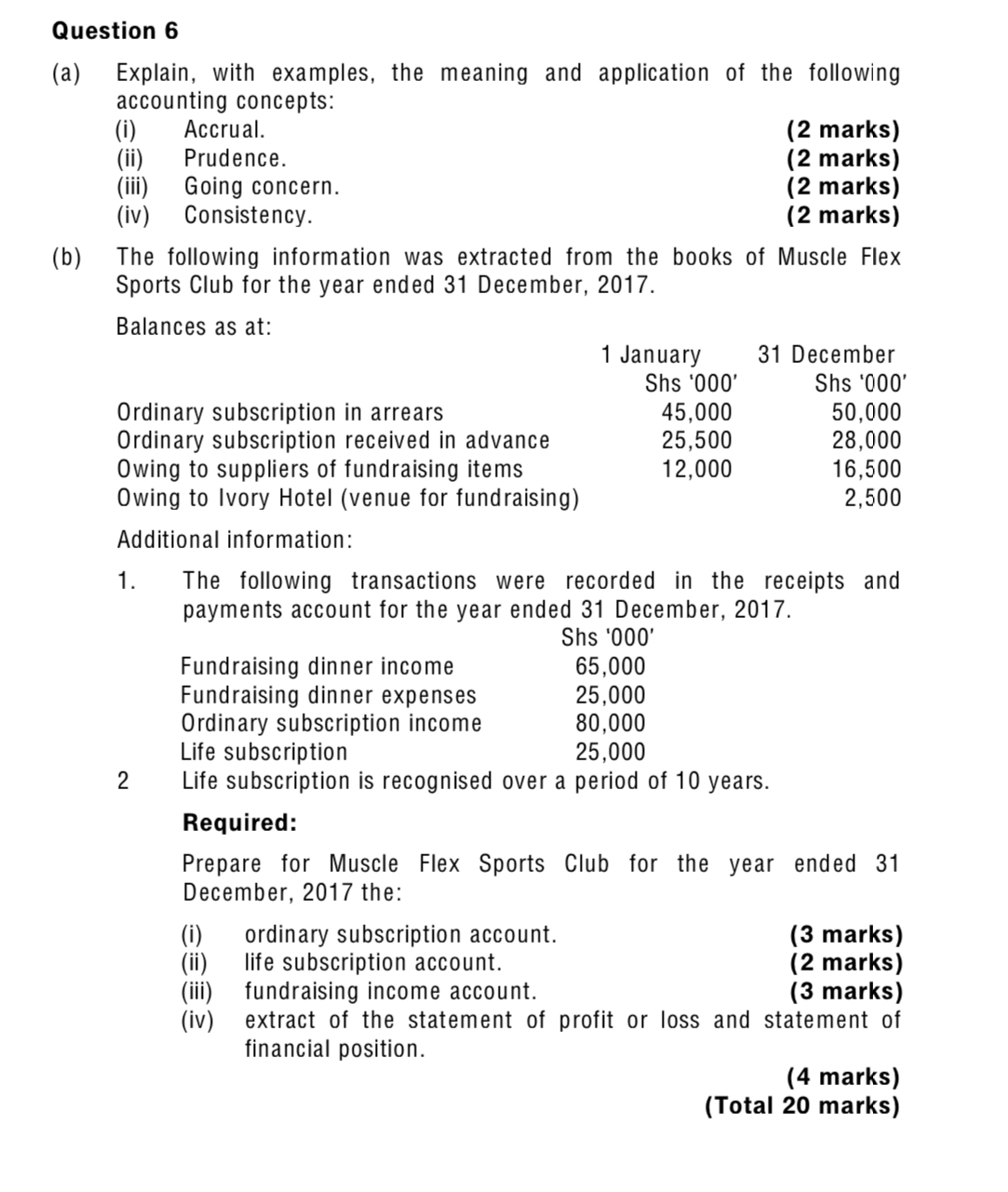

Question: Answer ALL QUESTIONS CORRECTLY Question 6 (a) (b) Explain, with examples. the meaning and application of the following accounting concepts: (i) Accrual. (2 marks) (ii)

Answer ALL QUESTIONS CORRECTLY

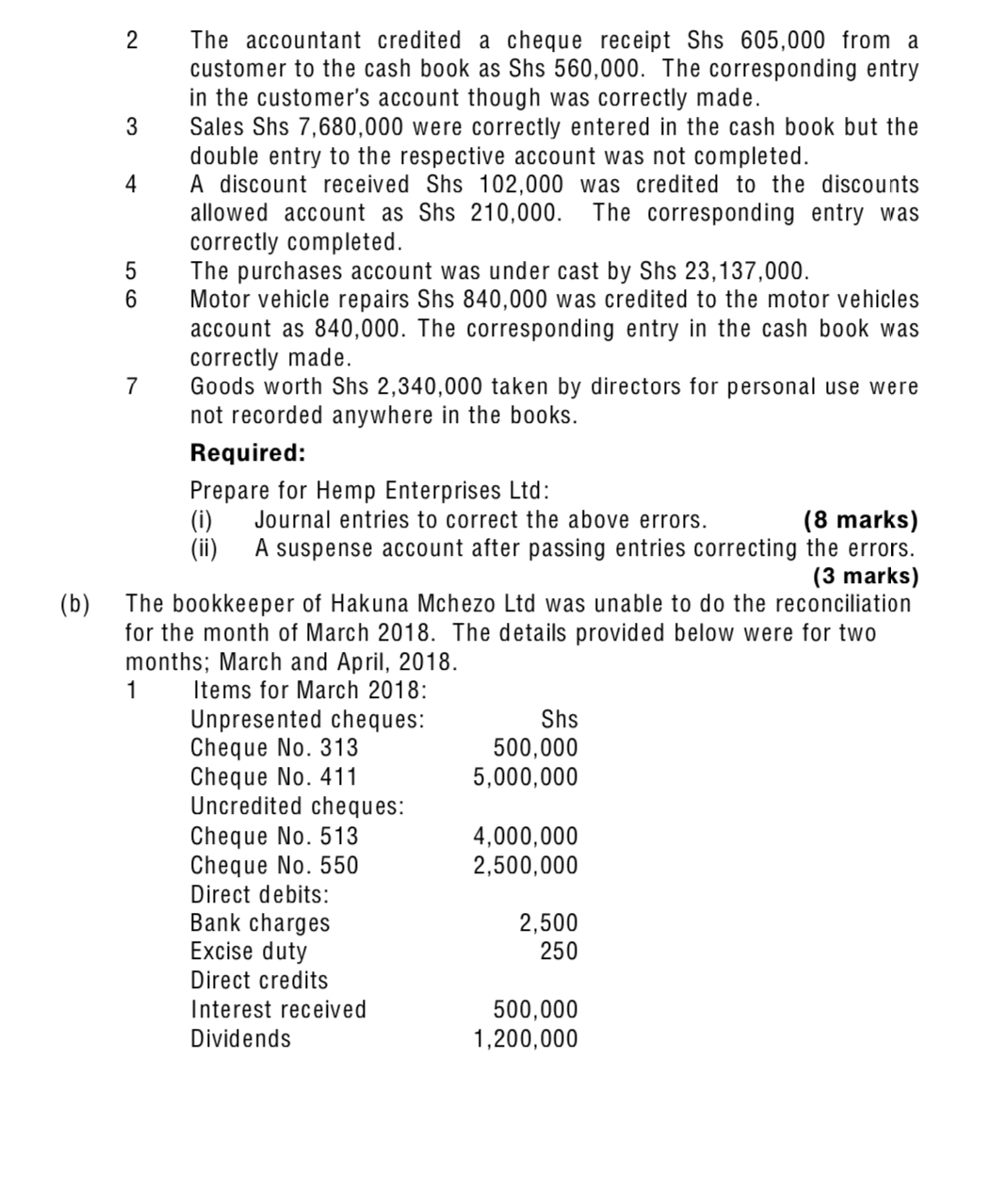

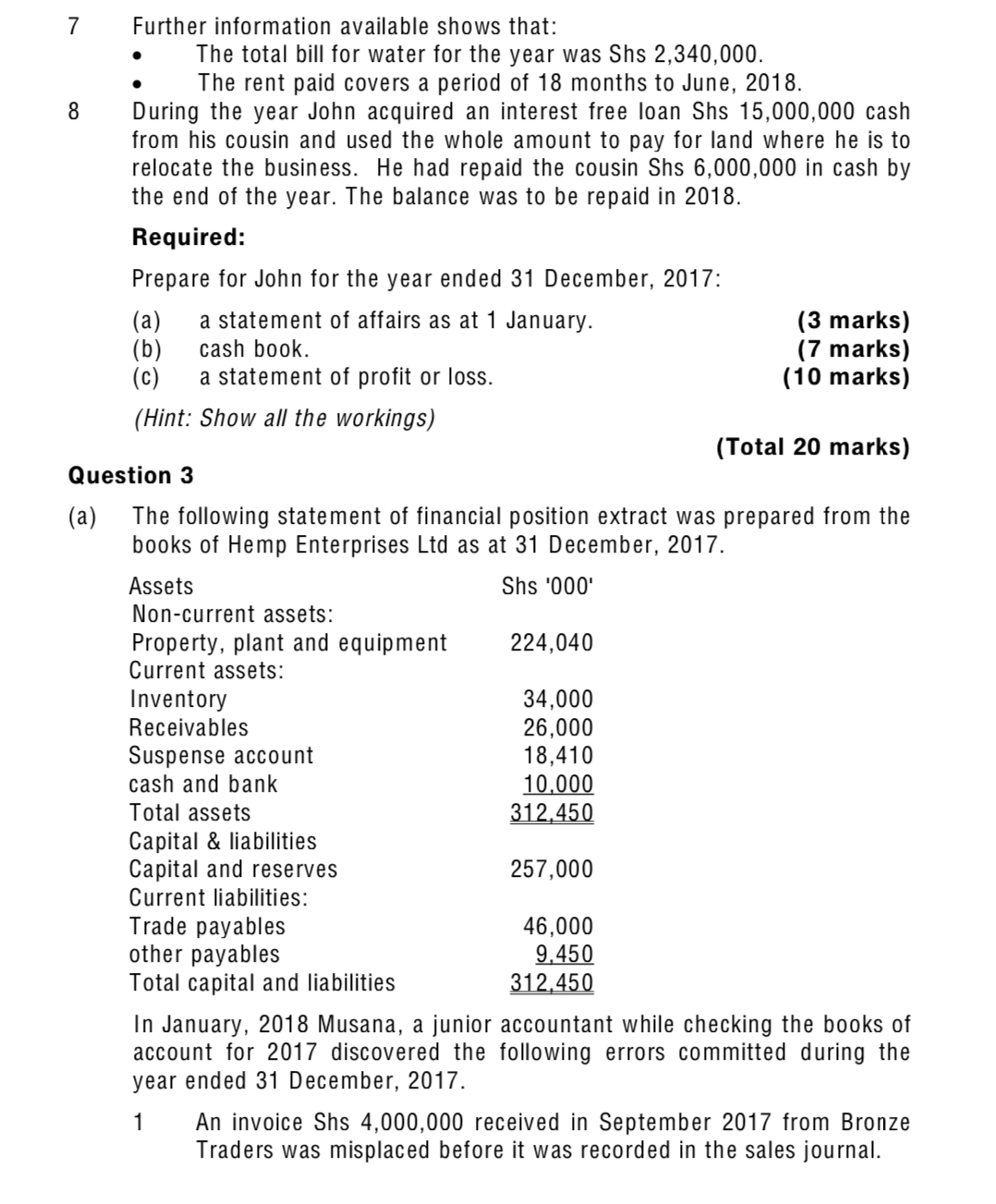

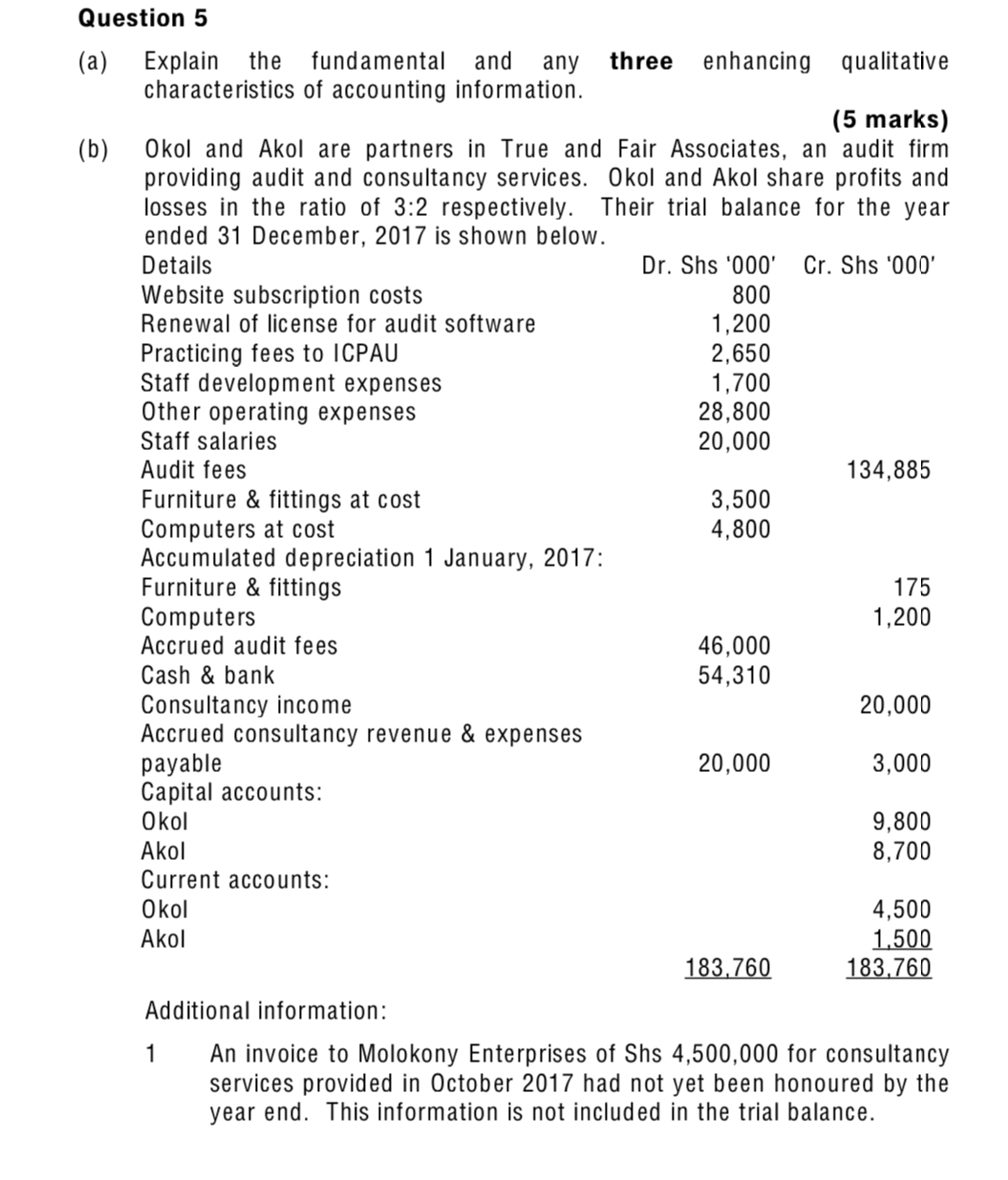

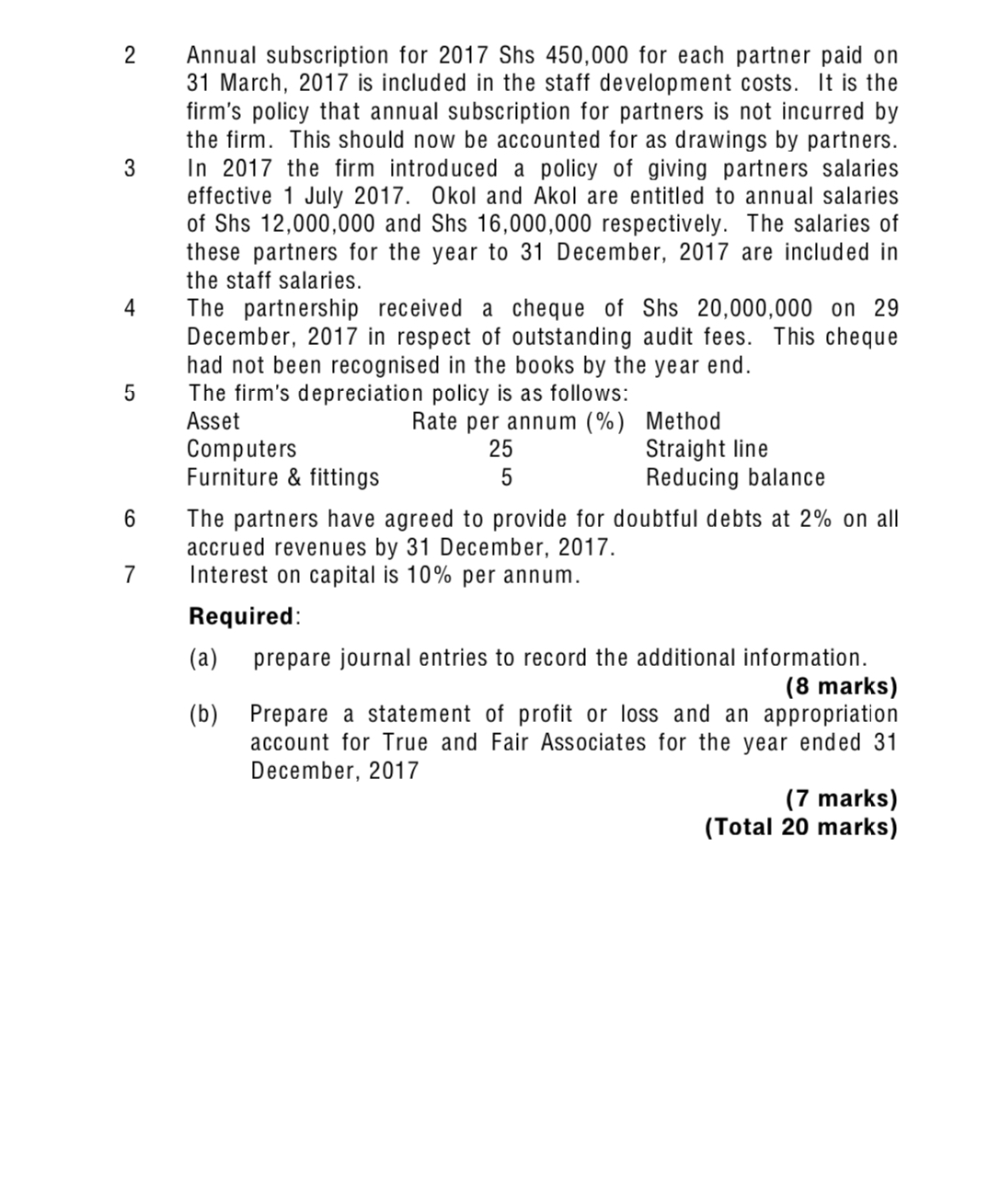

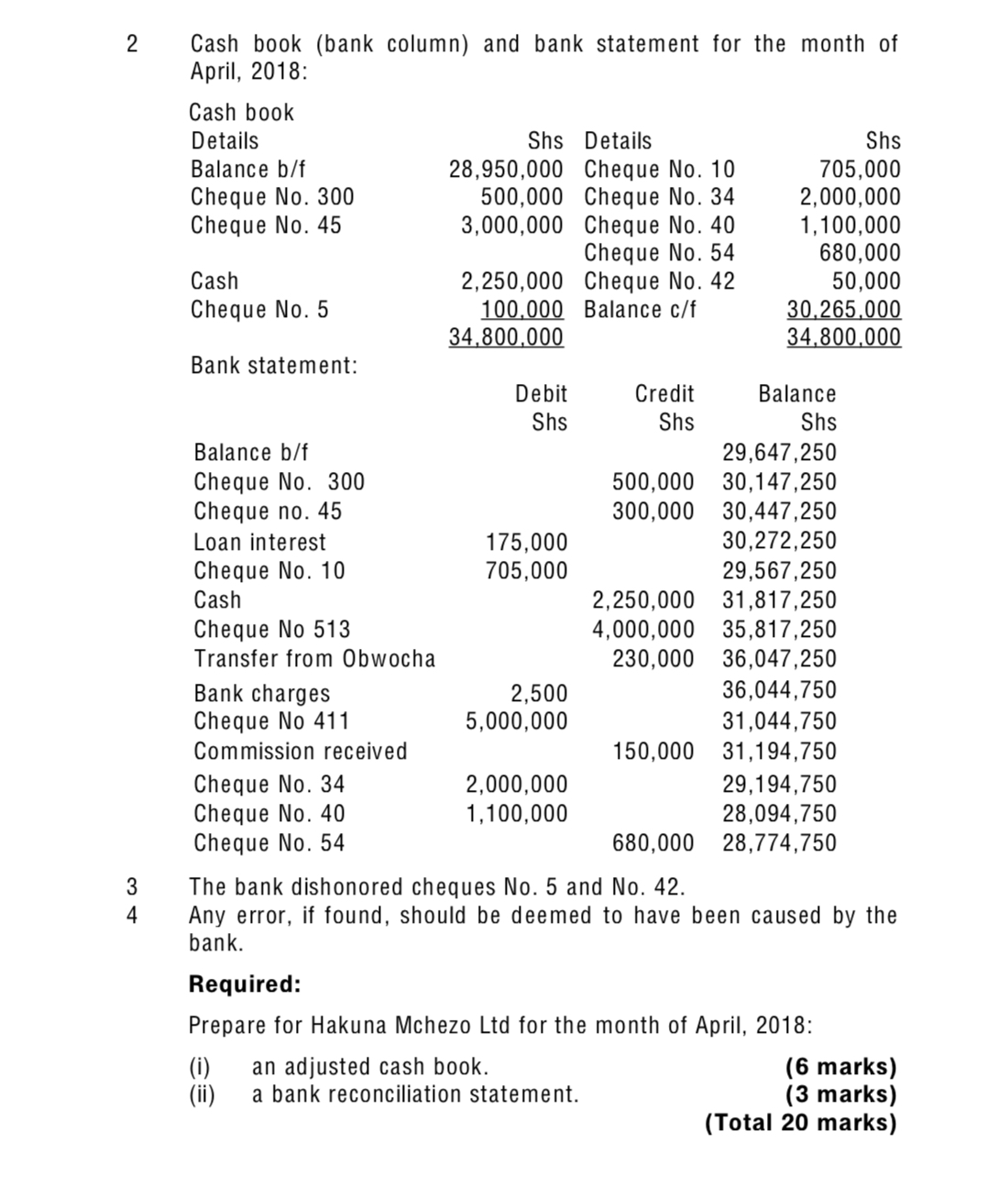

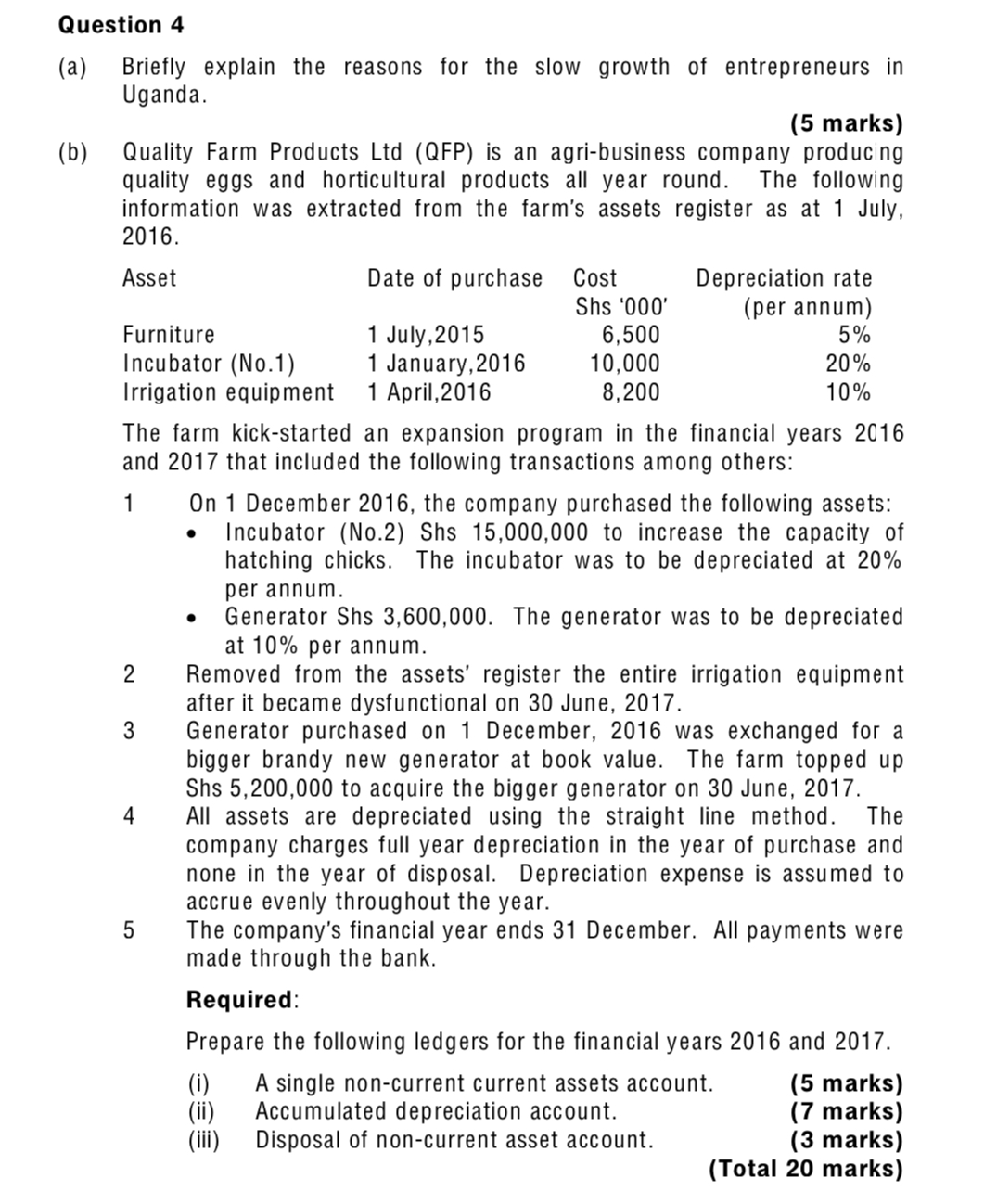

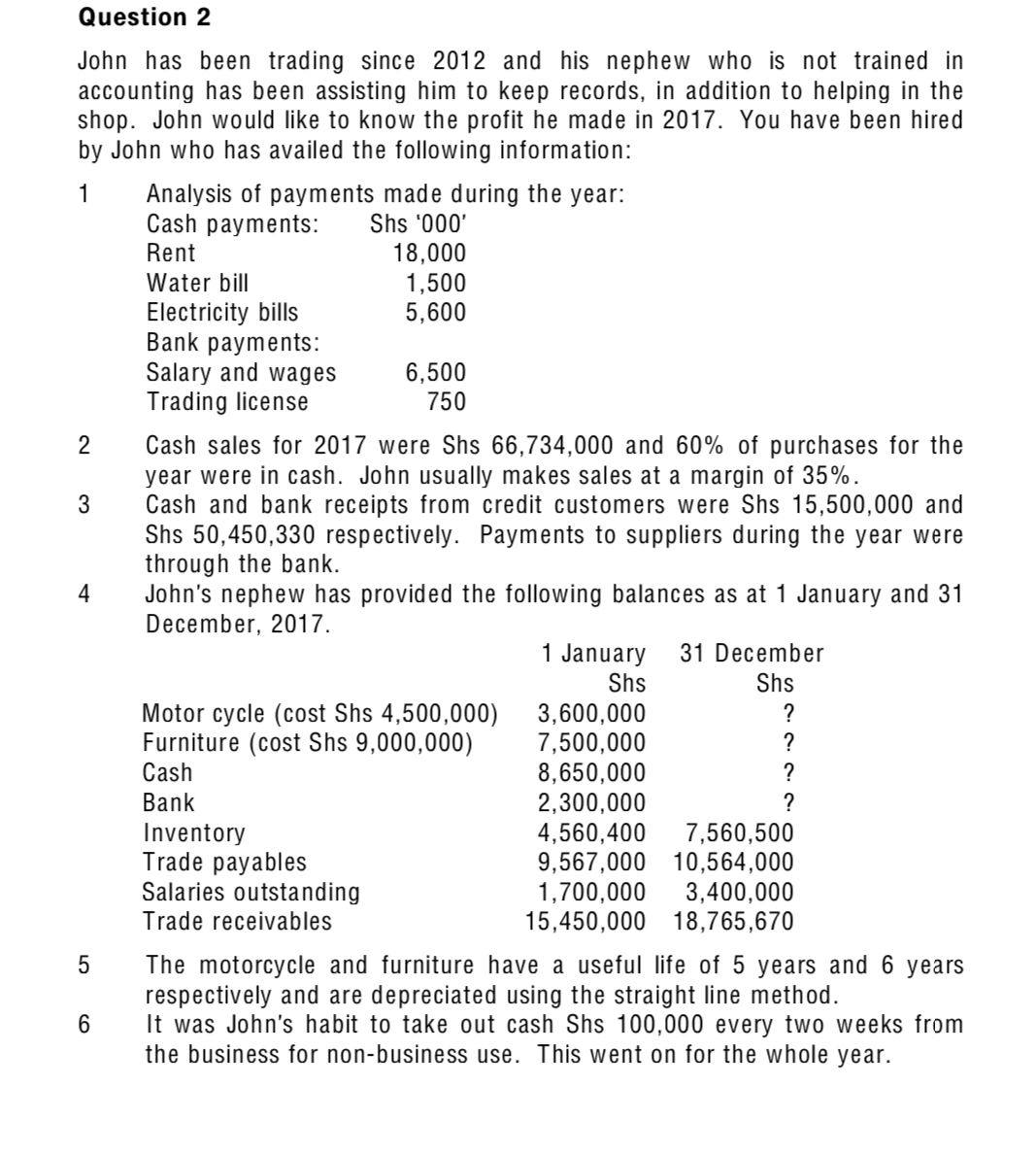

Question 6 (a) (b) Explain, with examples. the meaning and application of the following accounting concepts: (i) Accrual. (2 marks) (ii) Prudence. (2 marks) (iii) Going concern. (2 marks) (iv) Consistency. (2 marks) The following information was extracted from the books of Muscle Flex Sports Club for the year ended 31 December. 2017. Balances as at: 1 January 31 December Shs '000' Shs '000' Ordinary subscription in arrears 45,000 50,000 Ordinary subscription received in advance 25,500 28,000 Owing to suppliers of fundraising items 12,000 16,500 Owing to Ivory Hotel (venue for fundraising) 2.500 Additional information: 1. The following transactions were recorded in the receipts and payments account for the year ended 31 December, 2017. Shs '000' Fundraising dinner income 65.000 Fundraising dinner expenses 25.000 Ordinary subscription income 80.000 Life subscription 25,000 2 Life subscription is recognised over a period of 10 years. Required: Prepare for Muscle Flex Sports Club for the year ended 31 December, 2017 the: (i) ordinary subscription account. (3 marks) (ii) life subscription account. (2 marks) (iii) fundraising income account. (3 marks) (iv) extract of the statement of profit or loss and statement of financial position. (4 marks) (Total 20 marks) (b) 0101 The accountant credited a cheque receipt Shs 605.000 from a customer to the cash book as Shs 560.000. The corresponding entry in the customer's account though was correctly made. Sales Shs 7.680.000 were correctly entered in the cash book but the double entry to the respective account was not completed. A discount received Shs 102.000 was credited to the discounts allowed account as Shs 210.000. The corresponding entry was correctly completed. The purchases account was under cast by Shs 23,137.000. Motor vehicle repairs Shs 840.000 was credited to the motor vehicles account as 840,000. The corresponding entry in the cash book was correctly made. Goods worth Shs 2.340.000 taken by directors for personal use were not recorded anywhere in the books. Required: Prepare for Hemp Enterprises Ltd: (i) Journal entries to correct the above errors. (8 marks) (ii) A suspense account after passing entries correcting the errors. (3 marks) The bookkeeper of Hakuna Mchezo Ltd was unable to do the reconciliation for the month of March 2018. The details provided below were for two months; March and April. 2018. 1 Items for March 2018: Unpresented cheques: Shs Cheque No. 313 500.000 Cheque No. 411 5.000.000 Uncredited cheques: Cheque No. 513 4.000.000 Cheque No. 550 2.500.000 Direct debits: Bank charges 2.500 Excise duty 250 Direct credits Interest received 500.000 Dividends 1.200.000 7 Further information available shows that: . The total bill for water for the year was Shs 2.340.000. o The rent paid covers a period of 18 months to June. 2018. 8 During the year John acquired an interest free loan Shs 15,000.000 cash from his cousin and used the whole amount to pay for land where he is to relocate the business. He had repaid the cousin Shs 6.000.000 in cash by the end of the year. The balance was to be repaid in 2018. Required: Prepare for John for the year ended 31 December, 2017: (a) a statement of affairs as at 1 January. (3 marks) (b) cash book. (7 marks) (c) a statement of profit or loss. (10 marks) (Hint: Show all the workings) (Total 20 marks) Question 3 (a) The following statement of financial position extract was prepared from the books of Hemp Enterprises Ltd as at 31 December. 2017. Assets Shs '000' Non-current assets: Property. plant and equipment 224,040 Current assets: Inventory 34.000 Receivables 26.000 Suspense account 18.410 cash and bank 10000 Total assets M Capital 8. liabilities Capital and reserves 257,000 Current liabilities: Trade payables 46.000 other payables 9,450 Total capital and liabilities M In January. 2018 Musana. a junior accountant while checking the books of account for 2017 discovered the following errors committed during the year ended 31 December. 2017. 1 An invoice Shs 4.000.000 received in September 2017 from Bronze Traders was misplaced before it was recorded in the sales iournal. Question 5 (a) Explain the fundamental and any three enhancing qualitative characteristics of accounting information. (5 marks) (b) Okol and Akol are partners in True and Fair Associates, an audit firm providing audit and consultancy services. Okol and Akol share profits and losses in the ratio of 3:2 respectively. Their trial balance for the year ended 31 December, 2017 is shown below. Details Dr. Shs '000' Cr. Shs '000' Website subscription costs 800 Renewal of license for audit software 1,200 Practicing fees to ICPAU 2,650 Staff development expenses 1,700 Other operating expenses 28,800 Staff salaries 20,000 Audit fees 134,885 Furniture & fittings at cost 3,500 Computers at cost 4,800 Accumulated depreciation 1 January, 2017: Furniture & fittings 175 Computers 1,200 Accrued audit fees 46,000 Cash & bank 54,310 Consultancy income 20,000 Accrued consultancy revenue & expenses payable 20,000 3,000 Capital accounts: Okol 9,800 Akol 8,700 Current accounts: Okol 4,500 Akol 1,500 183,760 183,760 Additional information: 1 An invoice to Molokony Enterprises of Shs 4,500,000 for consultancy services provided in October 2017 had not yet been honoured by the year end. This information is not included in the trial balance.Annual subscription for 2017 Shs 450,000 for each partner paid on 31 March, 2017 is included in the staff development costs. It is the firm's policy that annual subscription for partners is not incurred by the firm. This should now be accounted for as drawings by partners. In 2017 the firm introduced a policy of giving partners salaries effective 1 July 2017. 0kol and Akol are entitled to annual salaries of Shs 12,000,000 and Shs 16,000,000 respectively. The salaries of these partners for the year to 31 December, 2017 are included in the staff salaries. The partnership received a cheque of Shs 20,000,000 on 29 December. 2017 in respect of outstanding audit fees. This cheque had not been recognised in the books by the year end. The firm's depreciation policy is as follows: Asset Rate per annum (%) Method Computers 25 Straight line Furniture & fittings 5 Reducing balance The partners have agreed to provide for doubtful debts at 2% on all accrued revenues by 31 December, 2017. Interest on capital is 10% per annum. Required: (a) prepare iournal entries to record the additional information. (8 marks) (b) Prepare a statement of profit or loss and an appropriation account for True and Fair Associates for the year ended 31 December, 2017 (7 marks) (Total 20 marks) 2 #00 Cash 000k (bank column) and bank statement 10f the month 01 April, 2018: Cash book Details Shs Balance bit 28,950.000 Cheque No. 300 Cheque No. 45 500,000 3.000.000 Cash 2.250.000 Cheque No. 5 100.000 30.000000 Bank statement: Debit Shs Balance blf Cheque No. 300 Cheque no. 45 Loan interest 175,000 Cheque No. 10 705.000 Cash Cheque No 513 Transfer from Obwocha Bank charges 2.500 Cheque No 411 5.000.000 Commission received Cheque No. 34 2.000.000 Cheque No. 40 1.100.000 Cheque No.54 Shs 705,000 2.000.000 1.100.000 680.000 50.000 30.205.00.11 30.00.0000 Details Cheque No. 10 Cheque No.34 Cheque No. 40 Cheque No.54 Cheque No.42 Balance c/f Credit Shs 500.000 300.000 Balance Shs 29.647.250 30.147.250 30.447.250 30,272,250 29.567.250 31,817,250 35,817,250 36,047,250 36,044,750 31 .044.750 31 .194.750 29.194.750 28.094.750 28.774.750 2.250.000 4,000,000 230.000 150.000 680.000 The bank dishonored cheques No.5 and No. 42. Any error, if found. should be deemed to have been caused by the ban k. Required: Prepare for Hakuna Mchezo Ltd for the month of April. 2018: (i) an adjusted cash book. (ii) a bank reconciliation statement. (6 marks) (3 marks) (Total 20 marks) Question 4 (a) ('3) Briefly explain the reasons for the slow growth of entrepreneurs in Uganda. (5 marks) Quality Farm Products Ltd (0FP) is an agri-business company producing quality eggs and horticultural products all year round. The following information was extracted from the farm's assets register as at 1 July. 2016. Asset Date of purchase Cost Depreciation rate Shs '000' (per annum) Furniture 1 July,2015 6,500 5% Incubator (No.1) 1 January.2016 10.000 20% Irrigation equipment 1 April.2016 8.200 10% The farm kick-started an expansion program in the financial years 2016 and 2017 that included the following transactions among others: 1 0n 1 December 2016. the company purchased the following assets: . Incubator (No.2) Shs 15,000,000 to increase the capacity of hatching chicks. The incubator was to be depreciated at 20% perannum. . Generator Shs 3,600,000. The generator was to be depreciated at 10% per annum. 2 Removed from the assets' register the entire irrigation equipment after it became dysfunctional on 30 June. 2017. 3 Generator purchased on 1 December, 2016 was exchanged for a bigger brandy new generator at book value. The farm topped up Shs 5,200,000 to acquire the bigger generator on 30 June. 2017. 4 All assets are depreciated using the straight line method. The company charges full year depreciation in the year of purchase and none in the year of disposal. Depreciation expense is assumed to accrue evenly throughout the year. 5 The company's financial year ends 31 December. All payments were made through the bank. Required: Prepare the following ledgers for the financial years 2016 and 2017. (i) A single non-current current assets account. (5 marks) (ii) Accumulated depreciation account. (7 marks) (iii) Disposal of non-current asset account. (3 marks) (Total 20 marks) Question 2 John has been trading since 2012 and his nephew who is not trained in accounting has been assisting him to keep records, in addition to helping in the shop. John would like to know the profit he made in 2017. You have been hired by John who has availed the following information: 1 Analysis of payments made during the year: Cash payments: Shs '000' Rent 18,000 Water bill 1,500 Electricity bills 5,600 Bank payments: Salary and wages 6,500 Trading license 750 2 Cash sales for 2017 were Shs 66,734,000 and 60% of purchases for the year were in cash. John usually makes sales at a margin of 35%. 3 Cash and bank receipts from credit customers were Shs 15,500,000 and Shs 50,450,330 respectively. Payments to suppliers during the year were through the bank. 4 John's nephew has provided the following balances as at 1 January and 31 December, 2017. 1 January 31 December Shs Shs Motor cycle (cost Shs 4,500,000) 3,600,000 ? Furniture (cost Shs 9,000,000) 7,500,000 ? Cash 8,650,000 '7 Bank 2,300,000 ? Inventory 4,560,400 7,560,500 Trade payables 9,567,000 10,564,000 Salaries outstanding 1,700,000 3,400,000 Trade receivables 15,450,000 18,765,670 5 The motorcycle and furniture have a useful life of 5 years and 6 years respectively and are depreciated using the straight line method. 6 It was John's habit to take out cash Shs 100.000 every two weeks from the business for non-business use. This went on for the whole year

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Accounting Questions!