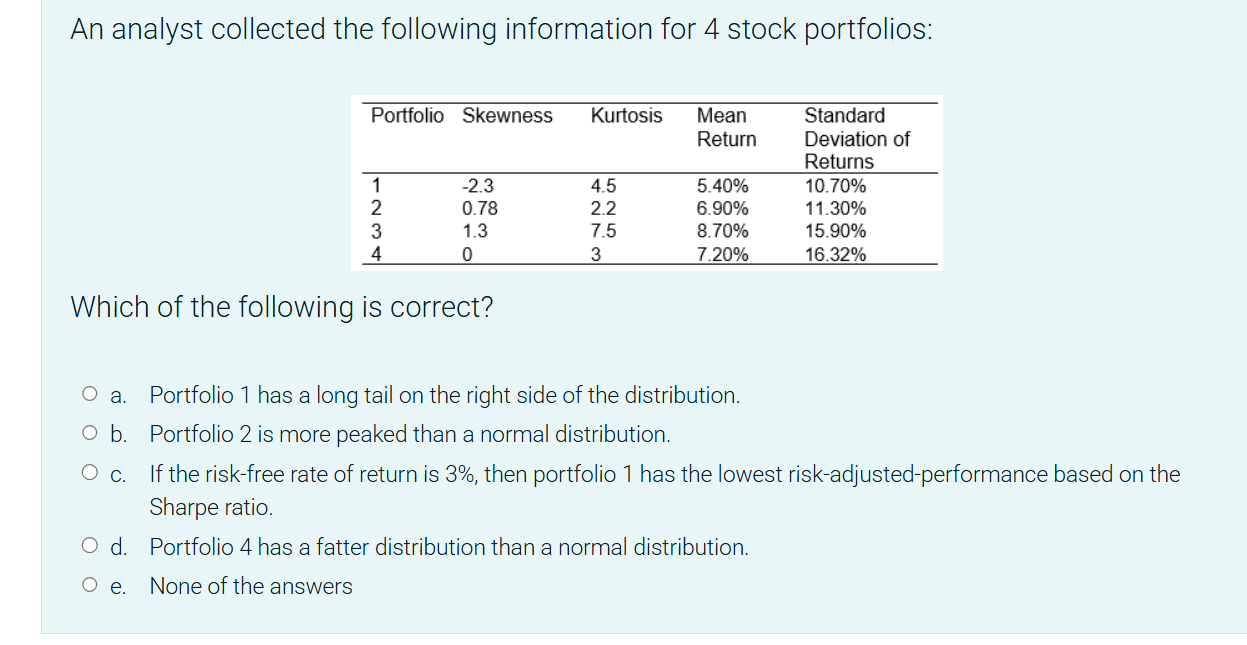

Question: answer An analyst collected the following information for 4 stock portfolios: Kurtosis Mean Standard Portfolio Skewness Return Deviation of Returns 1 2 3 4 -2.3

answer

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock