Question: answer 15-30 and I will upvote immediately! ASAP PLEASE MULTIPLE CHOICE - Choose the one alternative that best completes the statement or answers the question.

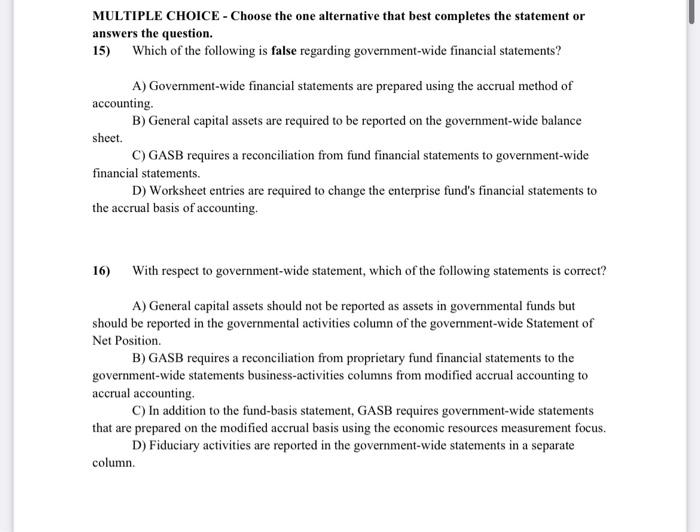

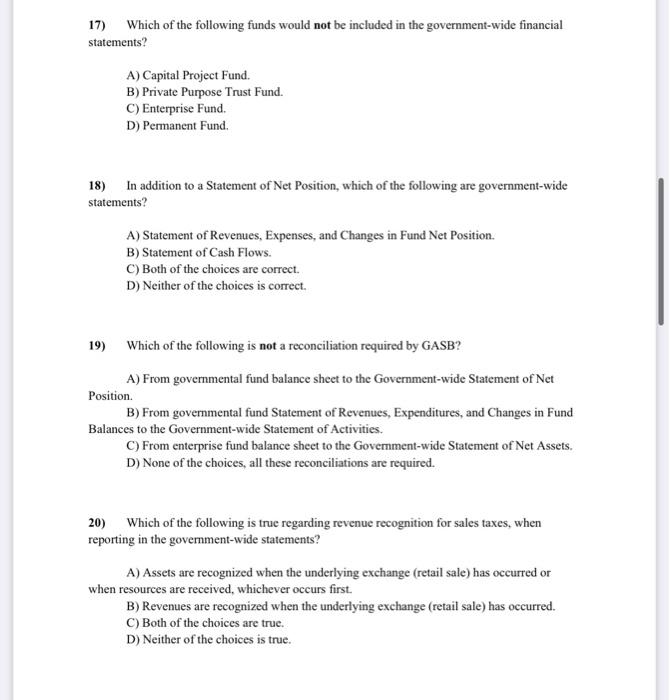

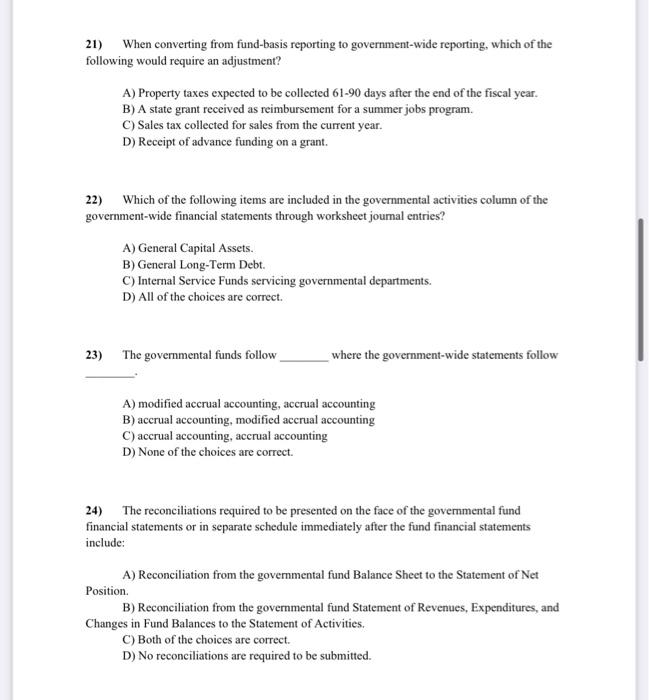

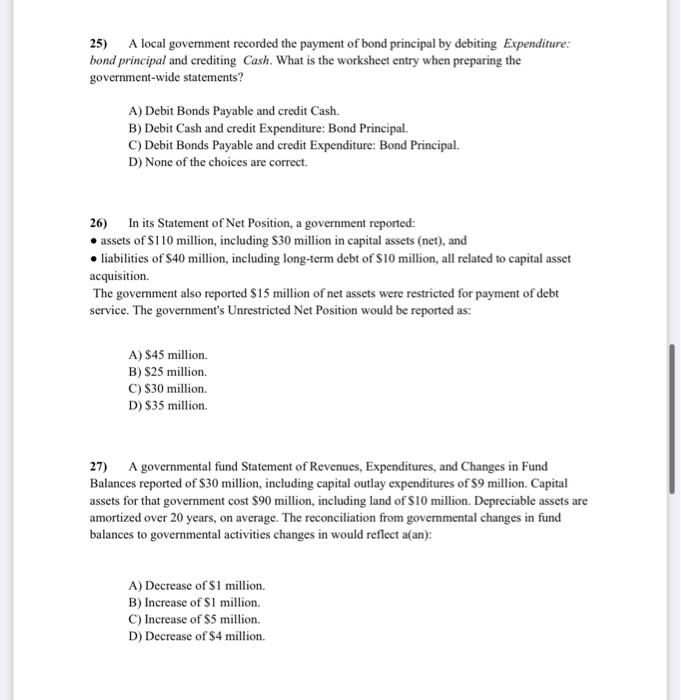

MULTIPLE CHOICE - Choose the one alternative that best completes the statement or answers the question. 15) Which of the following is false regarding government-wide financial statements? A) Government-wide financial statements are prepared using the accrual method of accounting. B) General capital assets are required to be reported on the government-wide balance sheet. C) GASB requires a reconciliation from fund financial statements to government-wide financial statements. D) Worksheet entries are required to change the enterprise fund's financial statements to the accrual basis of accounting. 16) With respect to government-wide statement, which of the following statements is correct? A) General capital assets should not be reported as assets in governmental funds but should be reported in the governmental activities column of the government-wide Statement of Net Position. B) GASB requires a reconciliation from proprietary fund financial statements to the government-wide statements business-activities columns from modified accrual accounting to accrual accounting. C) In addition to the fund-basis statement, GASB requires government-wide statements that are prepared on the modified accrual basis using the economic resources measurement focus. D) Fiduciary activities are reported in the government-wide statements in a separate column. 17) Which of the following funds would not be included in the government-wide financial statements? A) Capital Project Fund. B) Private Purpose Trust Fund. C) Enterprise Fund. D) Permanent Fund. 18) In addition to a Statement of Net Position, which of the following are government-wide statements? A) Statement of Revenues, Expenses, and Changes in Fund Net Position. B) Statement of Cash Flows. C) Both of the choices are correct. D) Neither of the choices is correct. 19) Which of the following is not a reconciliation required by GASB? A) From governmental fund balance sheet to the Government-wide Statement of Net Position. B) From governmental fund Statement of Revenues, Expenditures, and Changes in Fund Balances to the Government-wide Statement of Activities. C) From enterprise fund balance sheet to the Government-wide Statement of Net Assets. D) None of the choices, all these reconciliations are required. 20) Which of the following is true regarding revenue recognition for sales taxes, when reporting in the government-wide statements? A) Assets are recognized when the underlying exchange (retail sale) has occurred or when resources are received, whichever occurs first. B) Revenues are recognized when the underlying exchange (retail sale) has occurred. C) Both of the choices are true. D) Neither of the choices is true. 21) When converting from fund-basis reporting to government-wide reporting, which of the following would require an adjustment? A) Property taxes expected to be collected 61-90 days after the end of the fiscal year. B) A state grant received as reimbursement for a summer jobs program. C) Sales tax collected for sales from the current year. D) Receipt of advance funding on a grant. 22) Which of the following items are included in the governmental activities column of the government-wide financial statements through worksheet journal entries? A) General Capital Assets. B) General Long-Term Debt. C) Internal Service Funds servicing governmental departments. D) All of the choices are correct. 23) The governmental funds follow where the government-wide statements follow A) modified accrual accounting, accrual accounting B) accrual accounting, modified accrual accounting C) accrual accounting, accrual accounting D) None of the choices are correct. 24) The reconciliations required to be presented on the face of the govermmental fund financial statements or in separate schedule immediately after the fund financial statements include: A) Reconciliation from the governmental fund Balance Sheet to the Statement of Net Position. B) Reconciliation from the governmental fund Statement of Revenues, Expenditures, and Changes in Fund Balances to the Statement of Activities. C) Both of the choices are correct. D) No reconciliations are required to be submitted. 25) A local government recorded the payment of bond principal by debiting Expenditure: bond principal and crediting Cash. What is the worksheet entry when preparing the government-wide statements? A) Debit Bonds Payable and credit Cash. B) Debit Cash and credit Expenditure: Bond Principal. C) Debit Bonds Payable and credit Expenditure: Bond Principal. D) None of the choices are correct. 26) In its Statement of Net Position, a government reported: - assets of \$110 million, including \$30 million in capital assets (net), and - liabilities of $40 million, including long-term debt of $10 million, all related to capital asset acquisition. The government also reported $15 million of net assets were restricted for payment of debt service. The government's Unrestricted Net Position would be reported as: A) $45 million. B) $25 million. C) $30 million. D) $35 million. 27) A governmental fund Statement of Revenues, Expenditures, and Changes in Fund Balances reported of $30 million, including capital outlay expenditures of $9 million. Capital assets for that government cost $90 million, including land of $10 million. Depreciable assets are amortized over 20 years, on average. The reconciliation from govemmental changes in fund balances to governmental activities changes in would reflect a(an): A) Decrease of $1 million. B) Increase of $1 million. C) Increase of $5 million. D) Decrease of $4 million. 28) The City of Charlotte reported property tax revenues in 2020 in the amount of $10 million. The deferred inflow-property taxes reported in the General Fund's balance sheet was $300,000 on December 31,2019 and was $375,000 on December 31, 2020. During 2020 , $9,000,000 was collected. What amount should the city report for Property Tax Revenue in its year ended December 31, 2020 government-wide Statement of Activities? A) $9,075,000 B) $9,975,000 C) $10,075,000 D) $10,375,000 29) The City of Eugene reported property tax revenues in 2020 in the amount of $10 million. The deferred inflow- property taxes reported in the General Fund's balance sheet was $475,000 on December 31,2019 and was $400,000 on December 31,2020 . During 2020 , $9,000,000 was collected. What amount should the city report for Property Tax Revenue in its year ended December 31, 2020 government-wide Statement of Activities? A) $10,075,000 B) $9,925,000 C) $9,625,000 D) $8,975,000 30) A government's Statement of Revenues, Expenditures, and Changes in Fund Balances reflected proceeds of bonds in the amount of $2,000,000. That statement also reflected expenditures for debt service in the amount of $3,300,000, including $2,900,000 for principal payments. Assuming no other changes, the effect, when moving from the change in fund balances in the governmental funds Statement of Revenues, Expenditures, and Changes in Fund Balances to the change in Net Position for governmental activities in the Statement of Activities would be a: A) $900,000 increase. B) $900,000 decrease. C) $1,300,000 increase. D) $1,300,000 decrease

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts