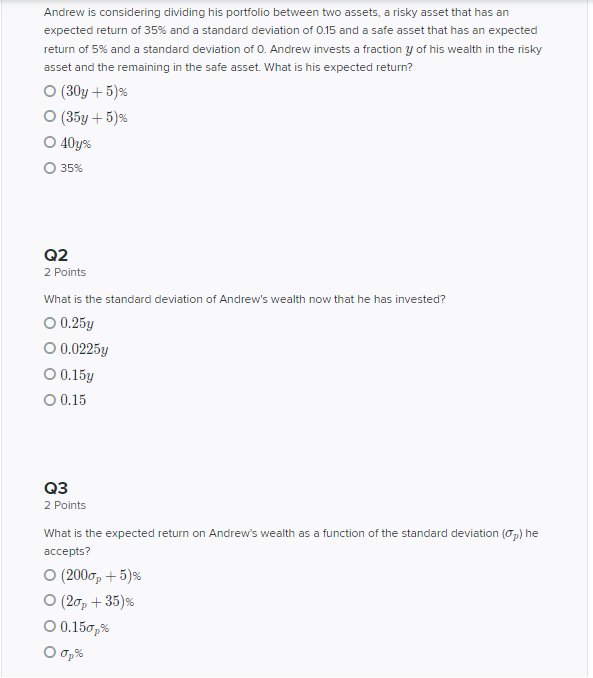

Andrew is considering dividing his portfolio between two assets, a risky asset that has an expected return of 35% and a standard deviation of 0.15 and a safe asset that has an expected return of 5% and a standard deviation of O. Andrew invests a fraction y of his wealth in the risky asset and the remaining in the safe asset. What is his expected return? (30y + 5)% O (35y +5)% O 40y% 35% Q2 2 Points What is the standard deviation of Andrew's wealth now that he has invested? O 0.25y O 0.0225y O 0.15y O 0.15 Q3 2 Points What is the expected return on Andrew's wealth as a function of the standard deviation (p) he accepts? (2000p+5)% O (20p +35)% O 0.150 %

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts