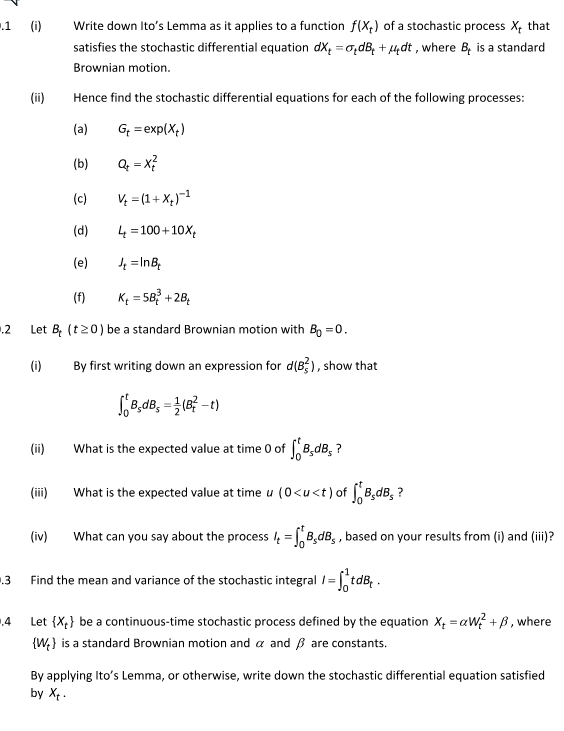

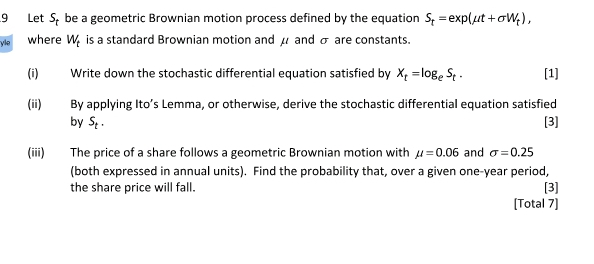

Question: Answer all the questions well. 1 (1) Write down Ito's Lemma as it applies to a function f(X, ) of a stochastic process X, that

Answer all the questions well.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock