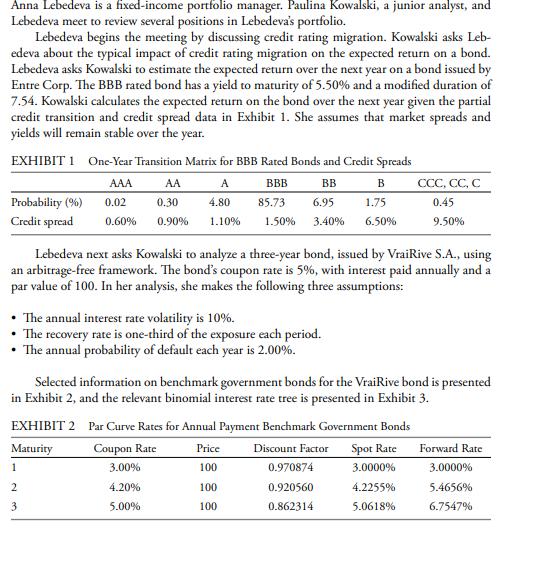

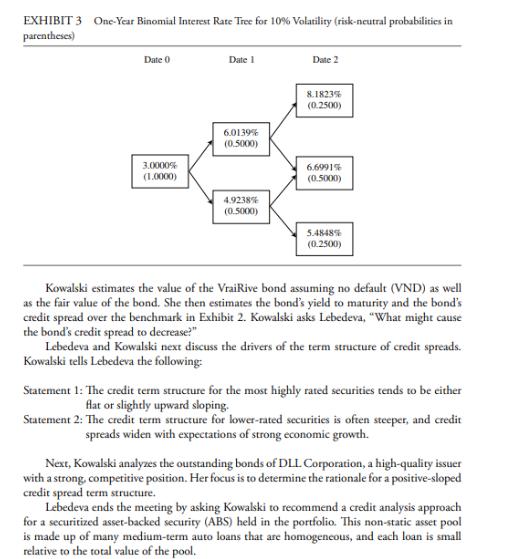

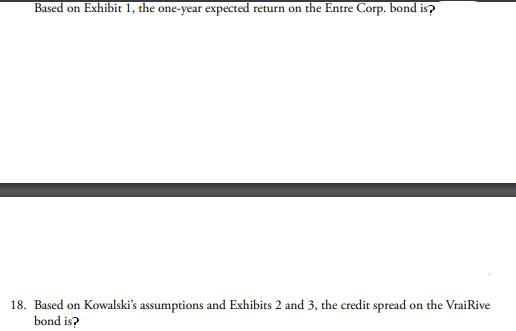

Anna Lebedeva is a fixed-income portfolio manager. Paulina Kowalski, a junior analyst, and Lebedeva meet to...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

To answer the questions provided Question regarding the oneyear expected return on the Entre Corp bond Based on Exhibit 1 to calculate the expected return on the Entre Corp bond which is BBB rated we ... View the full answer

Related Book For

Accounting Tools for Business Decision Making

ISBN: 978-1118128169

5th edition

Authors: Paul D. Kimmel, Jerry J. Weygandt, Donald E. Kieso

Posted Date: